When it comes to assessing loss cost experience for auto insurance, it’s important to consider the latest industry trends. In spite of all the recent uncertainties in the world, here are useful insights that can help your organization better understand automobile insurance risk moving forward. Since mid-2013, insurance carriers have noticed an increase in the frequency of automobile property damage and collision claims. To help better understand the ensuing loss cost experience, the Casualty Actuarial Society (CAS) identified trends based on data from the Federal Highway Administration, Bureau of Labor Statistics, the Census Bureau and other sources. Their findings identify key reasons for claims frequency and severity for each type of coverage and are worth a closer look.

Then, 2020 arrived. The unprecedented COVID-19 pandemic dramatically changed the way people traveled and impacted how companies conducted their business. No industry was left unscathed, including insurance. Ultimately, the pandemic could have permanent effects on the risk profile of property and casualty (P&C) insurance exposures.

In October 2020, the largest automobile claim in history was awarded by virtual trial in Florida, setting a new benchmark for future claims. Looking further into the future, ride-sharing services, artificial intelligence and autonomous vehicles will all likely change the landscape of the automobile insurance industry.

The summary below highlights 1) the results from a CAS study, released January 10, 2020, which identifies more trends for each sub-coverage category of personal automobile insurance, and 2) the impact seen thus far from the global pandemic and other emerging risk factors. We would like to point out that we do not own the rights to these exhibits. They are our adaptations based on the data and images provided from Casualty Actuarial Society.

Executives and risk managers may be wise to better understand the trends and potential root causes of auto claims in an effort to predict their organization’s loss cost experience more accurately. Oliver Wyman’s actuarial team is well-versed in on-going industry trends and stands ready to help.

Bodily Injury (BI) trends involve no-fault vs. tort states, congestion and driver’s age

What it covers: BI pays for injuries and lost work time caused to another person while the insured person is operating a vehicle, regardless of whether the injured person(s) is in a vehicle.

Contributing factors for BI claims:

- Rural and urban congestion. Both rural and urban congestion have strong positive relationships with loss cost and frequency.

- The percentage of elderly and young drivers. Older and younger drivers both have negative relationships with loss cost and frequency in tort states. In contrast, for no-fault states, the proportion of female drivers over age 80 and under age 24 had positive relationships with loss cost and frequency.

