There’s a lot of optimism around cell and gene therapies and the potential to reshape patient care. Every breakthrough generates more enthusiasm that patients will get access to innovative treatments for life-threatening diseases, with CAR-Ts changing long- term outcomes dramatically for conditions such as B- cell lymphoma and acute lymphoblastic leukaemia (ALL), while gene augmentation therapies are doing the same in conditions such as muscular dystrophy (SMA) and mutation-associated retinal dystrophy.

New therapies for life-threatening diseases

New therapies for Hemophilia A and B are coming to market, and many others that address larger volume indications like Parkinson’s Disease are projected to launch in the near- to midterm. A sizeable portion of drugs projected to launch by 2028 are aimed at diseases impacting one in 5,000 people, or even one in 1,000, significantly higher than the treatments launched until now, which generally targeted diseases affecting less than one in 50,000 or even 100,000. Payers and regulators have been making headway in revamping their assessment frameworks to make room for innovation, while health systems are lagging in developing the right capacity and capability that will be needed to scale up in the future.

Challenges in delivering cell and gene therapies

Several factors impact where cell and gene therapies can be delivered, including how safe they are to use, the capabilities and infrastructure needed to administer treatments, and how much financial burden is put on providers beyond the cost of the drug. Although not every modality within cell and gene therapy faces the same challenges from a treatment delivery perspective, products that have launched to date have been limited to a subset of tertiary care, mostly academic institutions. Biopharma companies are individually certifying and accrediting sites to make sure they have the right capabilities, infrastructure, and processes in place to handle the product and manage patients. Sites generally have to meet a range of requirements and use ordering systems developed by individual manufacturers, creating complexity and draining resources.

Tackling bottlenecks and scaling cell and gene therapy

Scaling cell and gene therapy requires advancing beyond the current model and addressing bottlenecks such as highly diverse and complex treatment delivery process, supply chains, capacity constraints and scarce capabilities. This is often compounded by misaligned financial incentives between manufacturers, payers, administering physicians and hospitals.

Learning from transplant care

The evolution of transplant care offers a roadmap for scaling cell and gene therapy. Like cell and gene therapies, the use of transplants come with significant safety concerns. This translates into the need for a highly- skilled workforce and continuous patient monitoring. Advances in science and technology (for example, greater understanding of Human Leukocyte Antigens (HLA) matching and complications such as GVHD), standardization of delivery capabilities, and clear alignment on financial incentives (for example, via introduction of dedicated DRG codes for Hematopoietic stem cell transplantation procedures) spurred a dramatic uptick the number of transplants in the US. Barriers remain in creating equitable access, but the upward trajectory is a net positive for the industry and patients.

Preparing health system care delivery for CGTs

Progress is needed in three key areas if cell and gene therapies are going to gain more mainstream traction:

Standardizing capabilities: Similar to what the industry experienced during the nascent days of electronic health records, there is limited harmony between stakeholders as they aim to bringing cell and gene therapies to market. Each drug manufacturer is creating a mini ecosystem that works for their products. This, in turn, forces providers to create workflows and capabilities unique to each pharmaceutical company and creates a strain on resources. The solution requires standardizing the capabilities, infrastructure, and workflow needed to deliver CGT to patients. Organizsations such as FACT and JACIE are trying to build standardization, but it is unclear if there is consolidated biopharma industry input going into the process. Working closely with biopharma manufacturers to develop standards and readiness checklists that can be applicable across modalities and therapeutic areas will be a key enabler for building scale.

Solving for safety: Although steady progress has been made by medical researchers, regulators, and the industry, safety concerns persist for cell and gene therapies. A large reason for cell and gene therapies being delivered where they are today is due to the pre and post treatment requirements driven by current safety concerns. Scientific evolution to generate safer therapies will enable a shift from tertiary to secondary care and community setting. Allogeneic cell therapies currently in development are aiming to reduce the complexity and improve the safety profile of cell therapies. While this a move in the right direction, this will likely take time to mature and may not be an option for all modalities and disease areas. Nonetheless, transitioning even a portion of therapies from tertiary care setting will help create capacity and make judicious use of the available resources.

