Private Equity Can Bolster Emerging Obesity Care Models

No drug category garnered more attention over the past couple of years than GLP-1s. Predominately used to manage type 2 diabetes, GLP-1s surged in popularity following promising results from clinical trials showing that they could be used for weight loss. Those results prompted the Food and Drug Administration in June 2021 to approve Novo Nordisk’s Wegovy for chronic weight management in certain adults, the first time the agency had taken such action in nearly a decade.

Since that decision, the use of GLP-1s to fight obesity has skyrocketed. The FDA in November 2023 approved a second drug, Eli Lilly’s Zepbound, for chronic weight management. And such drugs as Ozempic, Trulicity, and Victoza are being used off-label for weight loss. IQVIA reported a 41% annual growth rate between 2018 and 2022 for spend on GLP-1s. Various projections suggest the market could surge to between $70 billion and $100 billion over the next decade, with Novo Nordisk and Eli Lily expected to control more than 90% of the market.

While more studies are required to understand side effects, and steps need to be taken to address access and cost, the future market for anti-obesity drugs is immense and private equity firms are taking notice. The increasingly competitive landscape was a hot topic at this year’s J.P. Morgan Healthcare conference. We think private equity can play an important role in aiding start-ups and more established players build effective GLP-1 strategies.

Two models emerging for GLP-1 use

Demand for GLP-1s and similar diabetes and weight loss drugs soared over the past two years. The total number of GLP-1 prescribing providers rose an astounding 228% between July 2020 and May 2023, according to IQVIA. As usage climbs, two distinct care models are emerging: prescription only and prescription coupled with lifestyle intervention.