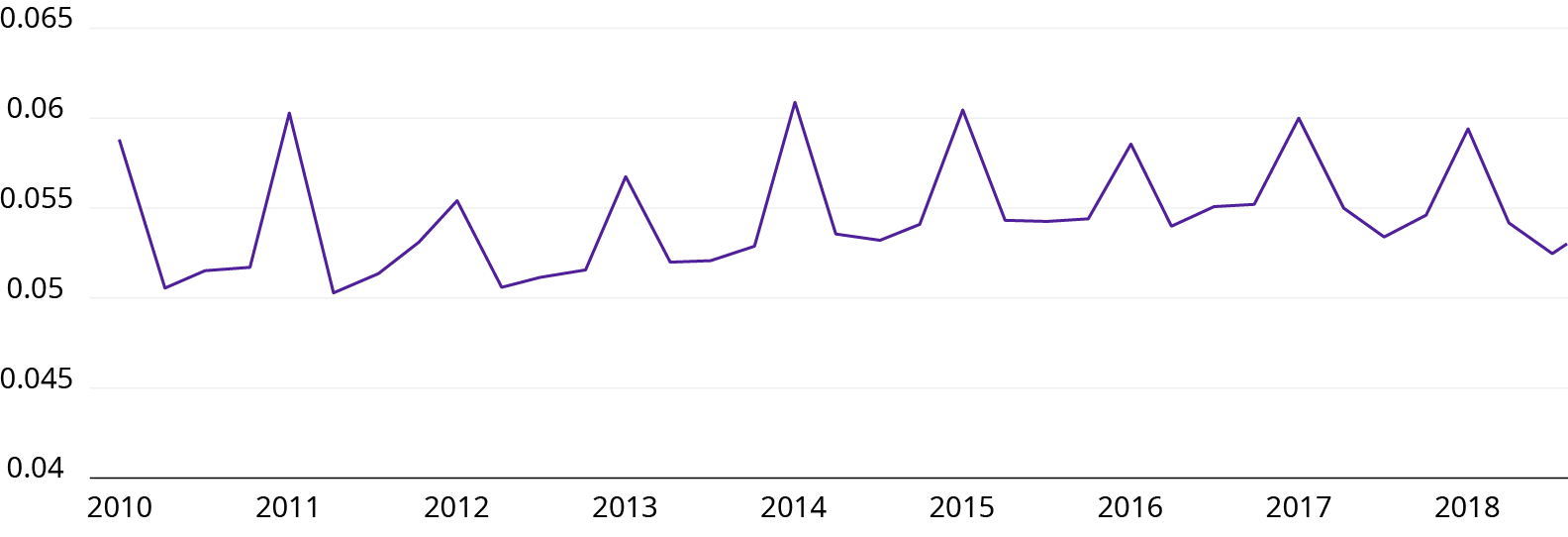

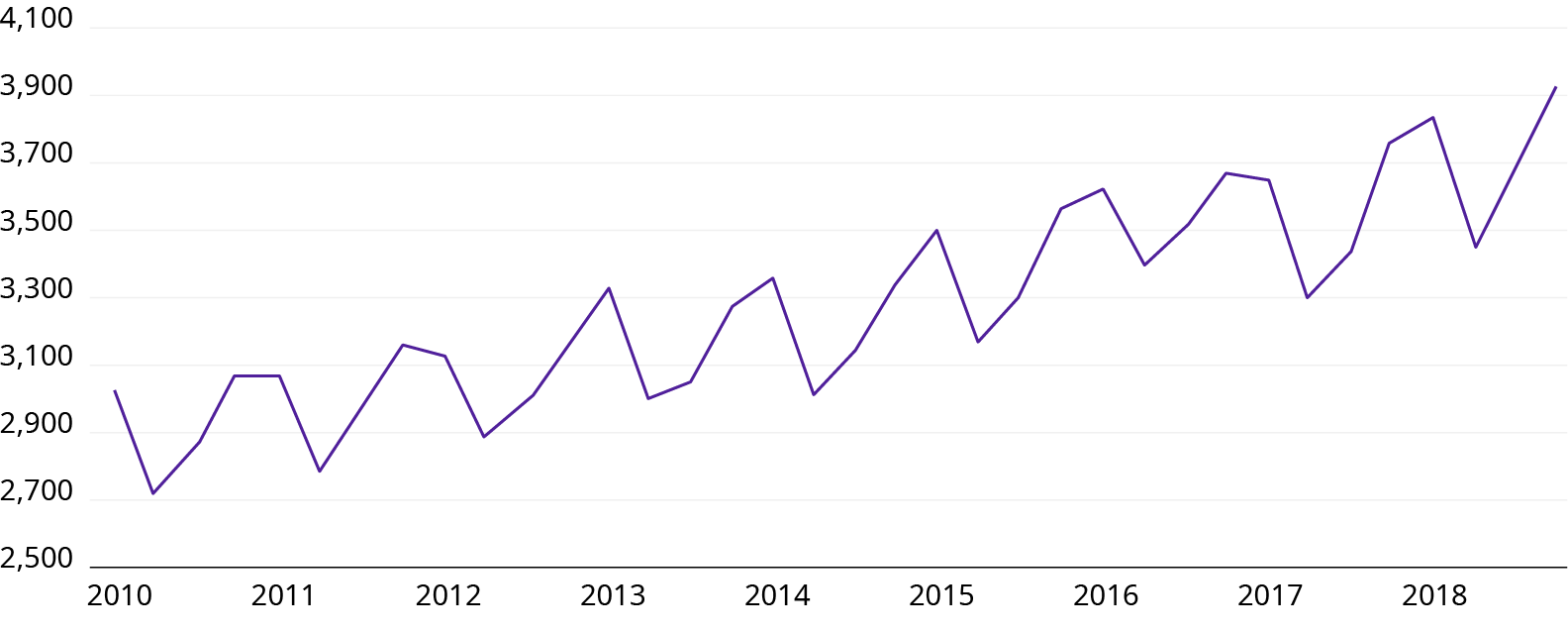

Collision trends relate to time of year, severity, snowfall, driver’s age and the relationship of vehicle miles or licensed drivers per mile of roadway in the state

What it covers: Collision coverage helps pay to repair or replace vehicles damaged in an accident with another vehicle or object.

Contributing factors for collision claims:

- Time of year and severity. Frequency has a strong annual seasonal pattern, with a peak in the first quarter. The severity of claims has increased over time more rapidly than inflation. One theory behind the increase is the higher cost of repairing automobiles with added safety features and new technologies.

- Snowfall. States were grouped into three categories based on their annual snowfall:

- Harsh winter states have the highest collision losses, particularly in the winter since snowfall hinders driving. Harsh winter states include AK, CO, MA, ME, MI, NH, NY, VT, WI and WY.

- Moderate and mild winter states also have this seasonality, but less dramatically.

- Some mild winter states, like CA and FL, have higher population densities, which results in a higher frequency from having more drivers on the road.

- Percentage of drivers under age 24 and over age 79. Both of these age groups were negatively correlated with collision frequency and loss cost. Although these drivers are more likely to cause collisions, they don’t contribute to congestion as much as drivers between these ages.

- Vehicle miles traveled per mile of roadway in the state and licensed drivers per mile of roadway.Both of these are indicators of congestion and are strongly correlated with collision frequency and loss cost.

