60% of Health Insurers Don't Offer Smoking Cessation Programs

Editor's Note: The following ideas and "Insurer Perspectives On Smoking Risks" report were originally published here on OliverWyman.com.

There are more than a billion smokers in the world today, and a billion people could die of tobacco-related causes this century. Smoking is the leading preventable cause of death and the second leading risk factor for attributable disease burden worldwide, accounting for 148.6 million disability-adjusted life years in 2015. Besides health harms, smoking is also responsible for nearly $2 trillion in economic consequences due to lost income and healthcare expenses.

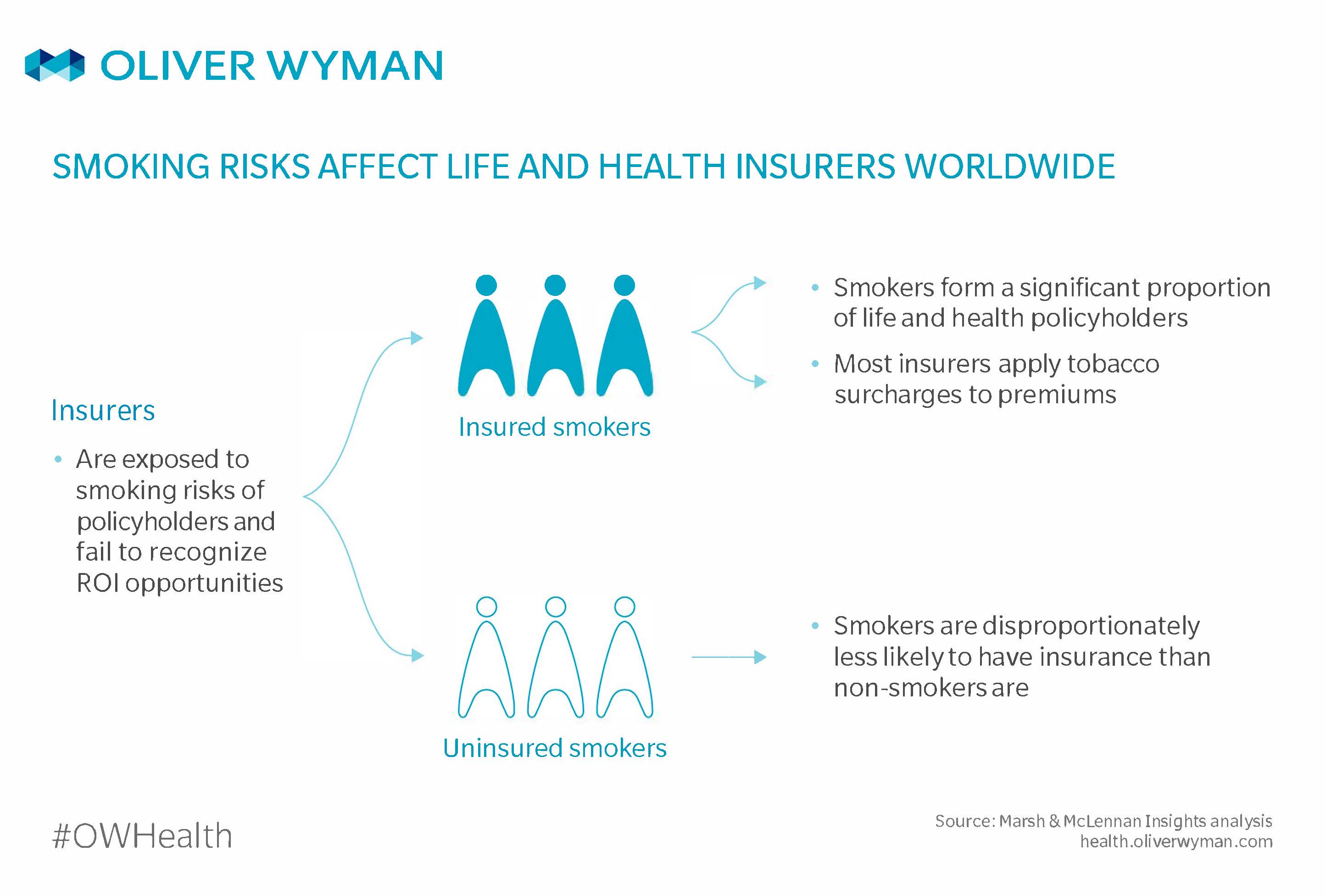

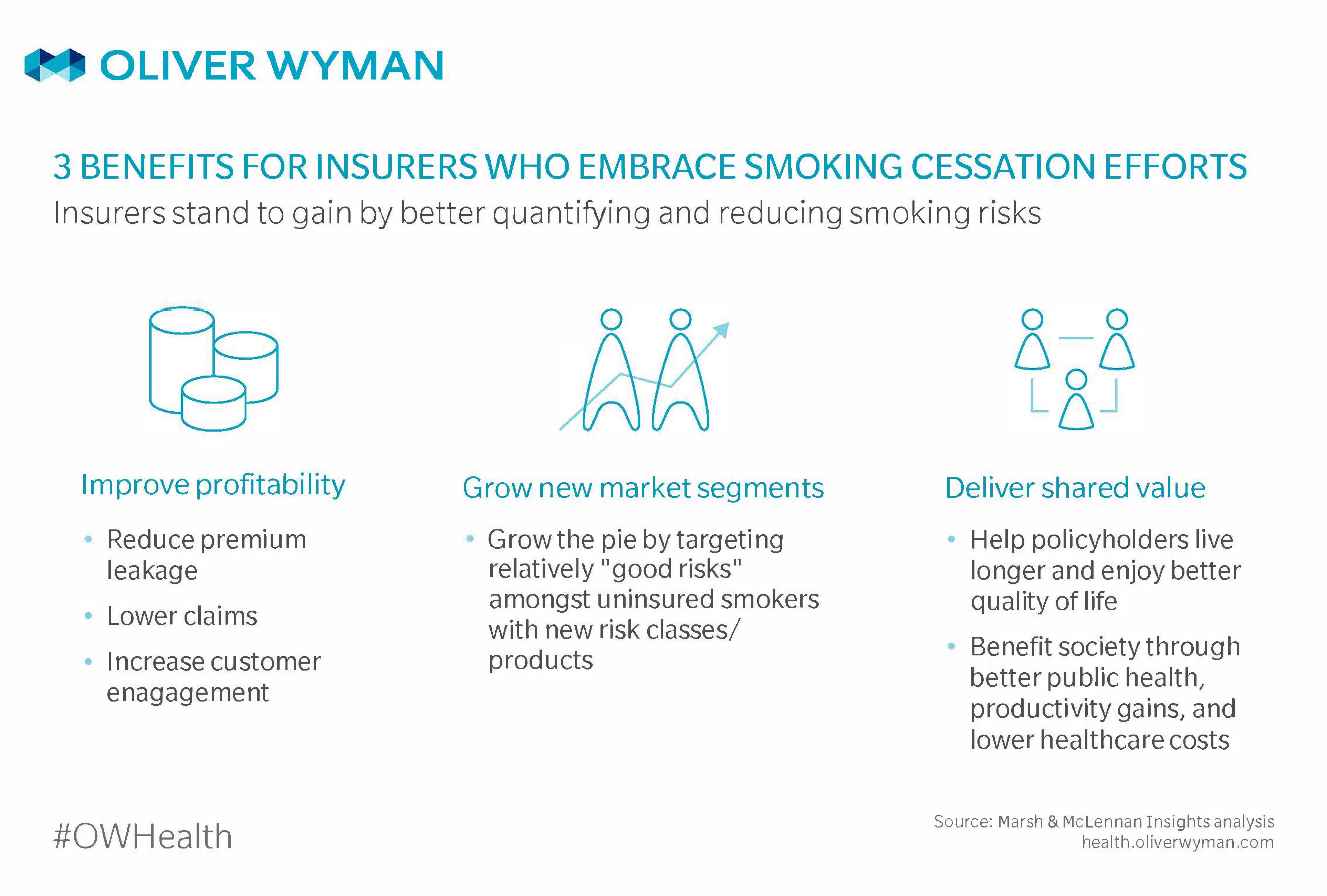

This global health challenge remains relevant to the insurance and reinsurance industries worldwide. Tobacco risks and regulations affect underwriting, pricing, claims, and reserves in all countries. Smokers account for a significant proportion (10 to 15 percent) of life and health insurers’ books of business, and insurers are exposed to the mortality and morbidity effects of tobacco. Smokers are disproportionately less likely to be insured, and insurers may be missing out on relatively “good risks” within a spectrum – such as those who are motivated to stop smoking but are currently priced out of the market. By improving how they assess and influence tobacco-related risks, insurers can improve health and quality of life for millions of people, improve profitability through reduced claims and reserves, and grow new market segments.

The Case for Re-Thinking Current Practices

Based on a global Marsh & McLennan (MMC) survey and interviews with insurers and reinsurers, the Insurer Perspectives on Smoking Risks report (funded by a research grant provided by the Foundation for a Smoke-Free World) finds that insurers have not radically changed their approach to tobacco risks in decades. Typically, insurers try to spot smokers at the application stage, charge them higher premiums (particularly for life insurance), and sometimes provide incentives or programs to help policyholders stop smoking.

