Despite the pandemic, the global luxury market has outperformed the rest of the retail and consumer goods market with robust growth due to the increasing number of high-net-worth individuals (HNWIs) worldwide.

Considered to be among the class of most valuable and durable luxury goods is the luxury vehicle market, which is expected to grab market share from the non-luxury vehicle market in the coming decade.

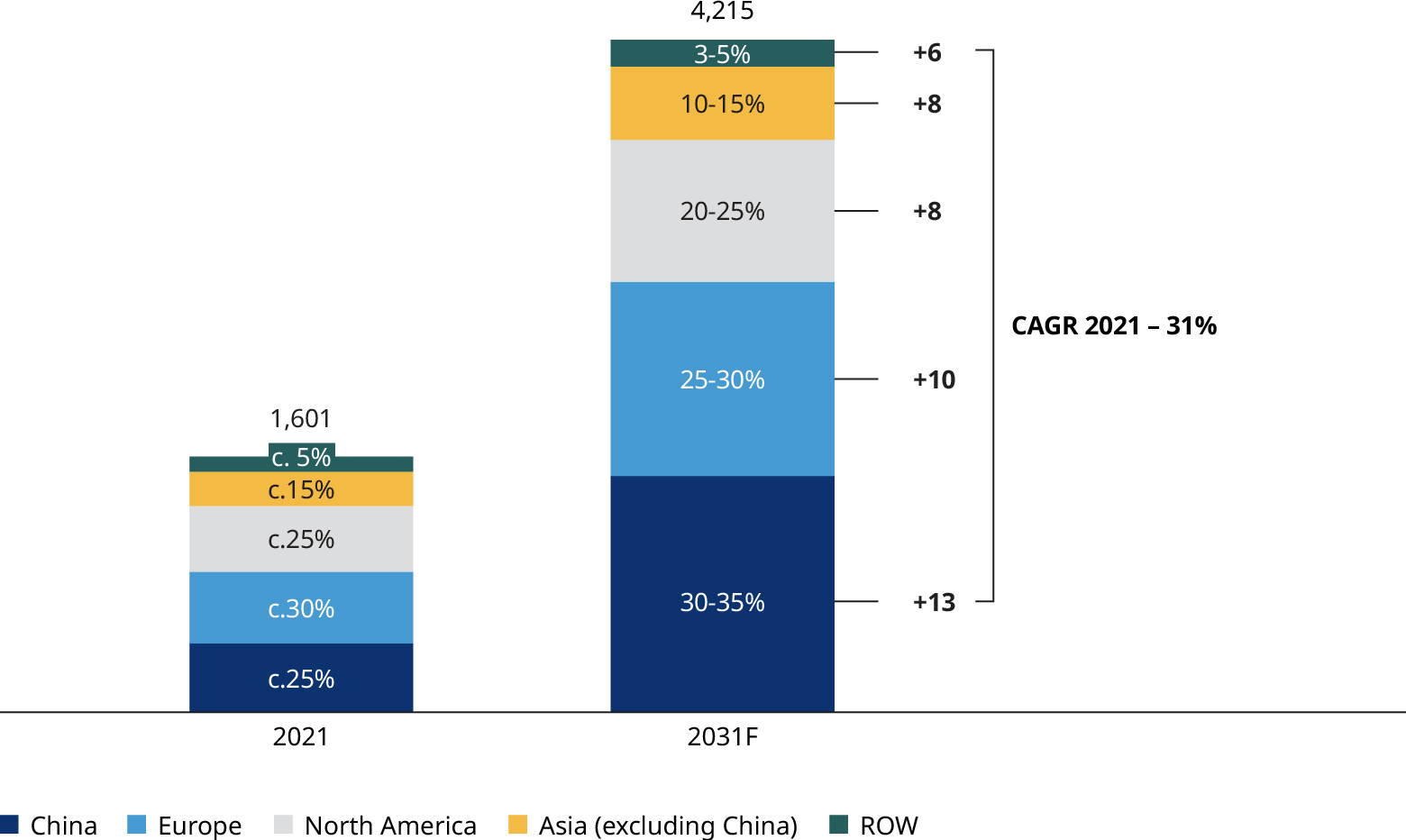

In fact, with the progress of connected car, autonomous vehicle, shared mobility, and electrification (CASE) technologies, the luxury (suggested retail price at $80,000-$299,000) and ultra-luxury (suggested retail price of more than $300,000) vehicles market is expected to grow at a much faster CAGR of 10% from 2021 to 2031.

