While progress in developing climate transition plans has been impressive, the depth and detail are often less reassuring.

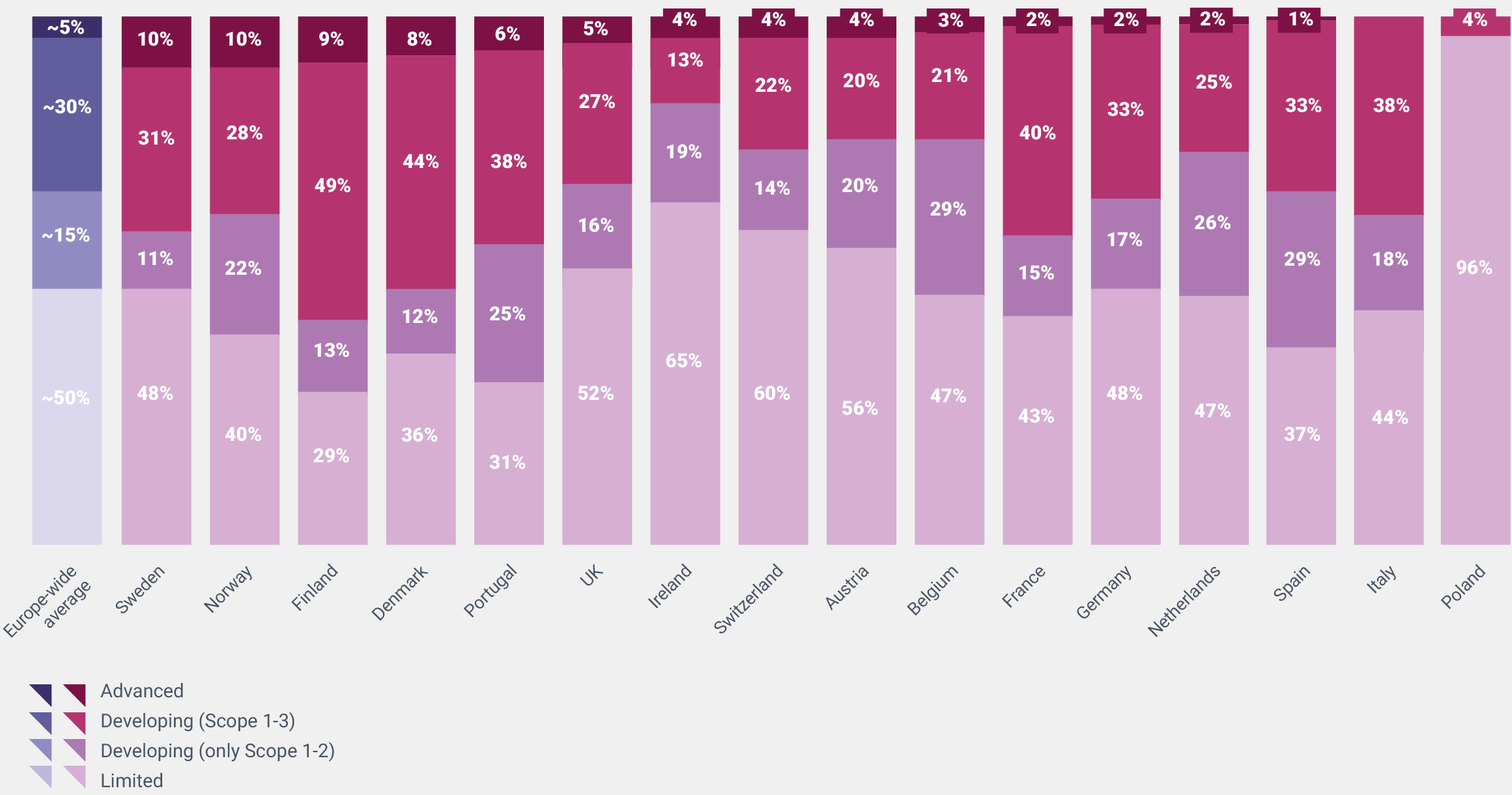

Around half of the European companies responding to CDP’s questionnaire this year claim to have transition plans aligned with the Paris Agreement’s 1.5 degrees Celsius limit. However, when we analyze the ambition and transparency of those plans based on their disclosures to CDP, less than 5% of companies show the advanced transition readiness required to achieve the Paris goal. Most companies also fail to address the economy’s impact on nature and its inherent connection with rising temperatures.