However, tobacco products, regulations and patterns of use continue to evolve – and with them, users’ risk profiles. While cigarettes remain the dominant tobacco product, newer products such as e-cigarettes and heated tobacco — collectively termed alternative nicotine delivery systems (ANDS) — are becoming popular: for example, e-cigarette use is estimated at four to six percent of the population in the United States, United Kingdom, France, and Belgium. These products have divided opinion among public health experts and policymakers, with no consensus on how to regulate them.

Except in the US where teen use of e-cigarettes is widespread, ANDS use is generally limited to current and former smokers – either short-term use to quit tobacco and nicotine products entirely, or long-term use replacing cigarettes, or dual use to cut down on cigarettes. In terms of implications for individual risk profiles, early evidence indicates the following harm continuum: abstinence < ANDS < cigarettes. ANDS are more harmful than never using tobacco/nicotine or quitting entirely. They seem to expose users to fewer known toxic chemicals than cigarettes and may be less harmful for current smokers. It is too early for conclusive evidence on long-term morbidity and mortality impacts, and risks vary widely across individual products in the category.

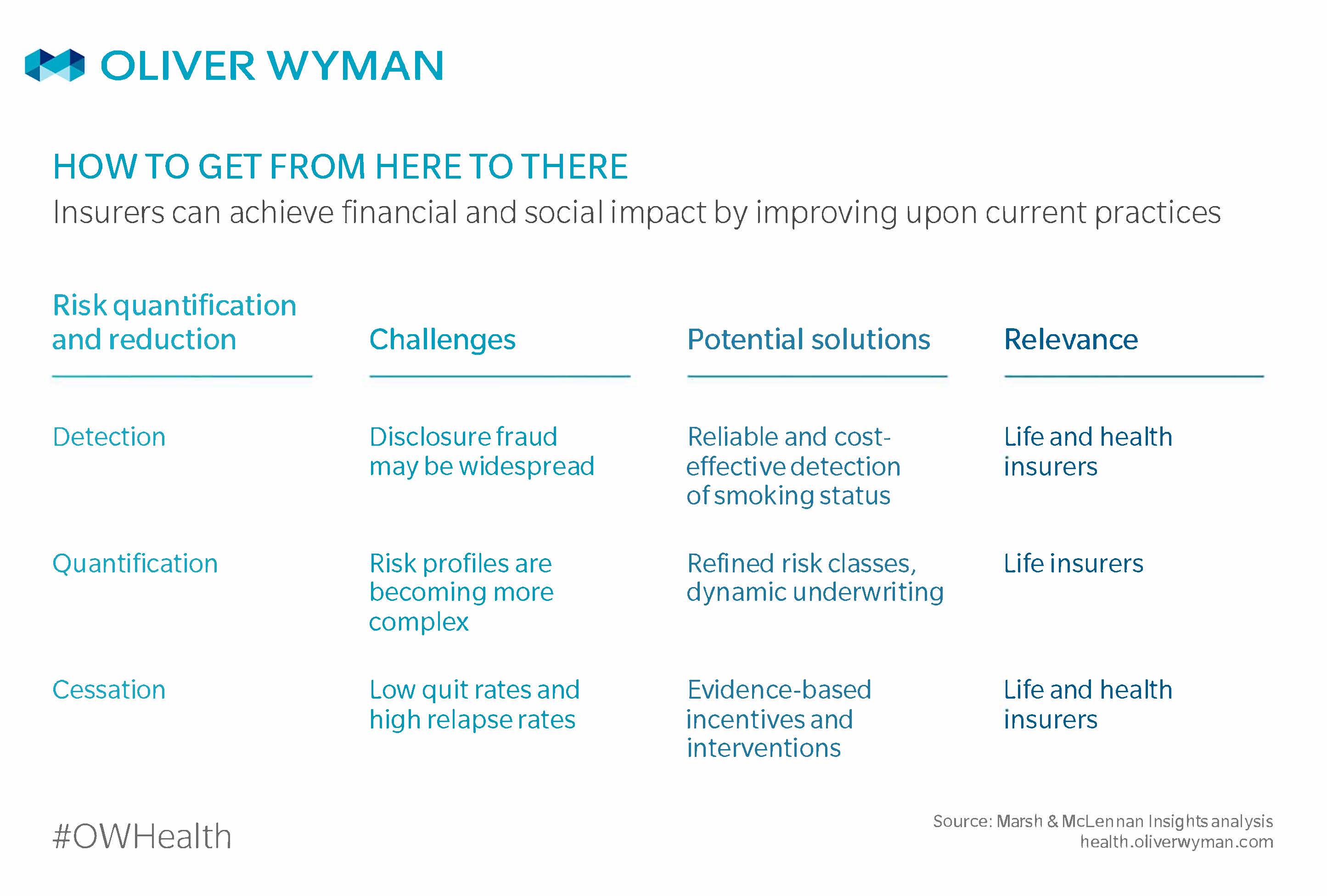

In a changing context, current insurer practices are looking far from perfect. Insurers believe that disclosure fraud may be widespread; their risk classifications and pricing remain binary while risk profiles are becoming more complex; and they are doing very little to measure and improve smoking cessation efforts. Emerging technologies and solutions present potential solutions for the industry.

