While many large industries see adaption to climate transformation as a burden, for the telecom operators industry, the opportunities outweigh the costs. A survey of 19 representative telecom operators, based on their CDP submissions, highlights the importance of three factors that have an impact on telecom operators’ carbon emissions: their upstream supply chain of goods and services, their use of energy to run networks and IT, and the downstream use of electricity as customers use their services (see Deep Dive 1).

The telecom operators’ own risk and opportunity assessment shows they expect climate change to increase usage of telecom services by two to three percent and boost revenues by one to two percent. Operational costs, meanwhile, will be balanced out by operational improvements. In other words, according to their own analysis, climate change is an opportunity (see Deep Dive 2).

These benefits depend, of course, on telecom operators taking the right steps to transform their businesses and reduce emissions. We think the most valuable progress can come from working with others — suppliers of capital goods, energy companies, and customers.

Telecom operators already source more energy from renewable sources than other industries on average, and they can do more by forming agreements with developers of renewable energy. Consumers can be further persuaded to use renewables through marketing appeals and special offers. To reduce emissions in their supply chains, telecom operators can work with their suppliers, using transparency measures and communicating their priorities.

These moves imply new ways of working — and thinking — at telecom companies, so they require an internal transformation. Positive effects could include a boost to employee morale, a clear message to investors on environmental commitments, and greater attractivity in the eyes of increasingly climate-aware customers. The response to climate change therefore represents an opportunity for telecom operators, which have already built momentum through their contribution to new working practices during the COVID-19 pandemic. We believe telecom operators can do more to realize the opportunities available in ways that will benefit customers, employees, and shareholders. For our benchmark group of 19 companies together, the upside is estimated to be between €7 billion and €14 billion in annual revenues.

