Healthcare in 2030: Five Mindsets Holding Incumbents Back

The healthcare industry’s progress solving major issues – cost, outcomes, experience – can perhaps best be described as incremental. Medical cost still outpaces inflation, increasing pressure to cut costs. The value chain remains static, as payers continue to own the bulk of lives, and provider-owned health plans are niched. Sure, value-based care adoption presses onward – led by the Centers for Medicare and Medicaid Services (CMS) – but most adoption efforts, focused on healthy or at-risk consumers, are still reimbursed via fee-for-service (FFS) payment models. Despite some notable progress, healthcare continues to lag most other industries in its inability to engage consumers, thereby putting other industries at the forefront of innovation.

But change may finally be shaking up the healthcare industry, as recent announcements of large deals and partnerships have shifted healthcare’s status quo conversations. Despite significant uncertainty, change seems more and more likely to come from outside of healthcare. And whether these outside “disruptors” end up changing the game amidst a seemingly unmalleable industry, the bottom line is most incumbents could have done more. The question is: What missed opportunities will incumbents look back on over the next decade or so and be kicking themselves for not having taken advantage of, and how and why could they have done more?

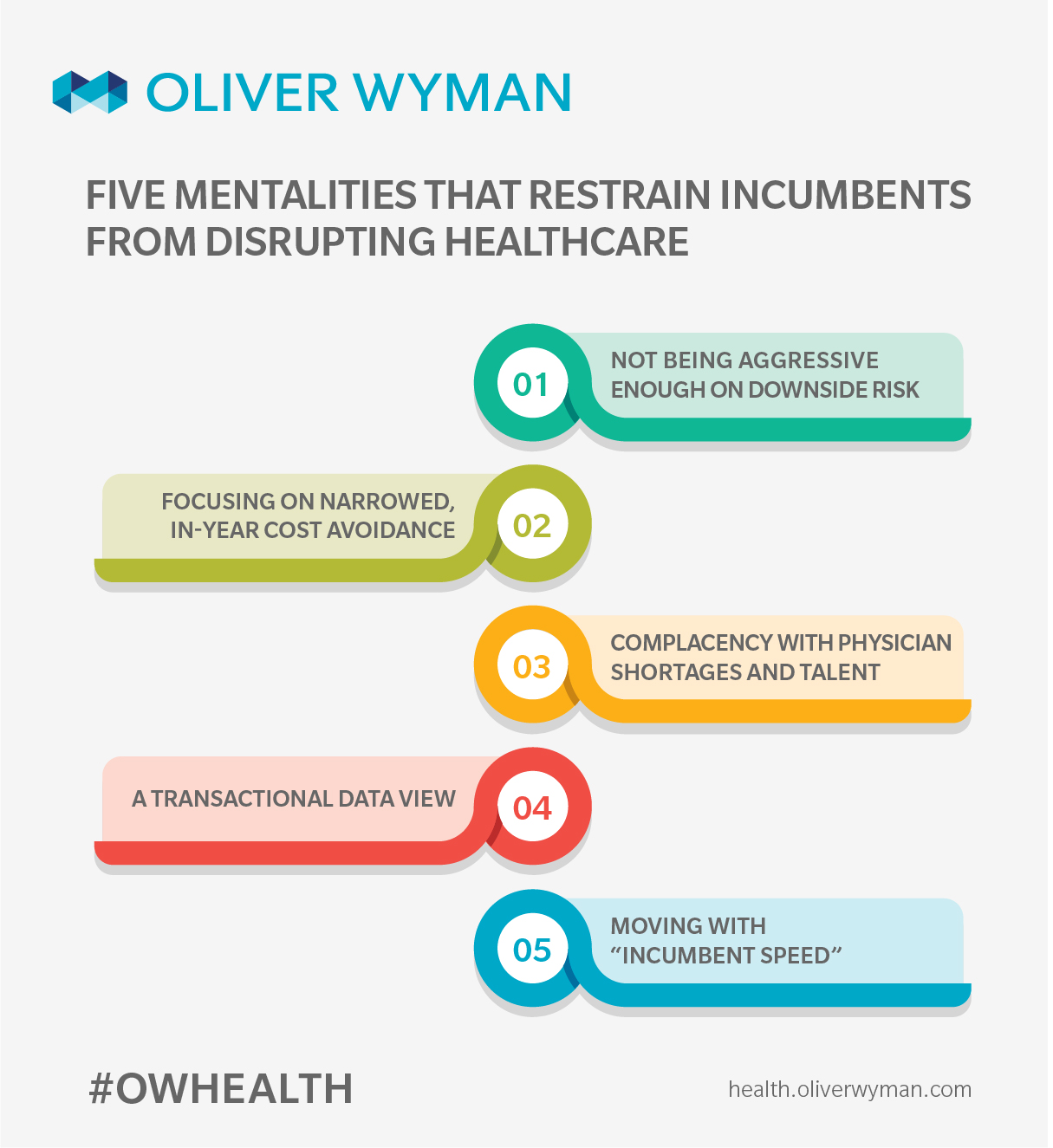

Perhaps it all comes down to changing the incumbent mindset. Here are five mentalities that hold incumbents back from disrupting healthcare, where had the industry moved more quickly or flipped the script with a bit more strategic design, healthcare’s disruption would be more likely to come from inside, not outside.

1. Not being aggressive enough on downside risk.

While there are visible examples of providers taking risk in support of moving toward value-based care, providers as a whole aren’t likely to embrace downside risk. Shared savings programs – driven both by commercial payers and CMS – lead to limited transformation, a view of value-based care as a contracting mechanism, and the lack of a plan to migrate whole books of business into new models. Going forward at current pace, CMS-based adoption continues. Complex conditions’ care models proliferate. Select population and procedures are capitated / bundled. And FFS reimbursement is the norm.

2. Focusing on narrowed, in-year cost avoidance.