Exhibit 1: Collision Frequency Over Time

Source: Casualty Actuarial Society, Auto loss costs: Collision Report

Exhibit 2: Collision Severity Over Time

Source: Casualty Actuarial Society, Auto loss costs: Collision Report

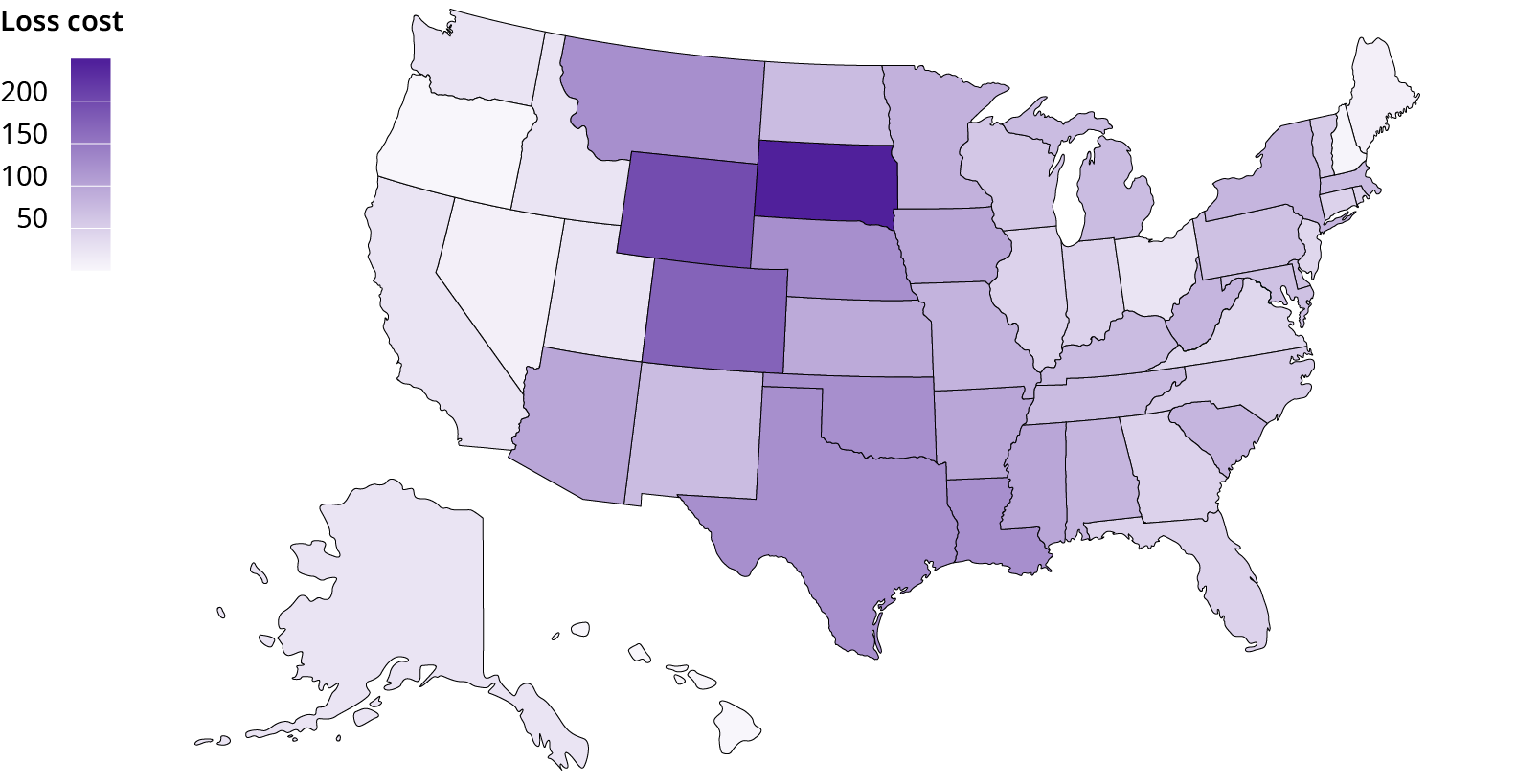

Comprehensive (COMP) trends involve weather events, wildfires, low-cost windshield replacement and increased severity

What it covers: COMP covers theft and any vehicle damage not caused by a collision, but rather by natural causes or those of pure happenstance.

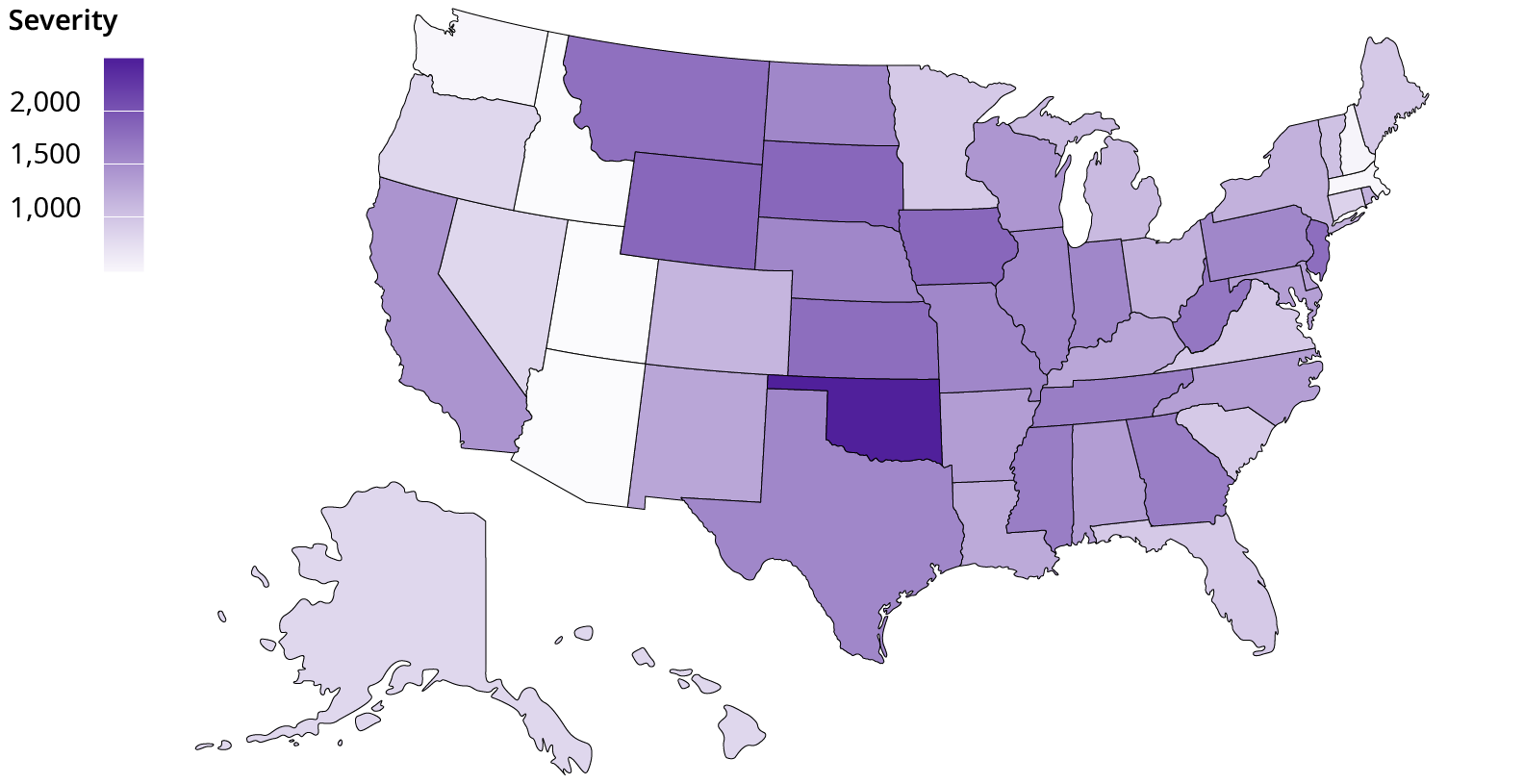

High loss cost states are from the Midwest, perhaps due to the high risk of natural disasters like hail, floods and tornados.

Exhibit 3: State Loss Cost US Map

Source: Casualty Actuarial Society, Auto loss costs: Comprehensive Report

Contributing factors for COMP claims:

- Total land area and weather. Western and central states have more total land area and harsher weather than in smaller states along the Eastern Seaboard.

