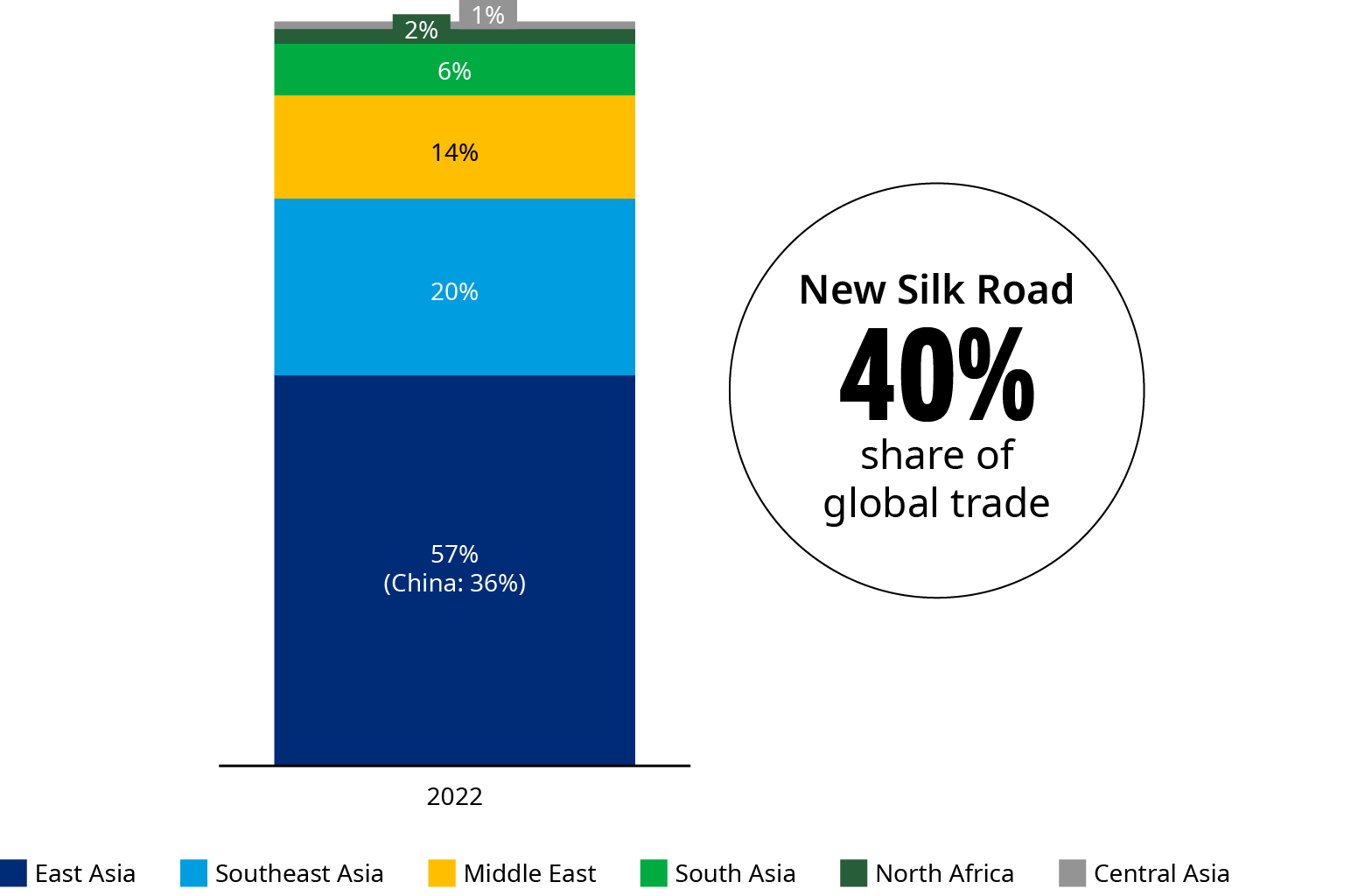

The New Silk Road is the world’s manufacturing hub, accounting for over 40% of global trade. However, supply chains are evolving fast in response to prices, politics, and pandemics, and so the region’s manufacturing footprint will look very different in 10 years’ time.

