The global aviation maintenance, repair, and overhaul (MRO) market exceeded $136 billion in 2025, up 8% over 2024. This increase reflects an extended MRO “super cycle” — a combination of an aging fleet requiring higher maintenance and ongoing durability/reliability challenges for newer aircraft. By the end of the decade, spending is expected to approach $193 billion, nearly double the 2019 level. Beneath this growth, however, there are concerns about a new supply chain paradigm — featuring more materials shortages, higher costs, and worse performance.

MRO industry's top disruptors for the next five years

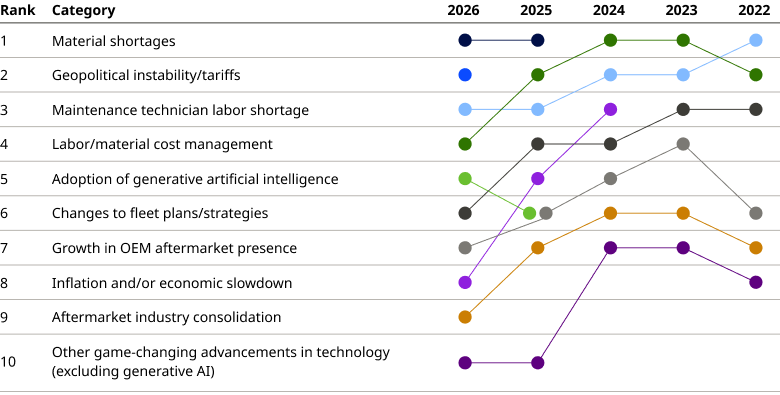

As always, we asked survey respondents to share their views on the top disruptors in the MRO industry over the next five years (Exhibit 1). Material and labor shortages and cost management continue to dominate, although a new category this year, geopolitical instability/tariffs, instantly rose to second place as a disruptor.

Tariffs have added to supply chain uncertainty, while geopolitical instability has put pressure on airline top and bottom lines. The adoption of generative artificial intelligence (AI) as a disruptor rounded out the top five.

Material costs exceed forecasts by up to 200 basis points in 2025

We have asked for several years in a row whether and when the industry expects post-COVID supply chain challenges to subside (Exhibit 2). It now appears that the answer is increasingly much further in the future or “never.” This suggests that the supply chain has structurally shifted to a new baseline — one in which higher costs and scarcity must always be factored into MRO regimes.

Material cost inflation remains challenging, outpacing expectations by 100 to 200 basis points per segment in 2025 (Exhibit 3). Survey respondents expect higher material cost inflation this year as well. Several factors are driving this outlook, including materials shortages, geopolitical instability, increased spare parts inventory, and the servicing needs of a large fleet of older aircraft. The need to recoup the high cost of new aircraft technology development is also putting pressure on the aftermarket. And some 90% of respondents said they are experiencing tariff impacts — particularly for component purchases, repairs, and engine overhauls.

Engine shop visits are taking longer and costing far more than expected

The growing idea that the supply chain has entered a new era is further supported by the ongoing difficulties in engine MRO, which accounts for more than half of MRO spend.

Engine turnaround times (TATs) on narrowbody engines are now regularly 180-200 days or more for many operators, well above pre-pandemic levels.

More than half of the respondents do not expect improvement in TATs within the next three years (if ever). Further, two-thirds of respondents report that shop costs for the newest, next-gen narrowbody engines are exceeding expectations by 21% or more (and a quarter by 50% or more).

Stabilizing labor rates but two-thirds of MRO operators struggle to find qualified technicians

Labor rate inflation in 2025 came in slightly below expectations across line and airframe, but remained stubbornly high for engines and components. In the case of labor, expectations appear to be converging with reality, as labor rate inflation has settled in at 5.5-6.0% across most categories. This is compared to about 3.0% on average pre-pandemic.

Labor attrition trends for 2025 were generally the same or slightly worse than a year ago, but more than half of survey respondents expect attrition to be even worse next year. The number of certified mechanics in the US, for example, is not keeping pace with demand. In line with this, two-thirds of respondents said that finding aircraft technicians and mechanics has become moderately to very challenging.

MRO is warming to AI, but data readiness is holding the industry back

Both this year and last, 58% of respondents reported their companies were stuck at the “experimental” stage of AI development. However, two-thirds said they are seeing value from AI that is as expected or more than expected – a strong uptick over prior years (Exhibit 4). This is likely due to a better understanding of AI's strengths and weaknesses, enabling more suitable and successful use cases to be built.

The challenges companies are facing in scaling AI — particularly a lack of data quality and availability — may be a key reason for the stallout at proof-of-concept. Organizations may need additional investment in data infrastructure and governance to support the data needs of more advanced AI applications. (According to our survey, half plan to invest in AI in the next five years, but only a third in IT infrastructure.)

About the 2026 MRO survey

Now in its second decade, the annual Oliver Wyman MRO survey is an industry standard that samples the attitudes and strategies of executives from across the aviation industry as they address key trends and emerging issues in the MRO sector.

This year, more than 150 aviation professionals from around the world took part in the survey. Respondents were drawn from a cross-section of airline operators, airline and independent MROs, OEMs, and others. About 60% are senior executives (C-suite or vice presidents) and 80% are director-level or above. And 70% of respondents’ companies have a primary base of operations outside of North America.