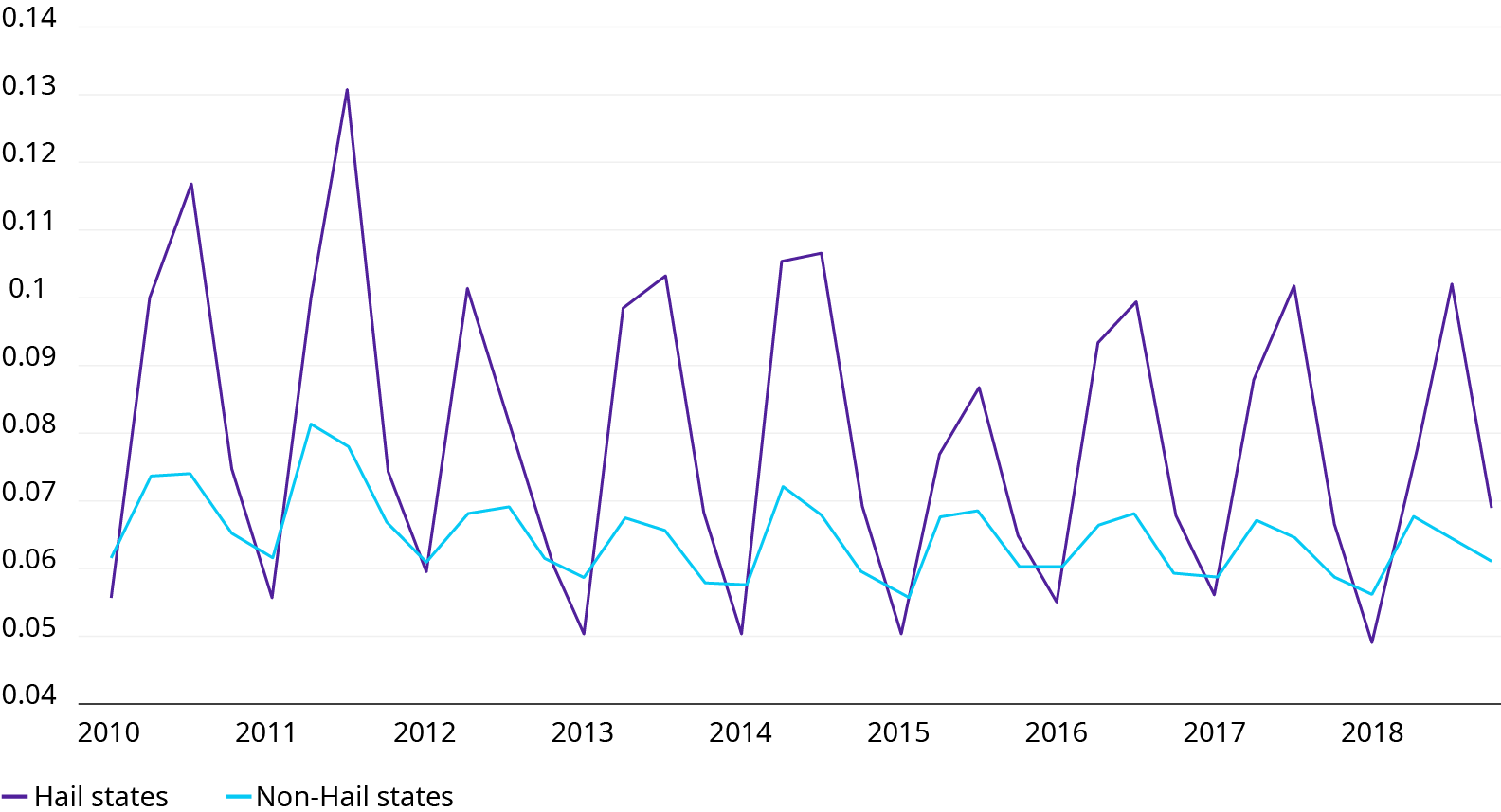

- Hailstorms cause higher COMP frequency. During the spring and summer, COMP frequency is higher than in other seasons because of weather conditions, including hailstorms. Certain states, including AZ, CO and TX, are susceptible to hailstorms and have higher COMP frequencies than other states. Severe hailstorms during 2010 and 2011 resulted in higher than usual COMP frequencies in hail-prone states (see Exhibit 4).

