Medicare’s Latest Innovation? Moving Cities to Managed Care

US healthcare’s last decade was one of transformation, disruption, and experimentation. There was debate around healthcare reform. Consumer-centric technologies were quickly adopted. Providers consolidated. Sites of care shifted. Value-based models became more of an industry focus. Then, as we turned the corner into a new decade amidst budding change, COVID-19 shocked the world.

As we look to innovations over the next decade, one development capturing our attention is the Geographic Direct Contracting Model, or the Geo DC Model, launched in parallel to the existing Professional and Global DC models. Direct Contracting is shaking up the Medicare alternative payment landscape, presenting powerful opportunities to accelerate the shift from volume to value in Medicare.

CMS’ Push Towards Value Continues

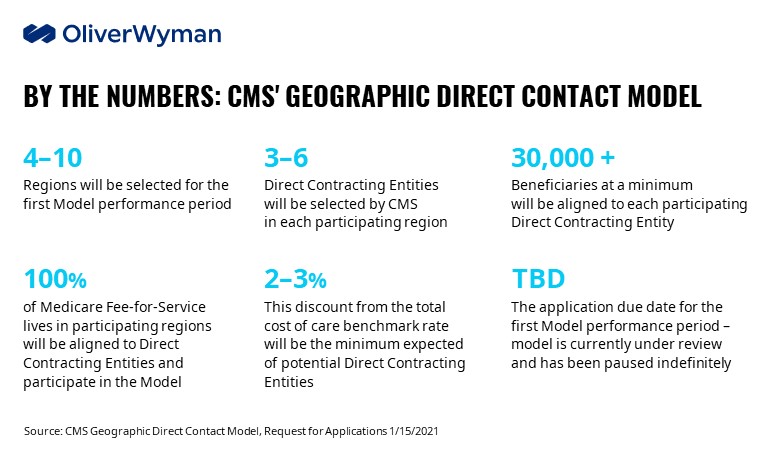

The Centers for Medicare & Medicaid Services (CMS) has continued its push towards value in Medicare by introducing the Geo DC Model. This follows the previously released Medicare Global and Professional Direct Contracting options, which similarly offer a broad range of industry players the opportunity to manage Original Medicare, or Medicare Fee-for-Service (FFS) lives through an influence model. The Geo DC Model seeks to align all original Medicare beneficiaries in targeted geographic areas to Direct Contracting Entities (DCEs) that are responsible for managing total cost of care (TCOC) without imposing additional cost-sharing or care restrictions. Although all three Direct Contracting options could potentially be active in 2022, it’s not yet clear how CMS plans to coordinate the models going forward.

Medicare Direct Contracting represents a fundamental shift in the management of Medicare FFS lives, transitioning from unmanaged care to an innovative model that aligns incentives for member management and cost accountability outside of traditional managed care constructs. The Geo DC Model is differentiated in its scale: all competitors in the Medicare value chain – whether providers, insurers, legacy players, or innovative upstarts – that operate in selected regions will be impacted by the Model and will require a differentiated approach to build and sustain competitive advantage.

CMS Outlines Target Regions for Participation

In its recent Request for Applications, CMS identified ten target regions for potential inclusion in the Geo DC Model.

Opportunities for Different Industry Players

The Model will transform the Medicare landscape, presenting different growth opportunities and competitive considerations for each industry segment:

Established Payers: Geo DC offers established health plans novel access to the Medicare FFS population – an opportunity to triple its Medicare membership base and improve Medicare Advantage (MA) penetration over time by converting beneficiaries to MA. Model per-patient economics may also be more favorable in the DC Geo Model than in MA - largely driven by reduced selling and general and administrative (SG&A) costs – though payers will need to effectively manage TCOC through the levers prescribed in the Model to capitalize on these savings.

Upstart Payers and Enablement Companies: By aligning 100 percent of Original Medicare patients, the Model offers an opportunity to achieve scale rapidly. These conditions reduce barriers to entry and enable players with limited experience but innovative approaches to secure a foothold.

ACOs and Risk-Bearing Providers: The Model enables ACOs to expand their risk portfolio and build operating efficiencies, offering additional negotiating leverage and population health insight as they take on additional lives. The Model rewards risk-bearing providers who have already invested in health plan capabilities (care management, member engagement, and downstream provider network management) to serve a broader range of Medicare beneficiaries, including new patients untouched by the ACO historically.

Hospital Systems: The Model could grow or erode the currently unmanaged Medicare lives that most hospitals depend on for contribution margin. Contracting as Preferred Providers to local DCEs will drive additional volume with and enhanced benefits such as patient transportation and remote monitoring.

Risks to Consider

Alongside these opportunities, Geo DC Model participation (and nonparticipation) presents risks. Entities that forgo participation may experience declining volume as Medicare patients are navigated to Model participants. Functionally, the promise of access to FFS lives/risk must be balanced with the challenge of managing complex health care needs and TCOC, while establishment payers must manage the impact of innovative payment models on the fundamentals of their MA business.

Not participating in the first performance period has significant implications. With a three-year bid cycle, players that opt-out will be stuck on the sidelines while competitors build inroads with the Original Medicare population, invest in care management capabilities, and strengthen "dance partners" and provider relationships.

If Successful, the Model Could Disrupt the Traditional MA Landscape

The Model presents opportunities for legacy MA players and upstarts alike to develop innovative partnerships between DCEs, provider organizations, and enablement firms. New market entrants can leverage the Geo DC Model to move upstream in the Medicare value chain. For established players, the Model has the potential to break up the hegemony that traditional MA powerhouses enjoy in many markets, driving these firms to offer new and differentiated value.

On March 1, 2021, CMS provided an update on the Model, stating: “The Geographic Direct Contracting Model is currently under review and CMS looks forward to sharing additional information when available.”

Even if the Geo DC Model is delayed or canceled, the evolution of Global and Professional Direct Contracting options is inevitable given the urgency around providing better, more coordinated care for Medicare FFS members while managing medical spend.

Closing Thoughts

Healthcare’s last decade was one of constant change and innovation. We envision the next decade will mirror the last in this regard as consumer-centric trends continue and ambitions to realize value-based care manifest. Medicare FFS members will continue to be at the forefront of value-based care innovation as stakeholders across the industry explore the potential of Medicare Direct Contracting.