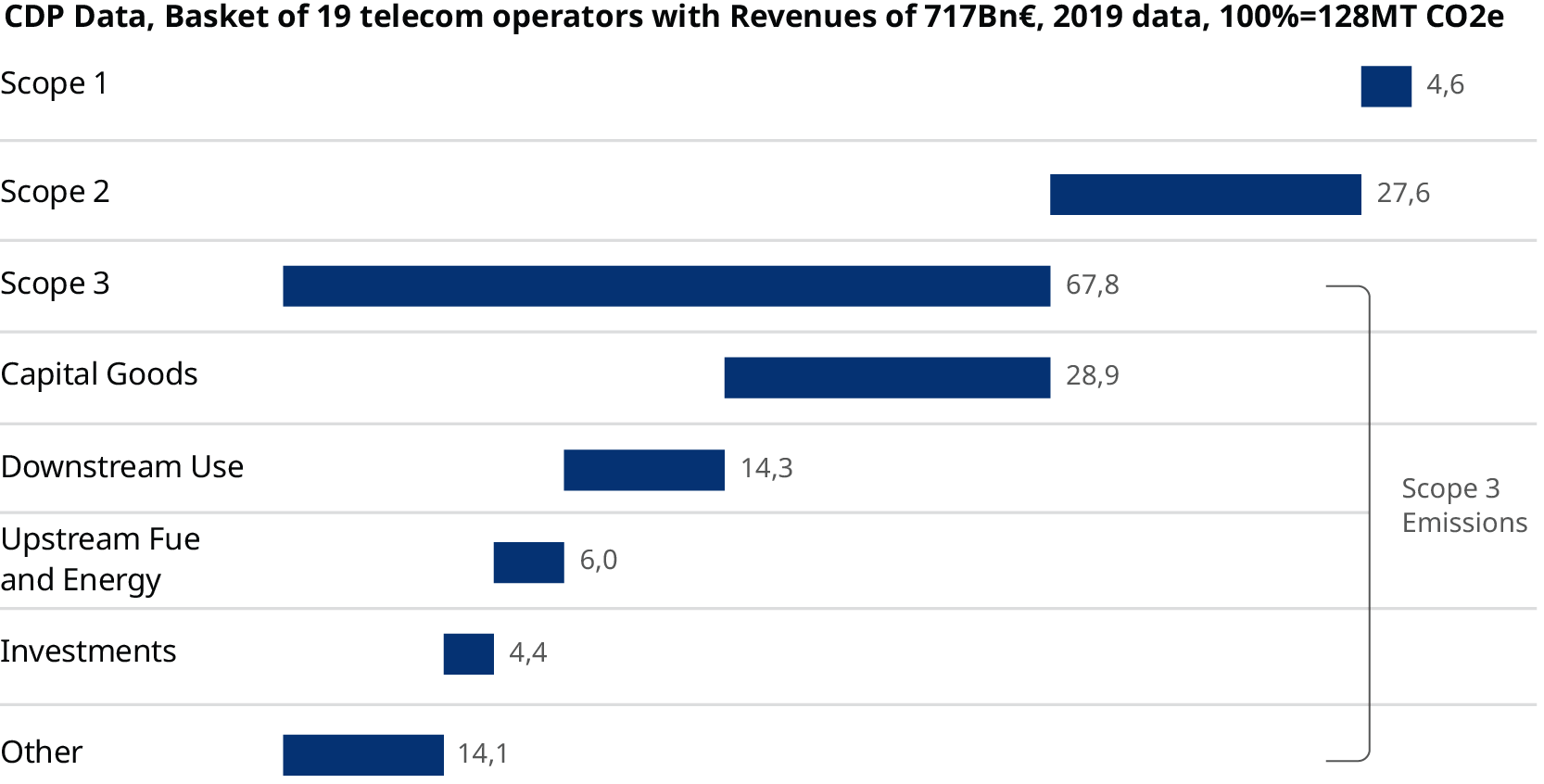

The results show that, if telecom operators want to reduce their emissions by more than 50 percent, as many have stated, they must address scope 3 the upstream supply chain, which accounts for nearly half their overall emissions. The biggest contributor is capital goods, followed by “other” (consisting mainly of goods and services), and upstream fuel emissions.

Scope 1 and 2 emissions arise primarily from the purchase or generation of electricity to run networks and IT, with a small quantity of fossil fuels needed to run offices, vehicle fleets, and various employee activities. Together scope 1 and 2 make up nearly a third of the total carbon footprint.

Our analysis is based on the recent reporting of 19 representative telecom operators to CDP, a partner of Oliver Wyman that gathers a comprehensive set of data on carbon emissions, including a breakdown as well as risk and opportunity assessments. The data is for 2019 — and, therefore, before the COVID pandemic and its impact on industry — and the companies are mainly European, though some come from Asia or the United States. There is significant variation in how data is reported — for example, which data are allocated to which categories — and we have tried to normalize the picture as far as possible.

Together, the telecom operators had total annual revenues of €717 billion, and they reported emissions of 128 million metric tons of carbon dioxide equivalent (CO2e). That represents roughly 180 tons of CO2e per million euros of revenues. This places telecom operators in line with the carbon intensity of the MSCI Europe Index and slightly below the MSCI World Index.

Clearly, any individual telecom operator may observe diverging metrics. Greenhouse gas emissions are usually divided into three scopes. Scope 1 are direct emissions by a company, including fuel combustion and company vehicles. Scope 2 emissions are indirect emissions that come from the consumption of purchased electricity or other forms of energy. Scope 3 emissions are other indirect GHG emissions, for example those that come from a company’s value chain or from use of products that a company manufactures. Grouping emissions in line with these scopes yields the picture in Exhibit 1.

Overall, roughly one-seventh of the emissions result from downstream use of telecom services — mainly electricity to operate telecom equipment, so there is a ratio of roughly 2:1 between emissions from power the telecom operators buy for their operations and emissions to downstream use of their products. Investments (minority shares in other companies) are mostly a small category, yet one global operator reports significant emissions of its minority investments. The main emissions driver overall are scope 3 emissions, specifically the upstream delivery of capital good and services.