There is fear of churn – from insurers, from employers, and from providers. This mindset prevents a longitudinal view of consumer health. The healthcare industry’s ability to shift from responding and repairing, to planning, predicting, and preventing is requisite to impact the health of constituents and the nation’s cost of care. Yet industry incentives to do so are not obvious; actions focus on ROI-proven activities that drive more near-term cost savings. In-year cost avoidance is obviously positive and necessary, but insufficient to disrupt an industry where poor choices and behaviors drive long-term cost.

3. Complacency with physician shortages and talent.

Physician shortages have grabbed headlines for years, yet little has been done to address this problem. Further, other looming talent challenges will compound this issue as other levels of clinical expertise become in short supply (like skilled nursing facilities). The healthcare industry is massively underprepared for new required skill sets, especially as more care moves out of the physician’s office and into the home. Technology solutions – many of which may come from outside the industry – will help, but are still nascent and don’t yet address up-and-coming business models.

4. A transactional data view.

Those in healthcare now realize the incredible importance of data to effectively engage individuals in their health and help manage their care. However, even with recent adoption of technologies like Fast Healthcare Interoperability Resources (FHIR), healthcare still largely operates in closed systems of information initially built to facilitate financial transactions. These closed systems are breaking down in isolated use cases, but are far from gone, and persist for both technical and business reasons. Additionally, these silos have yet to incorporate more “whole life data” that will strengthen engagement.

5. Moving with “incumbent speed.”

Incumbents appear slow to anticipate or respond to new disruptive business models, and they do not seem to see their customers' economic power. They clearly are reluctant to risk their current (successful) models. Meanwhile they lag in the capabilities and culture to pilot aggressively or scale successfully and purposefully. In healthcare, unlike other industries, the multitude of constituencies exacerbates complex legacy decision-making protocols.

Healthcare has enough waste in its system and pent up frustration from all parties. Yes, there are exceptions and bright spots all over the healthcare landscape, but even when successful, scale is limited. The disruptors can no longer be ignored. Too often, it’s believed outsiders are too far away to affect the system. Claims that those disruptors who don’t know healthcare also don’t know how to make money in healthcare won’t keep outside disruption at bay. It may be easier to disrupt than is anticipated – if there’s embracement of a new mindset.