Among all the major economies in the world, China is expected to be the fastest-growing market for luxury and ultra-luxury vehicles by 2031, with an anticipated CAGR of about 13%. By then, China’s share of this market’s global volume is expected to reach 30-35%.

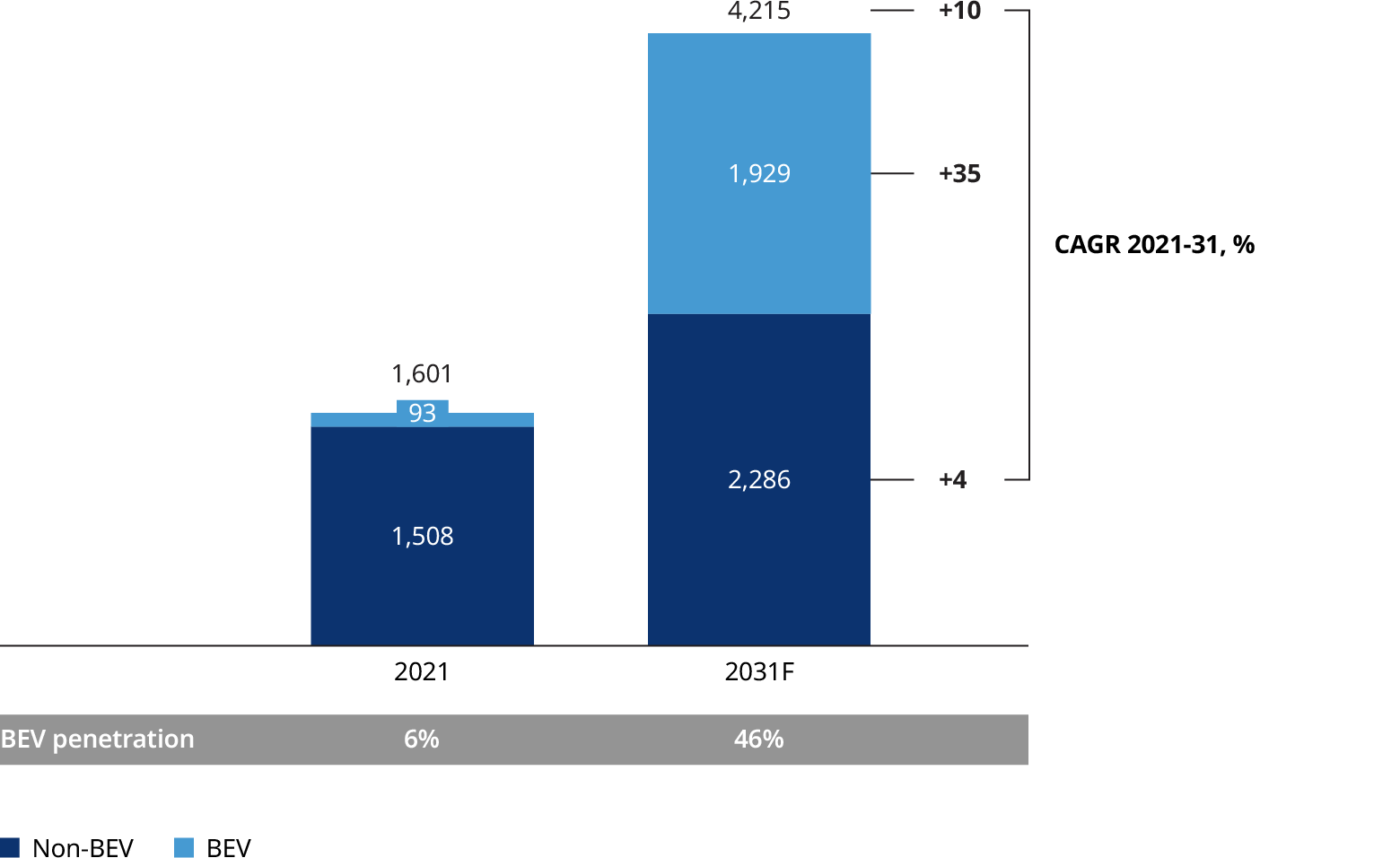

The overall battery electric vehicle (BEV) penetration rate of all luxury and ultra-luxury vehicles was around 6% in 2021. It is expected to grow to 46% in the next decade. The luxury and ultra-luxury BEV market will likely increase over the next 10 years, with a CAGR of about 35%, almost 10 times the CAGR expected for non-BEV. Driving future growth is the rising preferences of customers, electrification technology advancements, and favorable policies.

Evolving luxury vehicle technologies and business models

In addition to the traditional comfort, convenience, entertainment, and safety features, luxury electric vehicles bristle with advanced autonomous driving, connectivity, intelligent interactions with smart cockpits, and enhanced vehicle usage experiences. Major players have begun introducing these cutting-edge technologies to their new models.

Advanced and intelligent software systems also enable luxury and ultra-luxury automakers to unlock new monetization models, such as over-the-air upgrades for value-added services. In addition, new mobility services, such as battery-swapping, battery-as-a-service, car subscription, and car leasing, have also gained traction. Leading players have launched these emerging services, which can help expand their profit pools while providing a more flexible, convenient mobility solution for customers.

Intensified competition in the luxury car market

The luxury and ultra-luxury electric vehicle (EV) segment is still in its nascent stage. In 2021, the luxury and ultra-luxury vehicle market accounted for about 2% of all passenger car sales volume, with about 150 models launched. However, among these models, only less than 20 models are battery-electric. Considering the vast growth potential, the internal combustion engine (ICE) incumbents and emerging EV challengers are both targeting to enter this segment. Yet, both of them will encounter significant barriers. There would be a need for more relevant technologies, the flexibility of transitional challenges for the former, and a lack of brand awareness and marketing and distribution capabilities for the latter.

