The increasing attention and ongoing development of blockchain technologies highlight the need for blockchain-native “cash equivalents” — instruments that act as liquid means of payment and stores of value in blockchain-native environments.

This demand has predominantly been met by stablecoins historically. However, the possible adoption of blockchain for payments and complex commercial transactions at scale, including sophisticated institutional activity, raises questions as to what forms of digital money will be best suited to support the transfer of value on blockchain systems.

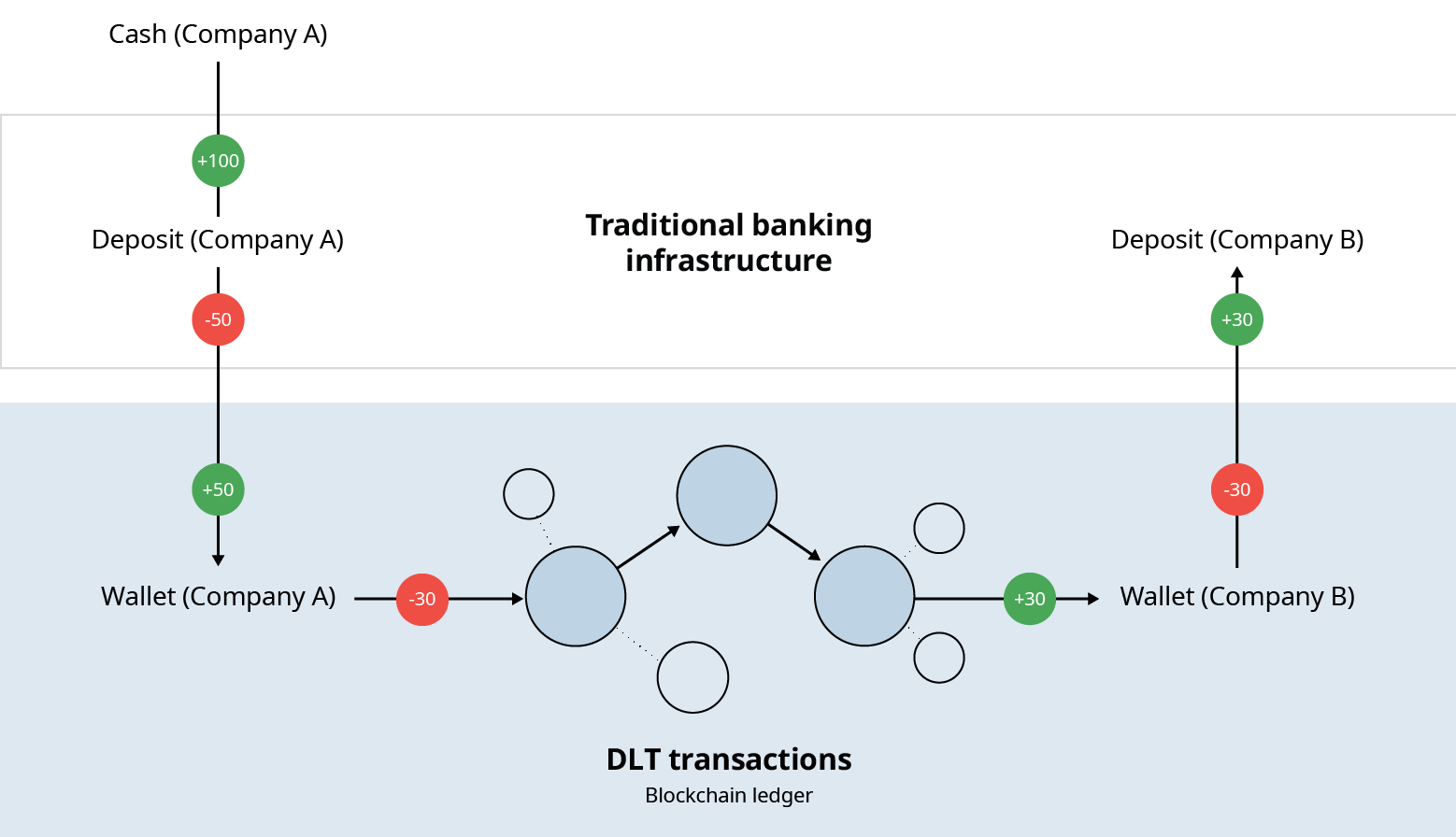

Blockchain-based deposit tokens are a promising, emerging form of digital money. They are the equivalents of existing deposits, held by a licensed depository institution such as a commercial bank, but recorded on a blockchain. From an issuing bank’s perspective, deposit tokens are simply a redistribution of deposit liabilities on the bank’s balance sheet, with no changes in the bank’s composition of assets.

Like bank deposits that make up over 90% of the money in use today, tokenized deposits can support a variety of use cases including domestic and cross-border payments, trading and settlement, and provision of cash collateral. In a token form, commercial bank money becomes a programmable instrument that operates 24/7 and can be transferred instantly, without relying on intermediaries. These technical features allow “deposit tokens” to express sophisticated payment operations and to act as collateral that travels within minutes.

As the token of a well-understood financial instrument issued by regulated institutions, deposit tokens can become a stabilizing force in the digital money ecosystem. The reliability of deposits, backed by the issuer’s safety and soundness regulation, capital and liquidity requirements, access to contingency funding through the central bank, and strong consumer protection policies mean that deposit tokens are designed to be a money instrument at scale that promotes financial stability.

The benefits of deposit tokens can be optimized by design choices that enhance their fungibility with other bank-issued deposit tokens and non-tokenized money. Users should be able to treat physical cash, non-tokenized digital money and various money-like tokenized assets as interchangeable assets with equal monetary worth and different technological properties. For deposit tokens that represent commercial bank money, this fungibility is facilitated by designs in the current banking system where central banks already act as trusted settlement institutions for private money issued by commercial banks.

Beyond economic fungibility, the success of new forms of digital money, including deposit tokens, hinges on the network effects of adoption. This will require interoperability between traditional finance systems and blockchains, interoperability across different chains and interoperability with other assets on a given blockchain.

For deposit tokens to improve the overall digital money ecosystem by creating productive linkages between traditional banking systems and blockchain, they must exist as an extension of those traditional systems, both in design and in regulation. Banks, policy makers and regulators alike should consider the unique risks and benefits of each new form of digital money and recognize the distinct characteristics of deposit tokens.

Written in collaboration with Onyx by J.P.Morgan authors: Naveen Mallela, Basak Toprak, Nelli Zaltsman, and Mario Tombazzi.