Climate transition plans are critical tools for leadership and Boards directing the initiatives needed to deliver on pledges made. External stakeholders are also demanding to see clear plans that set out concrete steps to drive change over time, and to understand how plans will adapt to shifting dynamics as technology, policy and commercial trade-offs evolve. That’s why both the substance and disclosure of transition plans matter.

Regulators in both the United Kingdom and European Union will be requiring companies to produce public transition plans as soon as next year. Both sets of regulators will also mandate regular disclosures of plans as well as on progress being made toward their objectives.

Many aspects of companies’ transition plans today are promising works-in-progress: adoption is still partial but heading in the right direction. Even in the areas where the most progress has been made, there are important discrepancies between leaders and laggards.

Governance being a good example. To illustrate, while almost all companies (99%) have adopted Board-level climate oversight, only half (54%) have integrated climate KPIs into executive compensation.

Among these stories of partial adoption, three more structural gaps emerge in corporate transition strategies today:

We assessed key actions across five core areas, based on industry standards and guidance on climate transition plans. While progress is strongest in putting in place governance structures and setting targets, it is weakest in setting out the internal and external implementation strategy, on elements such as financial planning and value chain engagement.

Internally, though 9 in 10 firms have initiatives in place to cut emissions, only 26% are able to assess the alignment of their spending and their revenue with their low-carbon transition. Externally, fewer than 40% are building climate concerns into supplier contacts. It is hard to execute a plan that is not connected to these critical business levers.

There is increasing realization that the global effort to combat climate change cannot be effective without addressing the nature crisis simultaneously. To reflect this, going forward transition plans will need to be enhanced to reflect firms’ dependencies and impacts on nature and biodiversity. Companies are starting to realize this: in the first year of disclosure, 39% of companies in the CDP questionnaire reported having made any public commitments on protecting biodiversity, though the scope and ambition of the commitments varies significantly. Some companies are limiting their efforts to respecting already legally protected habitats and locales.

Among companies operating in areas that materially impact water and forests, only small percentages had defined objectives and metrics for protecting nature. For instance, only 7% of responding companies had robust targets across water, climate, and forests, and only 5% of companies source at least 90% of their commodities in a certified no-deforestation compliant manner.

As financial institutions seek to make good on their commitments to net-zero, they will be increasingly scrutinizing corporate’s transition plans. Indeed, 80% of financial institutions responding to CDP have begun to assess the transition plans of their clients in at least some sectors. Looking at the banking system, a mismatch is emerging. 36 of the top 50 banks in Europe have committed through the Net-Zero Banking Alliance to steeply cut their financed emissions. To hit their targets, they need their corporate clients to cut their emissions steeply – or to find new clients. Today, however, up to 20-40% of corporate debt relates to companies with only limited transition planning in place, meaning they either lack decarbonization targets aligned with a 2°C limit, or have failed to disclose at least half of the transition plan-related indicators included in the CDP questionnaire.

While many financial institutions are keen to engage with corporates in high-emitting sectors to help them transition, it is hard for them to do so with confidence without these core elements of a plan in place. Companies that do not make progress to address these gaps are likely to find financing harder to access over time.

Although all companies should be disclosing on all elements of a credible climate transition plan, they are not a one-size-fits-all exercise. Each company will face different commercial trade-offs and decarbonization levers that need to be evaluated as part of its business strategy, and so each will be unique. For instance, a key element of an automobile manufacturer’s transition is its adoption of zero emissions vehicles which should be detailed in its transition plan with clear forward-looking sales targets and associated R&D-spend. Meanwhile, a financial institution should detail how it is adapting policies and decision-making to align its portfolio to environmental objectives.

Transition plans must also reflect the dynamic and uncertain economic environment companies operate in. While plans inevitably need to be revisited as technologies, regulation, and economics shift, investors and financial institutions — as well as the public and employees — are going to be increasingly less patient with backsliding. Like regulators, these stakeholders are not only going to demand plans that set out a vision of how the company can thrive while generating lower emissions. They are going to want to see clear strategies to deliver that vision.

A special thanks to Julien Hereng, Suzanne van der Meijden, Jennifer Tsim, Bruno Despujol, Simon Glynn, Simon Cooper, and Barrie Wilkinson for their contributions to the report.