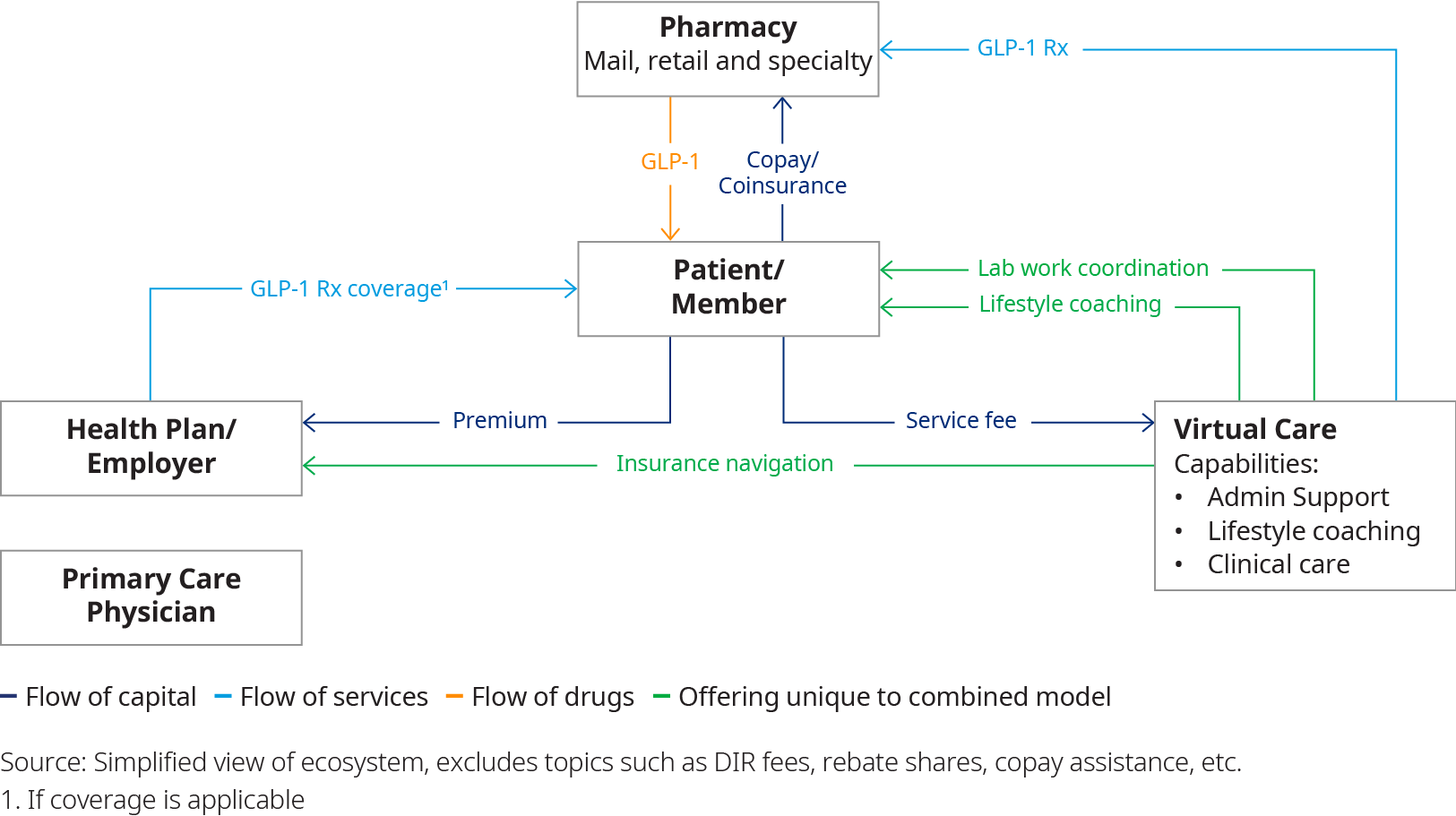

The prescription only model falls to physicians to manage but is not preferred since a holistic approach is recommended for treating obesity. Hybrid pharmaceutical and lifestyle intervention support models are more robust and provide an end-to-end patient experience. The model is typically built on a virtual care platform.

Key players in the hybrid prescription and lifestyle intervention market range from new entrants in the early-seed stage of funding to established titans of the weight loss industry investing in build-and-buy expansion strategies to compete.

WeightWatchers, for instance, acknowledged the need to dramatically overhaul its strategy given the rise of GLP-1s. CEO Sima Sistani told CNN that the company “got it wrong” and is now embracing the use of weight loss drugs. It also acquired telehealth platform Sequence in a move to adapt to consumer needs. Meanwhile relative newcomers like Everlywell, Found, and Noom captured consumer interest by coming to market as digital-first platforms. And established care providers like Teledoc added prescribing GLP-1s to their services.

Telehealth models and the impact on private equity

The rise of hybrid obesity care models is due in part to greater consumer acceptance of and expectations for virtual care. Close to 5% of medical claims were for telehealth services as of September 2023, up from 0.2% in January 2020, according to FairHealth. The allure of combining virtual care with weight management has sparked interest among private capital investors, who have taken note of high valuations in this space. Prominent examples include: Found’s $600 million valuation in the fourth quarter of 2022, WeightWatchers’ $132 million acquisition of Sequence, and Madryn Asset Management buying a 70% stake in Calibrate.

Going forward, success in this market will be rooted in two elements: operational excellence and market outreach to the consumer. Private equity is uniquely positioned to provide the framework and foundation building those out. Aside from coverage and cost, key concerns for patients in this ecosystem are long-wait times, unresponsive providers and clinicians, and shortages of GLP-1 pharmaceuticals. Investors can impact those factors in a variety of ways:

- Providing the capital required to source the appropriate staff to handle rapidly growing patient volumes. This will help reduce wait times for patients, improve throughput, and ensure clinicians have appropriate time to address patient concerns.

- Source best-in-class leadership to support in operational design and day-to-day management. This includes investing in white-glove offerings to differentiate in a crowded market from companies without the capital to match. Two key services are shipping and covering costs for at-home lab tests to accelerate the onboarding and prescription process while maximizing convenience for the consumer. Investors can also help expand insurance support capabilities like navigating communication with employer benefits managers and working through the prior authorization process. Assistance here will become increasingly important as an estimated 43% of employers plan to cover GLP-1s for weight loss in 2024, up from 25% in 2023. Broader coverage, however, will take time. Federal law currently bars Medicare from covering weight loss drugs. If that changes — legislation was introduced in 2023 — and Medicare adopts coverage, private insurers would be sure to follow.

- Invest in aggressive marketing to corner the market. Member growth will be dependent on consumer choice between relatively comparable companies. Getting in-front of consumers to capture share will require significant capital to support.

The race to capture market share in the hybrid obesity care space will intensify in the near term. Companies and investors that act now will have the benefit of building an infrastructure that can accommodate new drugs as they come online and adjust for evolving patient preferences.