While China will remain the region’s largest manufacturer, lower-cost producers, such as Vietnam, India, or even Egypt, will grow in importance. Higher-cost producers, such as South Korea, Japan, Saudi Arabia, and the United Arab Emirates (UAE), will also have roles to play.

Whether because of the shift from cost to resilience or the development of new technologies, the Silk Road will shape the world’s future supply chain. There are multiple pathways ahead, and while some are more positive than others, we see four exciting areas of opportunity:

- China Inc. goes truly global

Chinese manufacturers are increasingly investing in the Silk Road, rather than just exporting, opening up new joint venture opportunities. - Emerging private capital opportunities

Production relocation from China to the rest of the region is creating new opportunities for private capital, from manufacturing to logistics. - Asian manufacturing ecosystems

By targeting Asian manufacturing ecosystems, the Gulf Cooperation Council (GCC) region can position itself as a hub for exports into the Middle East and Africa. - The green manufacturing imperative

With the region facing looming carbon regulations and the changing priorities of multinational corporations (MNCs), green leaders will capture larger shares of the world’s future supply chain.

Three forecasts for the Silk Road’s future supply chain

Our forecasts are based on a matrix of integration and transformation. While high levels of integration and transformation would supercharge the New Silk Road, low levels would extend timelines for progress. The forecasts are not mutually exclusive, and the final scenario may contain elements of each.

Forecast 1: A regionalized economic bloc

In this potential scenario that involves high integration and medium transformation, intra-regional trade would rise rapidly as manufacturing relocates, FTAs are upgraded, and the region integrates and transforms rapidly.

The Silk Road’s intra-regional trade would rise to 70% of total trade, as the shift in supply chains would result in greater flows of intermediate inputs between countries. The region’s existing bilateral and multilateral FTAs would continue to expand and upgrade. The GCC countries would also join Asia’s major trade groups as observers or full partners, and talk of a super-regional trade group, such as an Asia, Middle East, and Africa, or “Silk Road” bloc would emerge.

Additionally, private sector opportunities in industrial real estate, logistics, and warehousing would grow rapidly, with sovereign wealth funds and major private capital investors taking the lead. The GCC would also develop rapidly as a manufacturing and logistics hub for Asian companies expanding into the Middle East and Africa.

Forecast 2: A China-centric economic region

This low-integration, low-transformation potential scenario involves China remaining central to the region’s manufacturing supply chains, as the scope for supply chain relocation reaches its limit.

This is because Vietnam would see costs rise rapidly as land and labor shortages loom, while India would struggle to scale foreign manufacturing owing to its well-known constraints. On the other hand, China’s cost competitiveness, automation, and access to clean energy would ensure its ability to retain a significant share of the region’s export manufacturing. Manufacturing would grow across the region, but China would be critical to the supply of component parts.

Cross-border payment systems, meanwhile, would develop slowly, as the return on investment would remain low given that intra-regional trade flows would be lower than in other potential scenarios.

Forecast 3: A clean and digitized economic bloc

In this potential scenario that involves medium integration and high transformation, there would be a shift toward decarbonized and digital trade that is faster than expected, leaving a widening gap between innovation leaders and laggards.

Regulatory changes across the region and in Europe would accelerate the push to decarbonized production to the benefit of clean energy producers in the GCC. Decarbonization efforts would accelerate the digitization of trade to improve traceability, but a gap would open up between sector leaders, such as China and Japan, and laggards, such as Indonesia and Egypt, who risk being stuck producing low-value manufactured goods.

Private capital, meanwhile, would focus on building carbon-neutral industrial parks, leaving legacy industrial assets struggling to compete for high-value exports. While the returns on new and legacy investments would widen steadily, China’s clean energy ambitions would ensure the country retains a sizeable share of global exports despite political tensions.

This article is part of our New Silk Road series