New Survey: CSR Uncertainty Looms Large Over Payers

With the June 21 ACA premium rate-filing deadline just a week away, a new survey by Oliver Wyman Actuarial Consulting reveals that US health insurers are approaching 2018 with a plan A and a plan B and they are seeking clarity around key policy issues.

In particular, the question of whether the Trump administration will continue funding cost sharing reduction (CSR) payments looms large over the market. Survey responses indicate the administration’s decision will have a significant impact on 2018 rates and payers’ continued participation in the ACA exchanges.

Here, Beth Fritchen, FSA, MAAA, and Kurt Giesa, FSA, MAAA of Oliver Wyman Actuarial Consulting provide a summary of the survey findings.

Impact of possible CSR defunding

The nationwide survey of health insurers, conducted May 16 to May 24, found that 94 percent of respondents currently offering plans on the ACA exchanges intend to remain in that market; 6 percent intend to exit.

However, if CSR payments are halted, 42 percent of respondents said they would likely withdraw from the market. The other 58 percent indicated they would refile proposed rates, with the assumption being payers would adjust rates higher to cover the loss of the CSR payments. (Although filing deadlines typically don’t allow for such tweaking, some state insurance regulators have indicated they will offer payers additional flexibility with filing deadlines and/or filing two different sets of rates.)

CSR is available to ACA enrollees earning 250 percent or less of the federal poverty level. The program is designed to defray out-of-pocket costs for people with lower incomes. To help insurers offset the cost of CSR, the federal government provides insurers with CSR payments. For the 2016 federal fiscal year, the government provided $7 billion; for the 2017 federal fiscal year, the payments are expected to hit $10 billion, assuming funding continues through year-end. The Trump administration has indicated it may halt these payments

The degree to which plans would be impacted by CSR defunding will vary greatly by market. Plans that have attracted a higher percentage of CSR-eligible enrollees will likely have a difficult time competing – this because most are expected to hike rates to cover the loss of CSR payments and a substantial rate increase could price them out of competition.