Improve Detection of Smoking Status

Most insurers and reinsurers consider the recent use of any tobacco or nicotine product to be smoking. To identify smokers, almost all insurers in the MMC survey rely on applicants to declare their history and frequency of tobacco use. Insurers verify smoking status for a sub-set of applicants through laboratory tests for cotinine (a metabolite of nicotine). “Smoker amnesia” is among the challenges of the current detection process: 20 to 50 percent of smokers declare wrongly. Also, the cotinine test delivers up to 50 percent false negatives (like if it concludes wrongly that a smoker is a non-smoker, such as when he/she skips tobacco use for a few days), and insurers are increasingly waiving tests to accelerate underwriting for applicants whose age and health history do not raise concerns.

Incorrect identification and unreliable verification of smokers leads to inaccurate underwriting and pricing of smoking risks. This results in premium leakage and lower profitability for insurers, and customers risk voided policies or reduced claims. Both miss opportunities to support smoking cessation and improve health outcomes. To detect individuals’ smoking status more accurately, insurers can consider the following solutions:

- Reduce disclosure gaps by asking intelligent questions that make it easier to be truthful and accurate, and harder to lie. The Reinsurance Group of America increased tobacco use disclosure from 35 to 52 percent by asking a non-binary question (“When did you last smoke?”). This let applicants feel more comfortable about their behavior and answer honestly, instead of in a way that felt socially acceptable.

- Improve risk triage through predictive analytics. Smoking propensity models use broad data sets — including conventional and voice elements — and advanced analytics to flag potential tobacco use and help insurers identify candidates for lab testing.

- Adopt more reliable and cost-effective tests when they become available. Insurers should keep tabs on biomarker innovation to find consistently accurate tests that are easy to administer and can distinguish between different products.

Assess Tobacco Risks in More Refined and Dynamic Ways

Seventy-six percent of insurers in the MMC survey treat smokers differently in underwriting and pricing, more commonly for individual life and health products than for group products. Most insurers treat all tobacco intake methods the same, resulting in binary risk classifications (non-smokers versus smokers) and up to four times higher premiums that do not differentiate by product type, frequency, or duration of use. This limited sophistication of risk assessment constrains insurers as tobacco risks become more complex. Insurers can respond to this challenge in several ways:

- Develop tiered pricing to reflect the relative risks of different products and patterns of use, as evidence emerges of their impacts on health and it becomes possible to validate their use.

- Personalize tobacco rates based on behavioral data, such as product types, frequency and consumption levels tracked by smart products or apps. A similar pay-as-you-use approach facilitated by telematics is transforming car insurance into tailored “risk pools of one”.

- Use dynamic underwriting and adjust pricing to reflect how risks change over time: for example, lower premiums for policyholders who quit smoking. Vitality, as just one example, uses customers’ lifestyle and health data to adjust premiums, reflecting risks more accurately and nudging healthier choices.

Measure and Improve Smoking Cessation Interventions

Most insurers take a passive approach to reducing smoking-related risks: 60 percent of the MMC survey respondents neither offer cessation programs or incentives, nor collect data on outcomes. What is not measured is not being improved, and there is an urgent need for more evidence-based and data-driven approaches:

- Offer effective interventions such as combined financial incentives and free cessation aids, which according to recent evidence, boosts quit rates and keeps participants engaged.

- Track uptake, success, and relapse rates. By learning from good and bad outcomes, insurers can understand which measures work and improve upon them.

- Apply nudges based on behavioral economics principles. For example, Manulife draws on the endowment effect by offering non-smoker premiums to smokers for the first three years and then raising premiums substantially if policyholders do not quit smoking by then. Digital health partnerships can help insurers apply such concepts to increase customer engagement, influence behaviour change, and reduce claim costs.

Some of these solutions are easy to implement, some will require investment in capabilities or partnerships, and some need more research or evidence but have the potential to transform the way insurers quantify and manage smoking risks. Insurers should monitor the science as it evolves and scrutinize innovative solutions as they emerge from incumbents and new entrants.