Form alliances to migrate to renewable energy faster

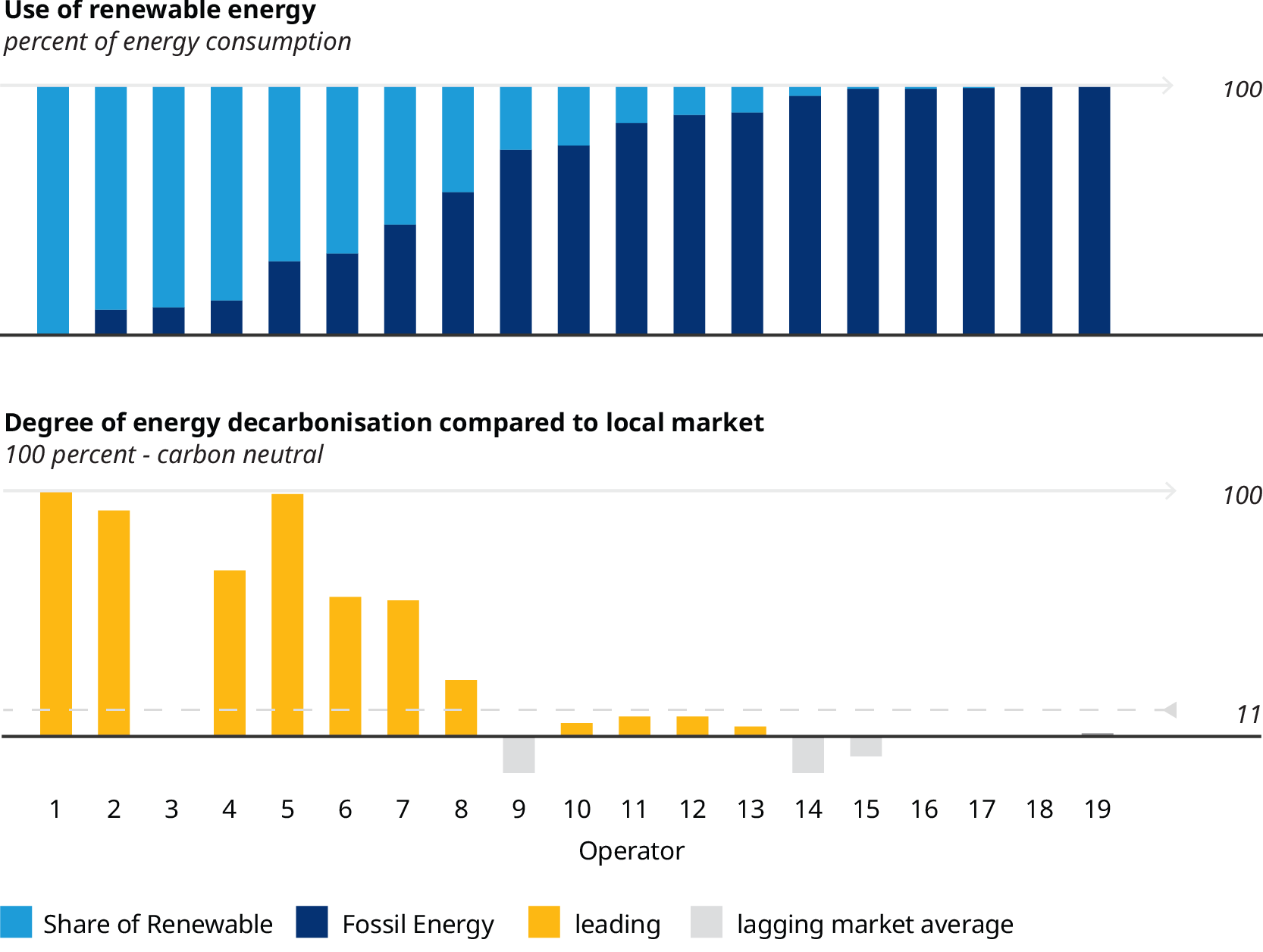

The greatest part of telecom operators’ Scope 1 and 2 emissions come from their use of electricity. This energy bill represents an average of around five percent of telecom operators’ overall operating expenditures, though the figure can be as high as 15 percent for telecom operators focused on mobile services, which are more energy-intensive.

Many telecom operators have already adopted this lever, and some of those have a zero or miniscule Scope 2 carbon footprint. On average, telecom operators already source 11 percentage points more renewable energy than their average local markets. This leadership results from a close focus by roughly one-third of the benchmark basket on renewable energy; the other two-thirds source renewable energy in line with other industries in their local markets.