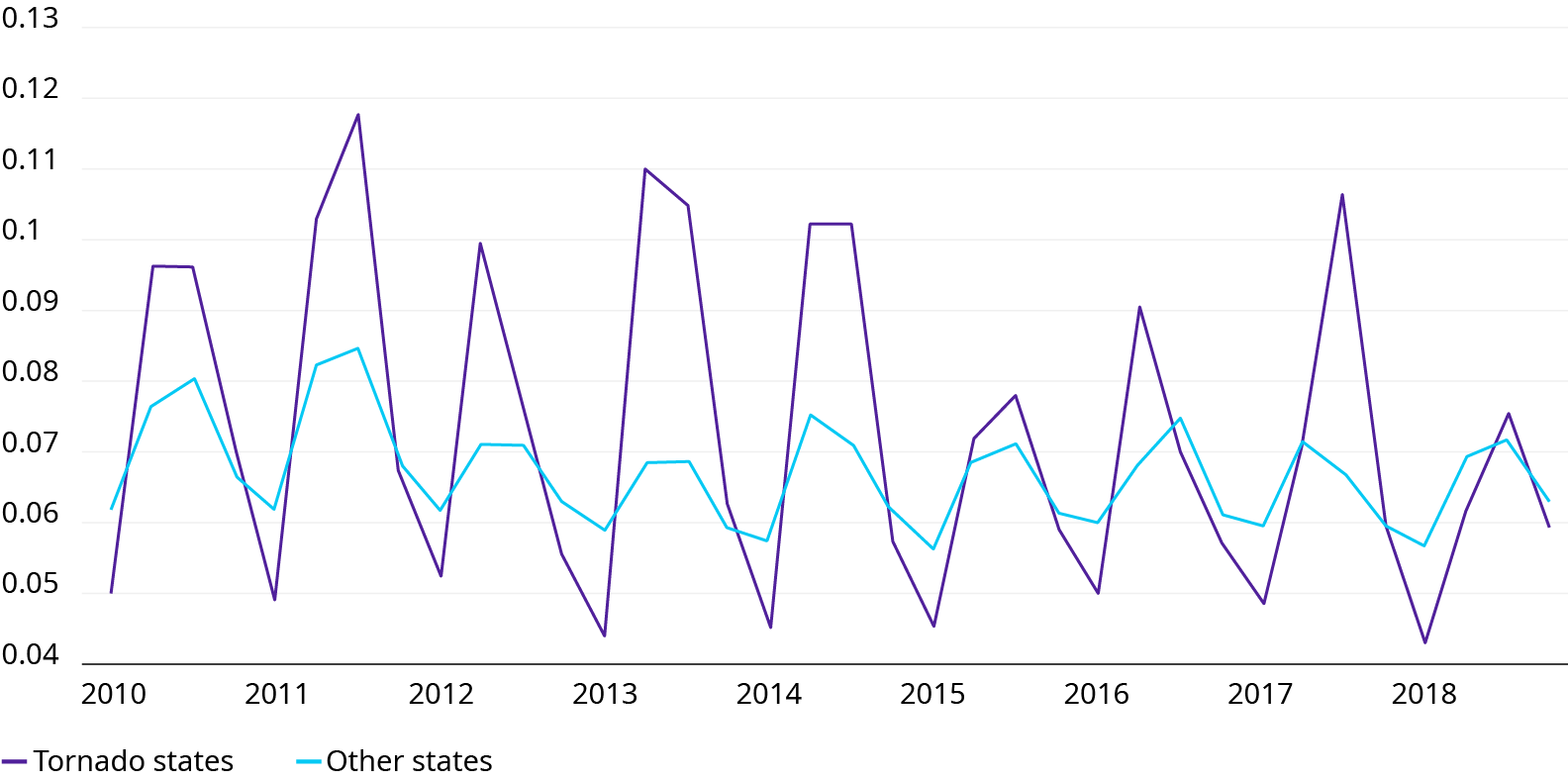

- High-tornado-risk states showed similar seasonality as high-hail-risk states. There are dramatic spikes in frequency during tornado season (see Exhibit 5).

- Wildfires also impact claim frequency, as large numbers of vehicles can be damaged during a big wildfire. The states that experience wildfires report higher average COMP frequencies than other states.

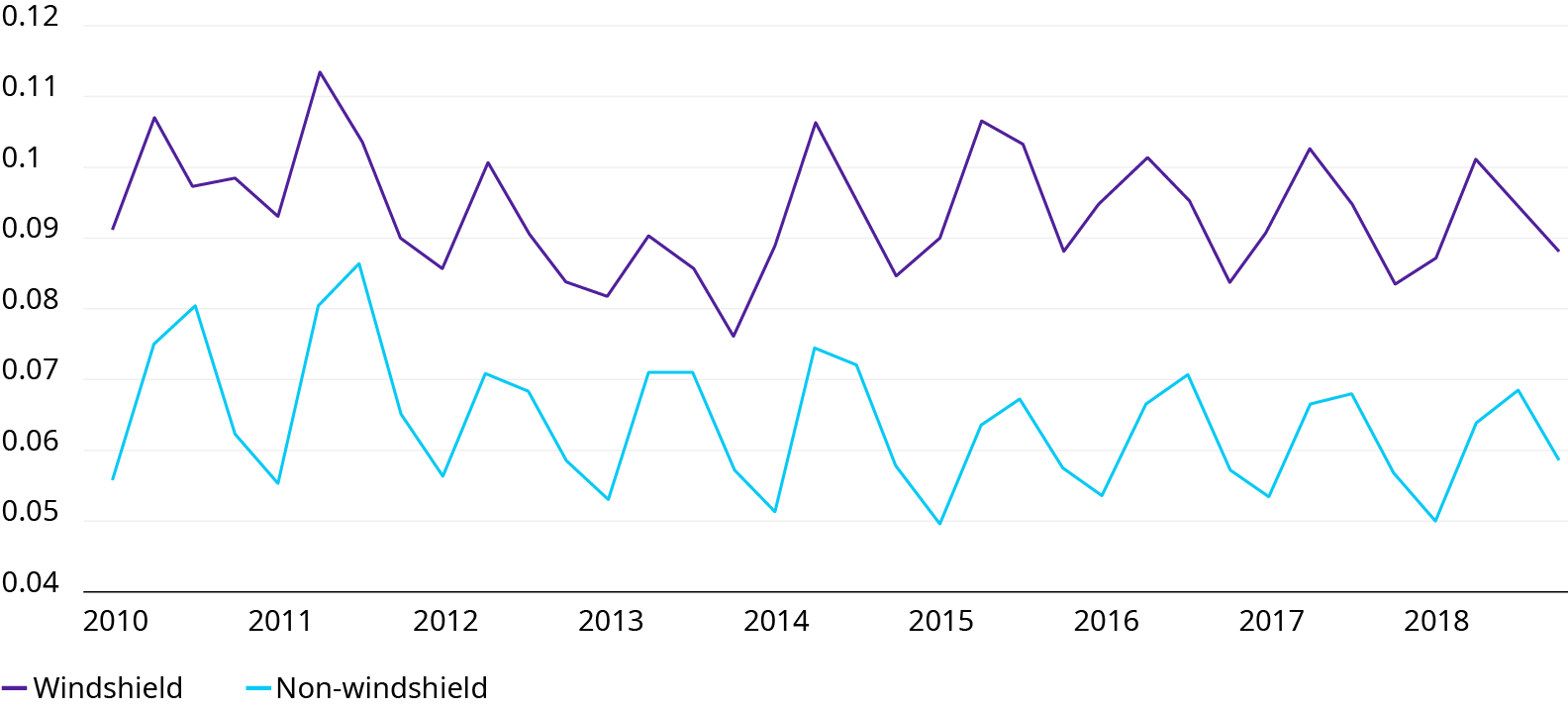

- Low-cost windshield replacement. Some states, including AZ, FL, KY, MA, NY and SC, require low- or no-deductible windshield replacement, which leads to higher COMP frequencies. States with low- or no-deductible windshield replacement have lower severity. Windshield replacement is frequent but also inexpensive.

