In the past decade, several education-focused unicorns raised hundreds of millions of dollars worldwide each year. In most cases, the companies had healthy, profitable business models. However, these deals were dwarfed by those of Chinese online after-school tutoring giants in 2020. They averaged three to five billion dollars each quarter, despite many of the institutions not exhibiting sustainable growth models at the time.

Investors were previously upbeat that Chinese middle-class parents tend to invest heavily in their children’s education, and that technological disruption could further spur this frenzy. Nevertheless, they ignored the fact that the government wished for good children’s education to be equally accessible without being financially burdensome for households in an already exceptionally competitive environment.

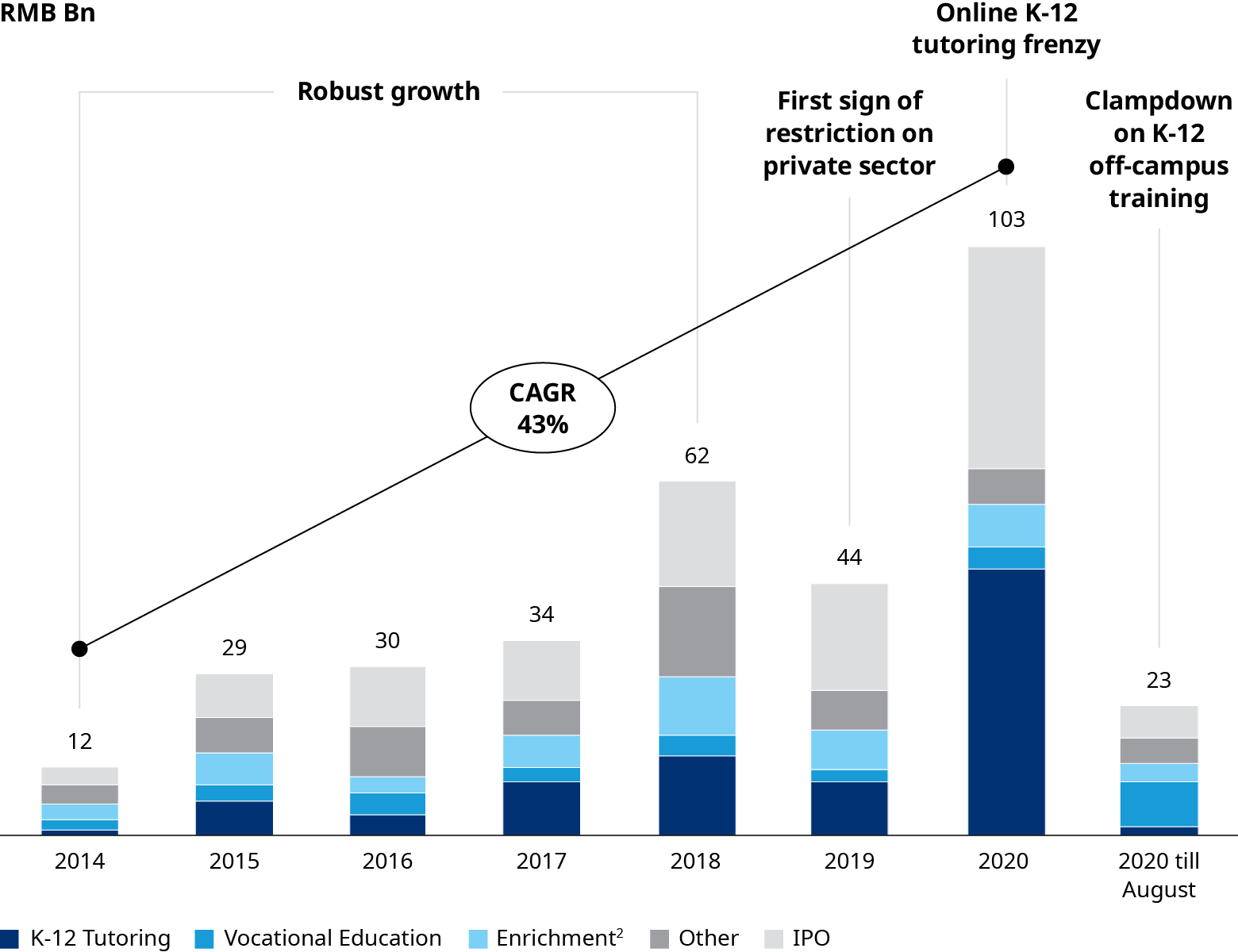

1. Excludes undisclosed investment and deals that haven't disclosed investment amount. 2. Includes language training.

The Chinese government has finally unveiled stringent polices to potentially end the barbaric growth of private education over the past decade. It also marks the beginning of a new era where off-campus institutions transform from shadow schools to effective supplement of on-campus education in China.

Many education operators and investors in developed and developing countries were shocked by China’s new policies, wondering whether similar policies would be implemented in their own countries or affect investor confidence. In our view, any potential policy changes in other countries would only be based on their own national conditions, so there is no need to panic.

What’s next for the off-campus education industry?

We believe that for the existing after-school tutoring products, companies need to shift from the extensive growth mindset to a refined management model, focusing on the profitability at the product level. Institutions must shift the focus to a lean operation perspective, which is centred on product design and internal management, from the previous traffic-driven perspective focusing on advertising and customer acquisitions. They must try to achieve a breakeven for each transaction and carefully manage various costs, such as those for customer acquisition and the R&D for courses. And operators need to adapt to the policy reform, continue self-inspection and navigation to find the right course (where their offerings align with the next generations’ education needs), and upgrade their operations.

Specifically, they can focus on the following aspects:

They can explore opportunities in, for example, the family education, enrichment course, study tour, and educational hardware segments. Example products may include aerospace-themed science literacy courses, STEAM-themed camps, and family education scenes powered by intelligent education software and hardware. When designing new products, companies should return to the core elements of education and refrain from the mindset of customer acquisition through burning cash. The new regulatory landscape indicates that companies may only achieve sustainable growth by designing quality products that address the pain-points of users.