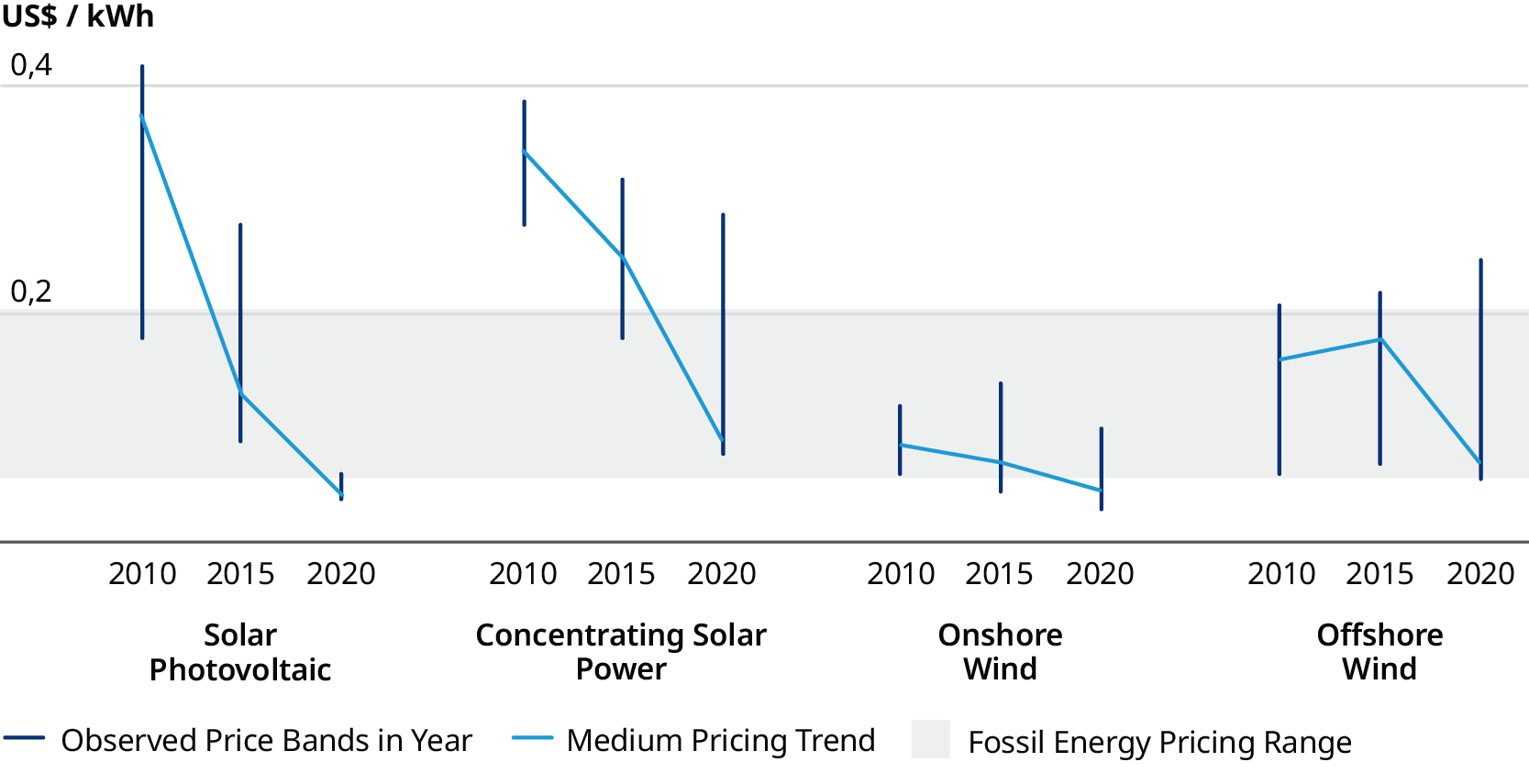

We think the shift to renewable energy could be accelerated, especially through power purchase agreements (PPAs). These are long-term arrangements that assure the developer of a renewables project that it will be able to sell the power it generates in future and provide the buyer with a stable, fixed price, as well as renewable energy credits. PPAs have significantly declined in price in recent years and now provide electricity at prices broadly in line with that generated using fossil fuels, despite undersupply of renewable energy in some locations.

Utility Teaming Opportunity: Given current market price levels and the longevity of telecom operators’ energy needs, they could team up with energy suppliers to support a long-term migration to energy from renewable sources. Potentially, the telecom operator could become a passive co-investor in a renewable power generation scheme.