Exhibit 4: Hail States vs. Non-Hail States Frequency

Source: Casualty Actuarial Society, Auto loss costs: Comprehensive Report

Exhibit 5: Tornado States Frequency

Source: Casualty Actuarial Society, Auto loss costs: Comprehensive Report

- Increased severity. All states, and especially those susceptible to hail, have experienced increased severity of claims. In the heatmap below for average severity in the U.S., the differences between the low severity states (AZ, ID and UT) and high severity states (IA, OK and SD) may be due to hailstorms and other severe weather.

Exhibit 6: Windshield States vs. Non-Windshield States Frequency

Source: Casualty Actuarial Society, Auto loss costs: Comprehensive Report

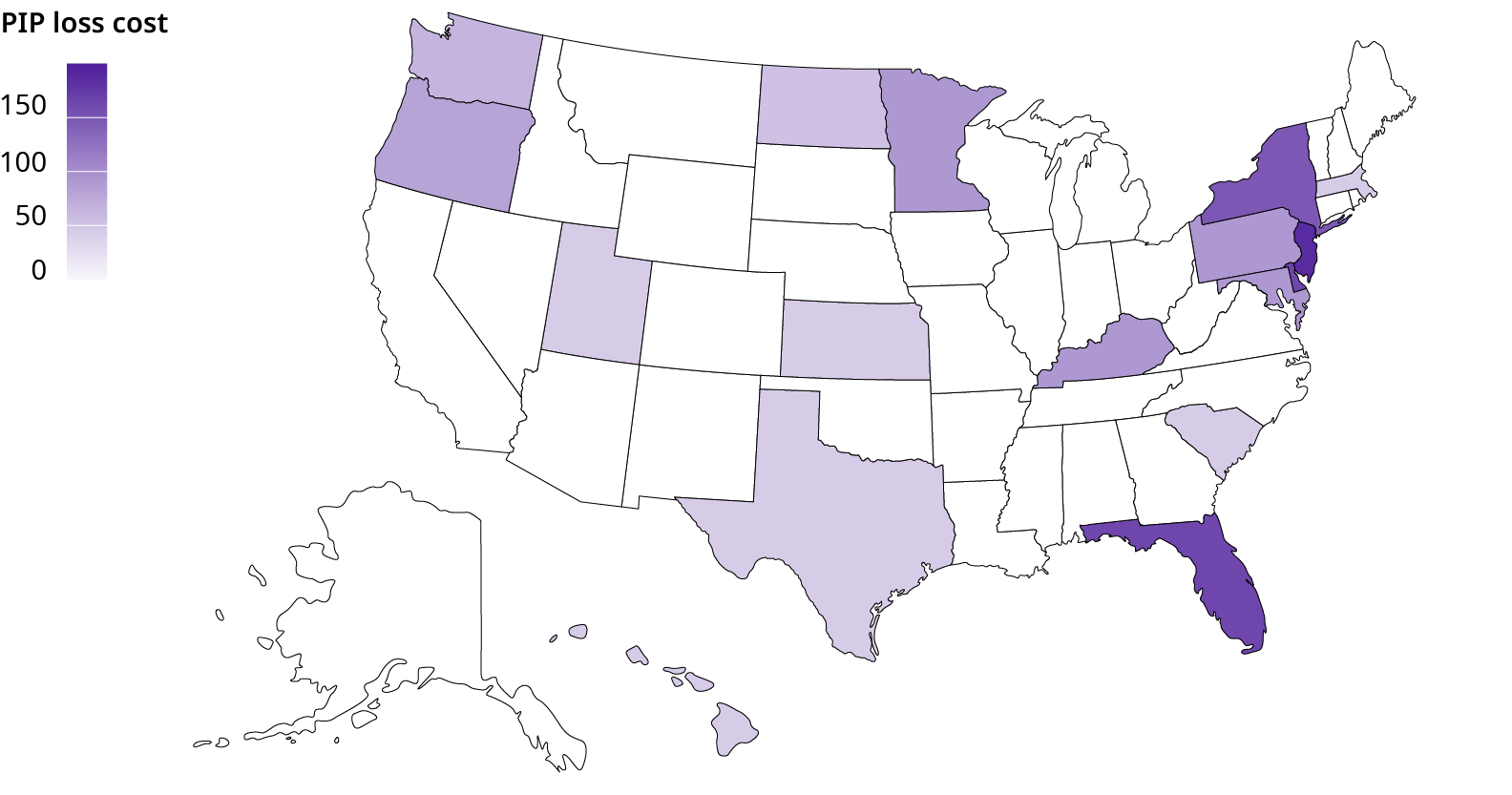

Personal Injury Protection (PIP) trends involve vehicle miles traveled per square kilometer of state land area, driver’s gender and age and verbal threshold vs. monetary threshold states

Exhibit 7: Average Severity

Source: Casualty Actuarial Society, Auto loss costs: Comprehensive Report

What it covers: PIP pays for the insured’s post-collision medical expenses regardless of who was at fault.

PIP coverage is only available in certain states. Where available, PIP coverage may be mandatory or optional. In some states, the insured can decline to file a PIP claim and instead pursue a legal case against the at-fault party only if the injury claim exceeds a monetary threshold. In other states, the insured can only sue if he/she has suffered certain types of injuries (e.g., disfigurement). This is called a verbal threshold.

In this map of PIP frequency, it’s clear that most states don’t offer this coverage. FL and MD have the highest frequency, while ND may have the lowest.

Contributing factors for PIP claims:

- Percentage of interstate roads. This is the most important factor for PIP severity and loss cost. The greater the percentage, the more negative the correlation. Here are the biggest contributing factors:

- Less turns and constant speed play a role. On interstates, people tend to drive in the same direction and generally at consistent speeds. Predictable driving could lead to less severe accidents and therefore lower loss costs.

- Percentage of male drivers age 75+ is an important factor that is positively correlated with PIP severity and loss cost. Older drivers may have slower reaction times and are more prone to serious injury. For verbal threshold states, the percentage of the male population over age 75 was the top factor contributing to PIP frequency.