Almost all mainstream luxury automakers have made public announcements regarding their electrification timeline and product pipeline, each with usually two to five BEV models in the works. In the next five years, we expect an influx of luxury and ultra-luxury BEVs to monetize opportunities in the market. The well-prepared players that are determined about electrification will likely be the winners.

Five strategies to get ahead in the luxury vehicle market

Accelerate portfolio upgrade. The phasing out of ICE vehicles in favor of EVs is irreversible. Players should think beyond “product” and consider the potential offerings they can create. This is a whole new realm that awaits exploration. To position automakers toward being “service providers” rather than just “vehicle manufacturers” would be a good start.

Play as technology pioneers. Luxury and ultra-luxury automakers embrace new technology opportunities through in-house research and development or external collaborations based on their strategic considerations and technological capabilities. However, they should strike a delicate and strategic balance between adopting new technologies and the total production cost.

Build-up of organizational competencies. Incumbents are expected to be more innovative and open-minded, actively accelerating their organizational transformation by integrating revolutionary approaches, such as user experience and digitalization of customer interactions. New challengers can learn the best practices from incumbents to reinforce their global governance and cross-border business collaborations.

Go to market with DTC. Personalized and individual experiences play a more pivotal role in affluent customers shopping for luxury cars, making the direct-to-consumer (DTC) model crucial for sales and marketing. However, the DTC model can threaten the long-established relationships between the ICE incumbents and their dealers. Combining the dealer’s 4S stores with direct retail stores or transforming the dealership model into an agency model might be viable solutions.

Reposition the “luxury” brand. The old-fashioned brand images of driving experience, engine performance, passion, or being part of the business elite have become obsolete. As a result, luxury automakers need to rethink their brand positioning by maintaining their original DNA and upgrading the brand to take advantage of new perspectives, such as the younger generation, digitalization, and sustainability.

Download our report for full access to the luxury vehicle market trends.