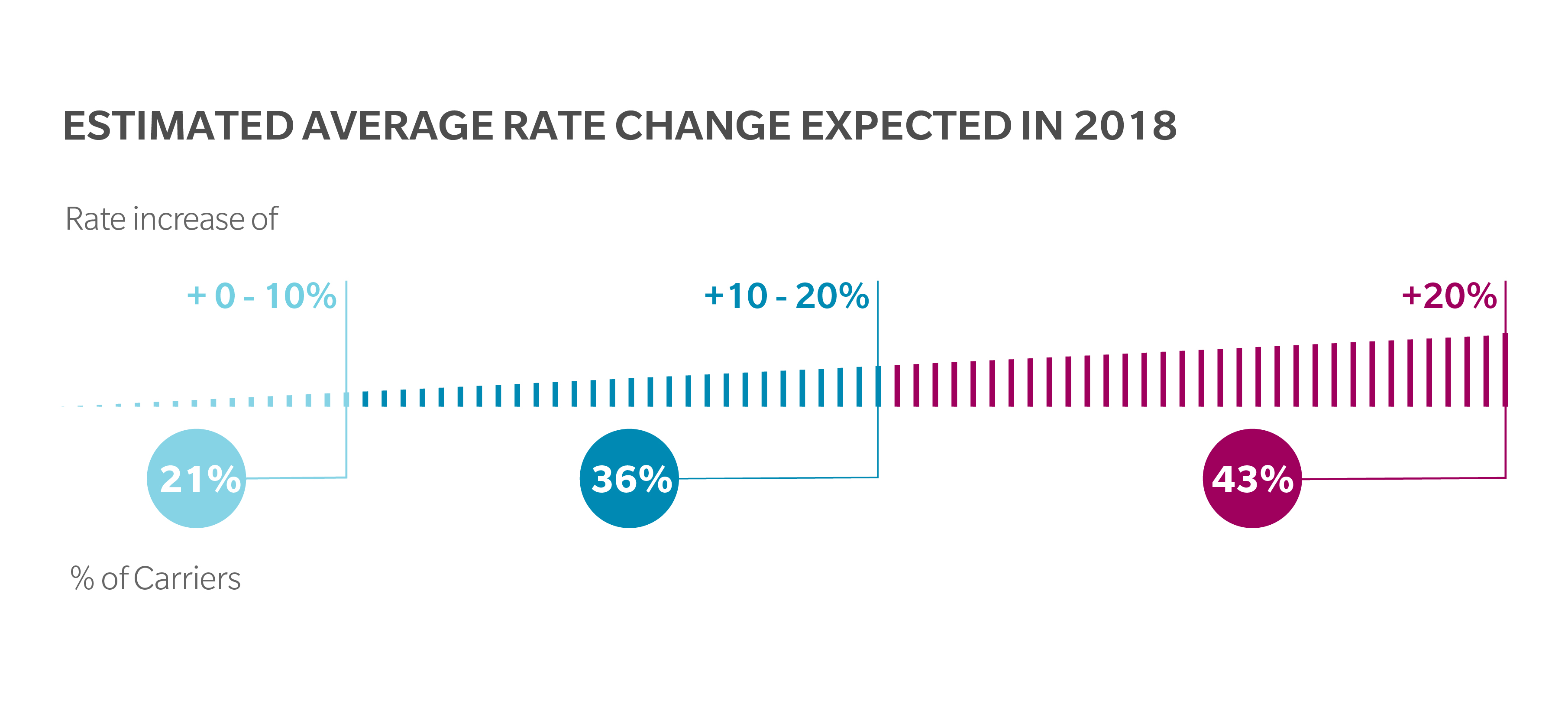

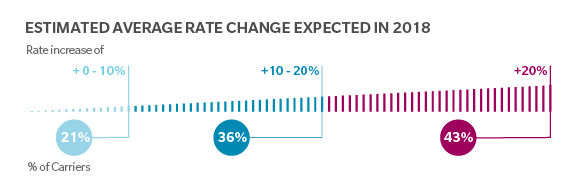

More rate increases

Our latest survey finds that the number of payers planning significant rate hikes is up. Of payers responding, 43 percent are planning on increases of 20 percent or more. When surveyed in April, just 25 percent said they were planning rate increases that high.

Fifty-seven percent of respondents are planning rate increases of 20 percent or lower. And taken as a whole, the straight average across all respondents was a 20 percent increase. In 2017, the weighted average rate increase was 22 percent, according to the Department of Health and Human Services.

Although our survey indicates that the average 2017 increase and 2018 proposed increase are comparable, this is not what the market had originally expected. Before the latest round of health reform, many had predicted that 2018 rate increases would be lower than in years past and that the market would begin to stabilize. Given the survey responses, it appears that the overall uncertainty of the market is impacting payers’ 2018 planning.

Regulatory changes not having significant impact

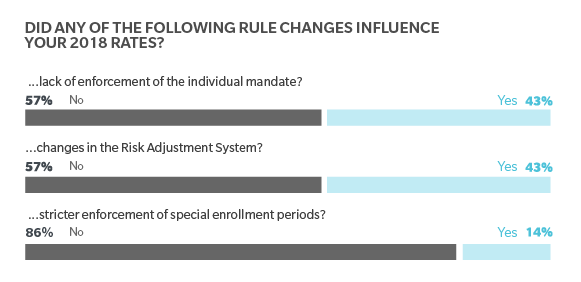

Survey respondents had a range of reactions to recent policy actions. In some cases, these policy and rule changes – some taken to help stabilize the individual insurance market – seem to have had little impact on payers’ pricing decisions. For example, 86 percent of respondents said the final market stabilization rule was not reflected in their pricing. The rule, which was released in April, shortens the open enrollment period and tightens special enrollment eligibility. Similarly, when it came to revision to the Risk Adjustment program, 57 percent of respondents did not take these revisions into account when setting rates.

Another significant change that could influence payers’ rate is the relaxation of the individual mandate. On January 20, President Trump signed an executive order instructing federal agencies to interpret the ACA’s regulations in a way that would “minimize the economic burdens” on individuals and businesses. In February, the IRS announced it would accept tax returns without proof of health coverage, meaning: people no longer have to prove they have health insurance and there is now no way to enforce the individual mandate.

When asked whether this relaxation of individual mandate influenced their 2018 rate setting, 57 percent of respondents said ‘no.’ Among the roughly 40 percent who said ‘yes,’ the impact ranged from rate increases of 3 percent to 20 percent. The wide range illustrates the difficulty payers are having anticipating the potential impact of market changes on the risk pool. For while the lack of individual mandate will likely lead to fewer young, healthy people enrolling, insurers can’t fully anticipate how it may impact other enrollees. And without a clear view of the risk pool, insurers are left having to make some assumptions about their 2018 risk pool.

Market seeks clarity

The wide range of requested rate increases considered alongside the range of assumptions included in the development of 2018 premium rates illustrate the uncertainty issuers are dealing with surrounding the individual market. The single largest concern for carriers right now is the potential defunding of the CSR payments. While a large portion of the insurers that responded to our survey stated they did not include the impact of the CSR defunding in their premium rates, the fact that 42 percent said they will likely withdraw from the market if CSRs are not funded shows the challenges issuers are facing in trying to serve this market.