- Vehicle miles traveled per square kilometer of state land area. One variable selection technique yielded vehicle miles traveled per square kilometer of state land area as the most important variable impacting PIP frequency. When all of the PIP states are analyzed together, frequency is positively related to vehicle miles traveled per land area of the state. The overall positive relationship implies that people driving more miles in smaller areas, an indicator of congestion, may increase frequency.

As shown in the below heat map, FL and NJ have the highest PIP loss costs, which may be related to their status as the only states where BI coverage is optional. With fewer at-fault drivers covered by BI insurance, more people need to file claims with their own PIP insurer, driving PIP loss costs.

- Verbal threshold vs. monetary threshold states. Different factors impact PIP frequency in verbal threshold states and monetary threshold states:

- For verbal threshold states,the percentage of elderly drivers has an impact. A greater percentage of elderly drivers increases PIP claim frequency. PIP coverage is declined in verbal threshold states for specific categories of injuries like death, dismemberment, or disfigurement. Elderly drivers may engage less in the risky driving behaviors that result in these types of injuries, resulting in comparatively more injuries falling under the verbal threshold and therefore more PIP claims filed. However, elderly drivers may have higher dollar-value claims due to the monetary cost of healing injuries at an advanced age.

- In monetary threshold states,interstate travel makes a difference. The increase in frequency of interstate travel is related to an increase in PIP claims. PIP coverage is declined after an accident if the claim exceeds a specified dollar amount, but interstate travel tends to result in more low-severity claims. With fewer accidents where PIP coverage is declined, PIP frequency may increase.

Exhibit 8: Personal Injury Protection Loss Cost By State

Note: Michigan is excluded. MI has an outlier PIP severity, and the state is excluded from the Casualty Actuarial Society’s analysis. Its no-fault insurance law mandates that the insurance company of an injured driver pays for “all reasonable charges incurred for reasonably necessary products, services and accommodations for an injured person's care, recovery, or rehabilitation” (Michigan Insurance Code Act of 1956, section 500.3183).

Source: Casualty Actuarial Society, Auto loss costs: Personal Injury Protection Report

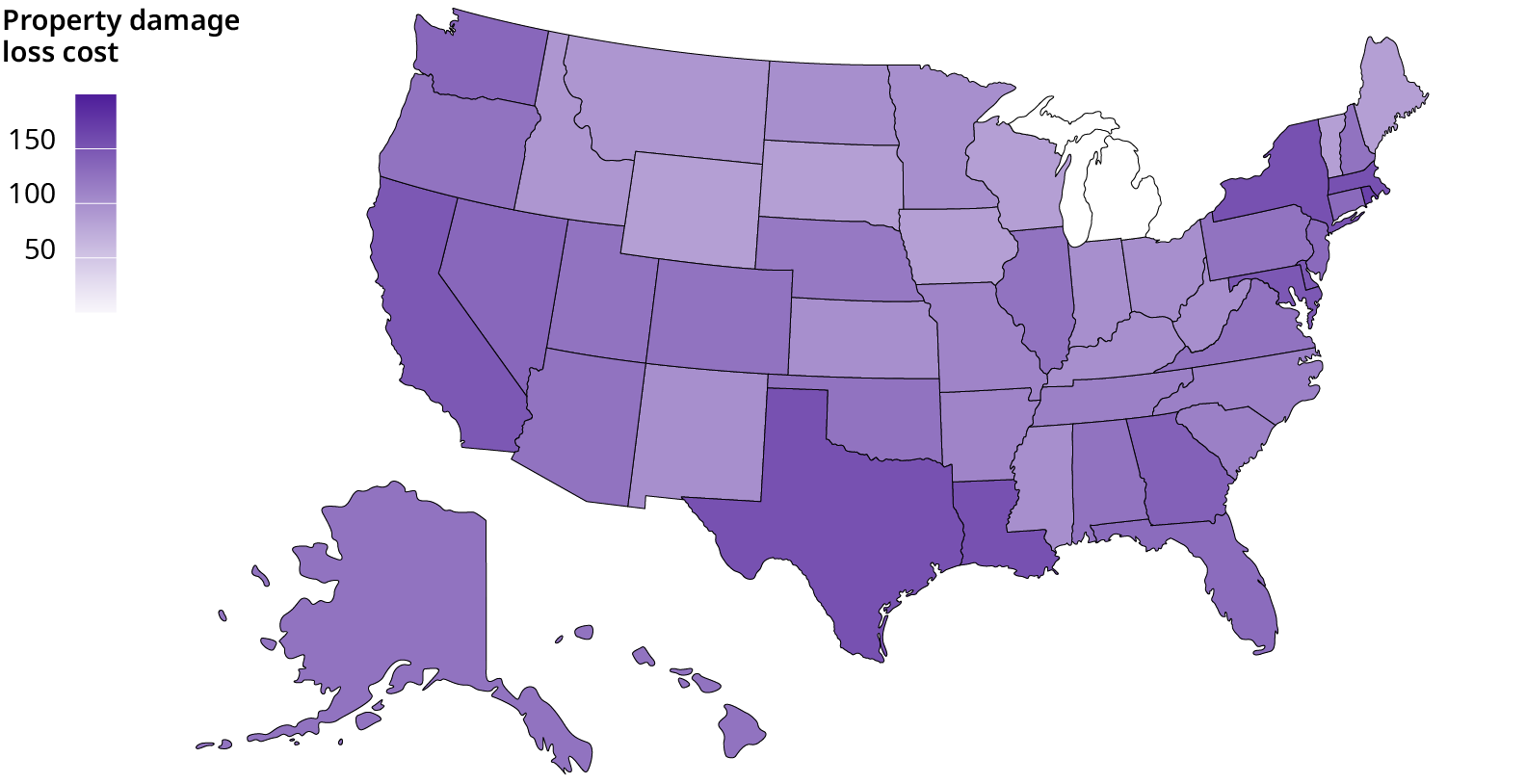

Property Damage (PD) trends are correlated with urban areas, congestion and personal income

What it covers: PD coverage in most states pays to repair damage caused to another driver’s vehicle or property after an accident where the insured is at fault.

