Managing loyalty rewards programs through the pandemic has brought on a wide range of challenges to accurate forecasting, from changes in consumer behavior to changes in program rules to account for the pandemic. Here, we are highlighting two particular aspects that have had a surprisingly large impact on “breakage” (or the percentage of points that will not be redeemed).

Pandemic Impact #1: Points are being accrued differently than before leading to decreases in breakage

Over the course of the pandemic, members who typically accrued via credit cards (or other financial sources) remained highly engaged. Conversely, members who accrued via travel or entertainment sources became much more disengaged. How does this change in point accrual sources impact breakage estimates?

Consider the following illustrative graph:

* Illustrative graph based on experience of a number of loyalty programs pre- and post-pandemic

As shown, the number of points accrued via Flight, Entertainment and Retail sources plummeted during the pandemic whereas the number of points accrued via credit cards remained largely unchanged. As a percentage of all points accrued in a period, Credit Card Accruals jumped up from 40% before the pandemic to 80% during the pandemic, as shown in the following pie charts.

All other things equal, members accruing via a credit card are generally more engaged than members accruing via Flight, Entertainment or Retail sources. Thus, as a percentage of points accrued, breakage should decrease for points accrued during the pandemic because, simply, point activity is more weighted towards types of members that redeem a high proportion of their points.

However, while the overall breakage rate may decrease, this is unlikely to translate to a higher liability estimate, since the breakage rate will be applied to a smaller number of points accrued in each period.

Impact #2: An "expiry freeze” during the pandemic can lead to sharp changes in breakage

As discussed above, a group of members in your program may have fallen into dormancy during the pandemic – for example, travel and entertainment members who could no longer continue to accrue during the pandemic.

You may have implemented a freeze on point expiry for the majority of the pandemic so as to prevent newly disengaged members from expiring, and thus to keep them engaged with the program over the long term. Engaged members (e.g. credit card accruers) continue to accrue while disengaged members hold on to dormant points. This is illustrated in the example below.

After March 2022, you may be considering removing the expiry freeze. A large number of dormant members will then face point expiry in an event we call an “expiry wave”. Will you need to increase or decrease your loyalty liability estimate following the expiry wave?

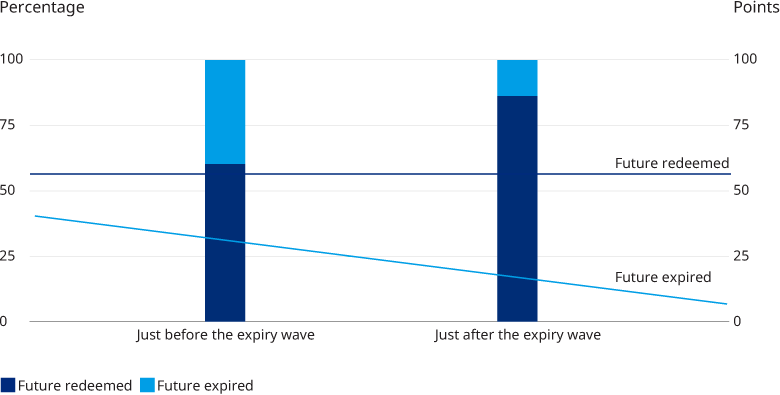

Consider the following graph:

On the left, we show your financial position just before the expiry wave – you are reserving for 60% of points in force, assuming that this proportion of points will go on to be redeemed in the long term. When point expiry recommences, the expiry wave hits – a large number of points in force is removed from your program as expired points. This leaves a greater proportion of points in force that can be expected to be redeemed in the long term. In the right column, around 85% of points are ultimately expected to be redeemed.

The jump in the redemption expectation (from 60% to 85%) is a significant increase of 25 percentage points. But do not be alarmed, for your financial liability should not change due to this event alone, all other things equal. As shown in the example, the same number of points are expected to be redeemed in the long run (55 billion points in the graph) before and after the expiry wave. It is only the number of points expected to be expired in the long run that will change (37 billion points before the wave reducing to 9.2 billion after the wave). This explains the abrupt increase in the redemption expectation to 85%.

When forecasting your loyalty liabilities, be sure to adjust your redemption expectations assumptions if a percentage is applied when preparing your financial statements.

Conclusion

The examples provided here demonstrate that care is needed when applying breakage rates in practice. To ensure that the breakage rate being applied at any moment is consistent with the most-up-to-date information available, it is important to frequently review accrual, redemption and expiry assumptions as loyalty programs move into different phases of the pandemic.