Creating clear financial incentives: While there are financial and marketing benefits for academic and specialty medical centers to participate in clinical trials, most are not eager to deepen relationships with drug manufacturers and become commercial sites. Those pursuing that route have to strike a delicate balance between their research missions and the commercial opportunities. Additionally, payers don’t have visibility into the upfront infrastructure investment and ongoing costs providers incur to get accredited to deliver CGT to patients. For gene augmentation therapies, bypassing buy and bill and using specialty pharmacies is helping payers manage their costs but also creating a financial disincentive for hospitals to pursue CGT. For autologous cell therapies, although the DRGs have been adjusted over the past year to increase reimbursement to sites, they still fail to cover the full cost of the end-to-end process and all financial risks to the provider. Academic centers need to share cost data with payers and provide a clear picture of the total cost, not just the cost of therapy. There is a clear need to bring payers onboard and develop a clear dollar flow that incentivizes HPCs and sites to build necessary capabilities to administer cell and gene therapies and expand access to patients.

Tackling these issues will pave the way to additional treatment delivery models that extend beyond tertiary care and create additional capacity, including in community settings.

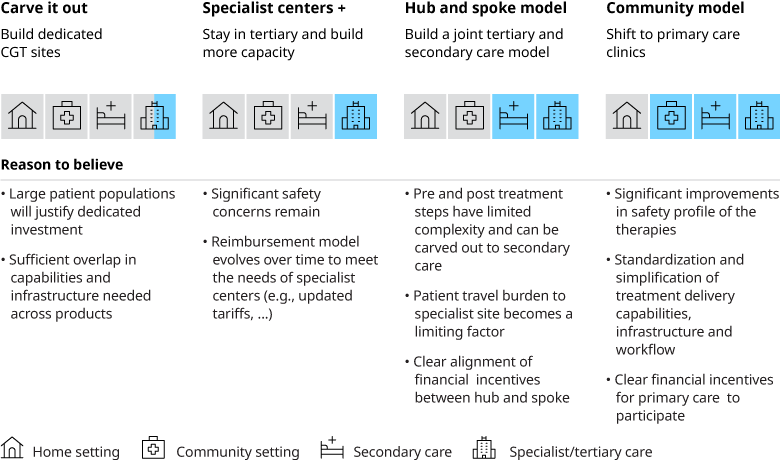

Each of these models have their pros and cons and may not work for all modalities within CGT. For example, for allogeneic cell therapies and gene augmentation therapies a Hub and Spoke model or even a community model could work if the safety profile improves, and financial incentives are aligned across the different players in the ecosystem. Whereas for autologous cell therapies developing dedicated sites and units may be a reasonable option, especially given the volume of patients that will be eligible for cell therapies is likely to far exceed the volume of transplant patients today. Given the right financial incentives, this could open the door to creating significant capacity in the system.

Supercharging healthcare systems for cell and gene therapies

The evolution of the site of care model over time will depend on the success of the treatments and the size of the population they address. However, there is a clear need to drive alignment across payers, biopharma company, and providers. Mapping out the patient pathways early to highlight gaps in diagnosis, delivery capability, infrastructure, capacity, and bringing payers and providers onboard is key to successful collaboration. Early dialogue will help biopharma companies figure out where they can help build, how they should develop their supply chains, and where a greater lift will be needed from health systems. The transplant analogy shows that this can be done, but it will require all stakeholders to align and co-create the care infrastructure and pathways of the future, so that those who need it can access the treatments.

This white paper is an output of a recent cell and gene therapy (CGT) roundtable convened by Oliver Wyman to bring together industry leaders across biopharma, payer and provider organizations to discuss the current state of play for cell and gene therapy site of care model, future outlook and key success factors.