Education and training institutions can also tap into the adult training space, including conventional vocational training, new occupational training, degree education, and elderly education. There are already cases of K-12 tutoring providers attacking the vocational training market, and vocational training players entering the field of higher education through industry-university joint colleges.

The business-to-business (B2B) market, which serves schools and education authorities, is also worthy of attention. Under the new policies, education authorities and schools need to improve educational quality and efficiency, a formidable task for schools with less competent teachers and dated IT capabilities. Their needs for empowering technologies, and better content and training will drive an increase in procurement and provide new opportunities for B2B suppliers.

Exploring education markets overseas is also expected to become a new option. However, players should not simply duplicate the current offerings tailored to the China market and launch them in other countries. Instead, they need to carefully design new products customized to the local markets’ target customers. Some players have already successfully launched Chinese-learning courses and 2C enrichment education in foreign markets. Compared to content-oriented products that require much more local-market knowledge, technology-driven tools such as online delivery platform and photo-searching homework helpers are easier to get off the ground in these overseas markets.

Overall, enrichment education, vocational training, and overseas business expansion are expected to see accelerated growth. The previously less popular online B2B market will also be reignited and usher in a fast-growing pattern (similar to that seen in developed markets) in the next five to ten years. In fact, it is the best window for overseas players to explore the above sectors in China, but they need to work harder on content compliance. All their previous concerns, such as the less rigid demand and the lack of share of wallet, have now been swept away by the new policy.

We have no doubt that China’s education reform will continue to deepen, and more policies and detailed implementation guidelines will be unveiled in the rest of the year. We are convinced that as the education industry kicks off a new chapter, high-quality products are still prized commodities in China. Education and training institutions and investors need to urgently embrace and adapt to these changes, leveraging their wisdom and innovation capabilities to wisely navigate this new landscape.