Contributing factors for PD claims:

Exhibit 9: Average Property Damage Loss Cost, 2010 - 2018

Note: Michigan is excluded. In MI, PD applies to the damage of physical property and vehicles only if the vehicle was parked at the time it was damaged. Therefore, it doesn’t cover claims to other vehicles that were damaged while driving. However, in contrast to PIP, MI’s PD loss cost is extremely low.

Source: Casualty Actuarial Society, Auto loss costs: Property Damage Report

- Urban areas.The proportion of vehicle miles traveled in urban areas and proportion of road miles in urban areas were variables that have a strong positive relationship with PD loss cost. This implies that states with more cities and that have more cars on urban roads tend to have higher loss costs.

- Congestion. Congestion, defined as the number of vehicle miles driven per mile of road, has a strong negative correlation with PD severity. This may be because as the road becomes more congested, cars move slower, which usually causes less property damage. Accidents that happen at slower speeds tend to be less severe.

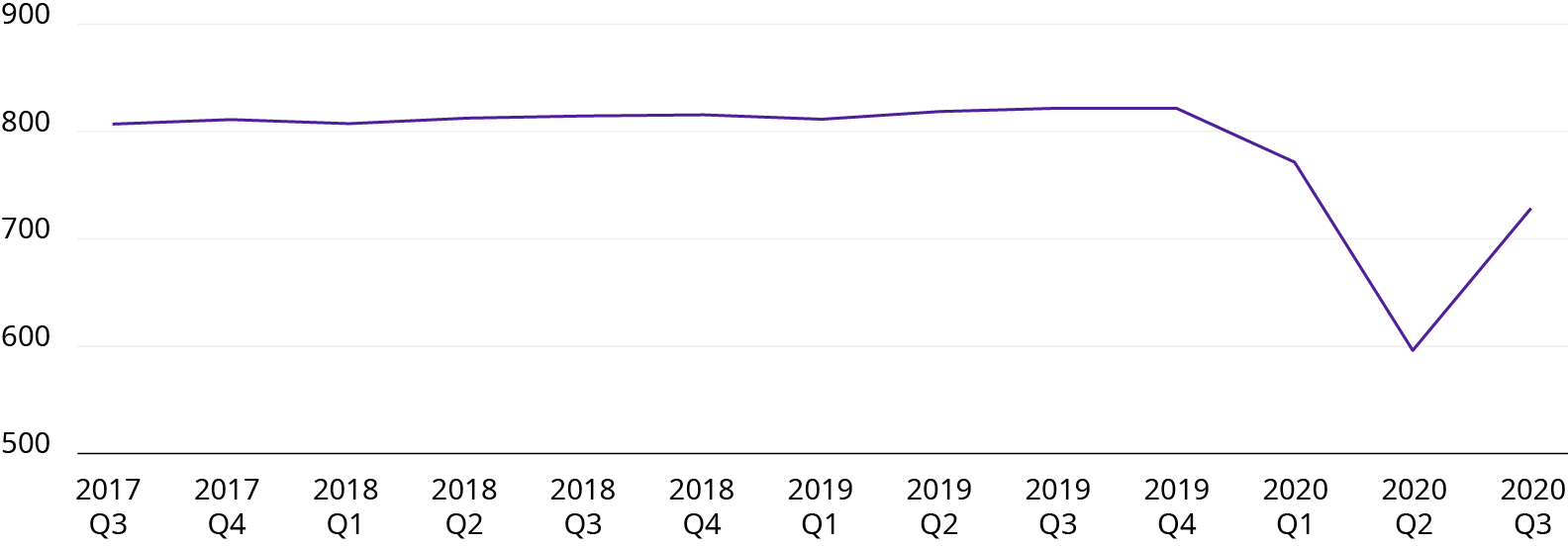

Global pandemic, legal and future trends may have a lasting impact on congestion and loss cost

What it entails: The impact of COVID-19 is still being realized, but it has clearly altered driving habits and reduced congestion, which may not return to pre-pandemic levels once the health crisis has passed.

Contributing factors for reduced congestion and increased loss cost:

- Vehicle usage. Vehicle usage was greatly reduced due to the government mandated stay-at-home orders issued in mid to late March 2020. However, even after the orders were lifted, vehicle miles have not quite returned to their historical levels. Perhaps one of the primary reasons for this change is due to companies around the nation embracing virtual work environments.

- Less congestion and riskier driving habits. Lower vehicle usage contributes to less congestion on the roads. Both personal and commercial automobile claim frequency are negatively correlated with vehicle congestion. However, according to a recent study by the U.S. Department of Transportation’s National Highway Traffic Safety Administration (NHTSA), the pandemic may have started a new trend of reckless driving behavior leading to higher claim severity. For the second quarter of 2020, the projected fatalities per 100 million vehicles miles traveled is 1.42, which represents an increase of approximately 29 percent compared to the first quarter’s projected rate. The recent trends in riskier driving patterns include more speeding, less seat belt usage and an increase of drivers under the influence of drugs and alcohol.

- Social inflation. Commercial automobile severity may continue rising due to the continued rise of social inflation (the rising costs of insurance claims resulting from increased litigation, plaintiff-friendly legal decisions and larger jury awards). In fact, the largest automobile verdict in history was recently issued to a Florida man for injuries he received in a 45-vehicle pileup in 2018 — he was awarded $411,726,608.

- Exposure reductions and premium refunds. Most lines of businesses experienced exposure reductions, which lead to premium refunds. According to AM Best, U.S. property and casualty insurers returned $8.5 billion in premiums during the first half of 2020. The most affected lines of businesses were auto-related coverages.

- Future factors. Even after the dust settles from the pandemic, it’s possible that lower commuting miles stagnate vehicle usage. Other factors such as ride-sharing services, artificial intelligence and autonomous vehicles will continue to reshape the landscape of automobile insurance. The results of which are yet to come.

Exhibit 10: Seasonally Adjusted Vehicle Miles Traveled (Billions)

Source: Oliver Wyman. Original data from www.fhwa.dot.gov/policyinformation/travel_monitoring/20septvt/