Telco climate risk and opportunity assessment

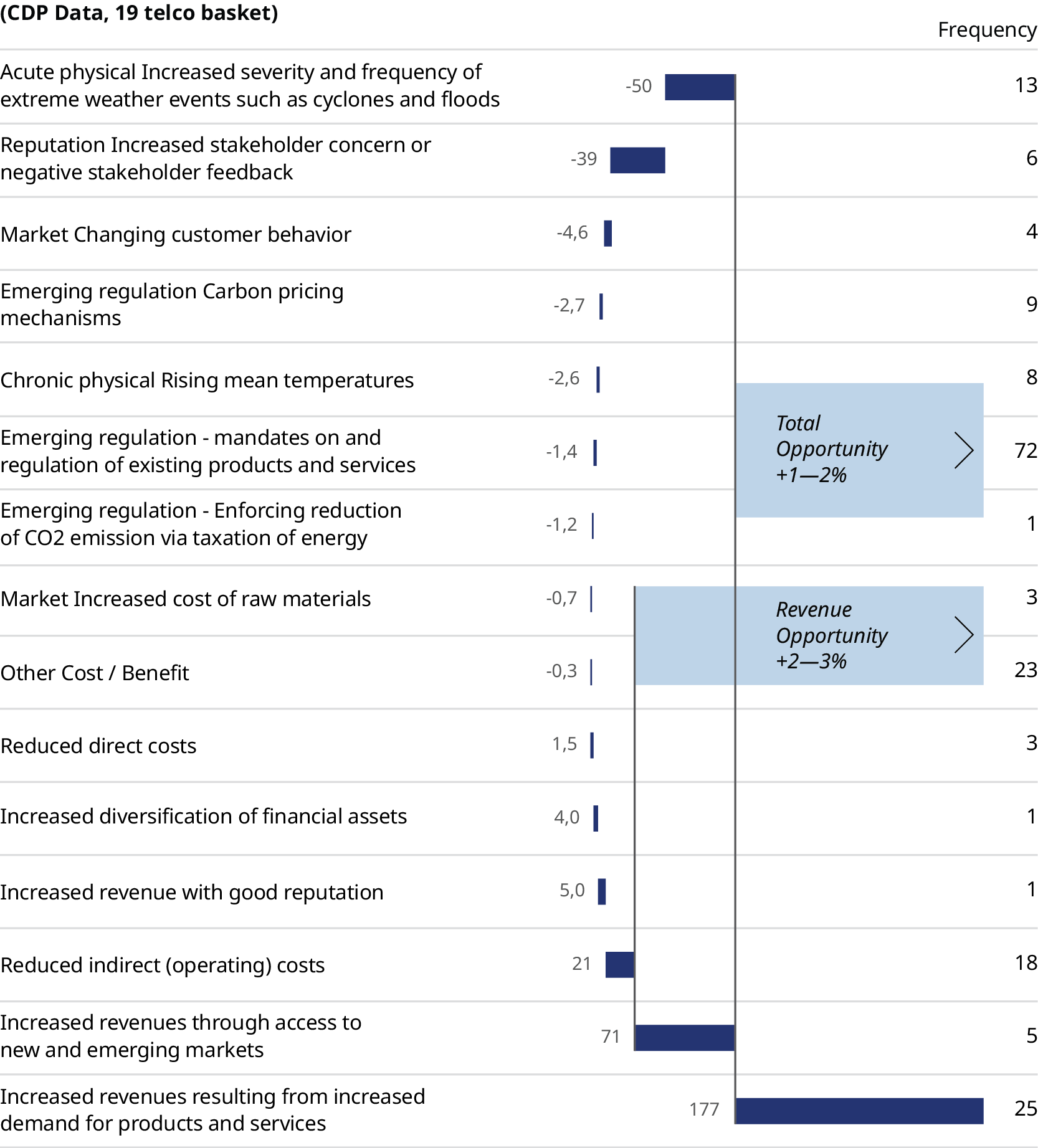

As part of the CDP reporting, each participant carries out a risk and opportunity assessment, including a ranged impact assessment. Exhibit 4 shows the aggregated and normalized impacts that telecom operators reported to CDP in basis points of revenue (100 basis points = one percentage point).

The impact of extreme weather events is estimated to equate to revenue reductions of 50 basis points, while the stakeholder concerns over environmental reputation will take off another 39 basis points. One of the telecom operators reported a much greater reputational revenue risk — around four percent of revenue (400 basis points).

Regulations, however, which are often cited as a source of extra cost, were seen as having relatively little financial impact — only five or six basis points of extra cost. (A larger bucket of drivers with a collective impact of less than one basis point have been aggregated in the “other” category.) Overall, operational costs and improvements nearly balance each other out, and the positive balance results from an increased take-up of telecom operators’ products and services.

Telecom operators see greater upside than downside in the impacts of and reactions to climate change, with total opportunities outweighing the costs by 1.8 percent (177 basis points) of revenue.

Incentivize consumers and B2B customers to reduce emissions

Downstream use of electricity — that consumed by the operation of B2B and B2C customers — accounts for 15 percent of telecom operators’ carbon footprint. Customers can rarely switch their power source for specific purposes or devices, but telecom operators can use incentives to encourage the adoption of renewables-based electricity. For consumers, these can take the form of brand-enhancing marketing appeals to a mobile operator’s green credentials; bundles that combine telecom services with power generated from renewables; perks — such as offering renewable energy users free weekend data or free sports on Friday; and financial incentives. Verifications that customers have indeed switched to renewables-based power could also lead to useful insights into their behavior and into the market in general.

In Spain, some telecom operators sell solar energy packages for businesses to self-install on warehouse roofs. Others have teamed up with or acquired electricity companies, so that the telecom operators and the power companies can offer products to each other’s customers.

This is particularly beneficial for telecom operators, as the market for renewables-based electricity is growing much faster than the communications market.

Customer Teaming Opportunity: Team up with utilities and other energy companies and use renewable energy to strengthen the bond with customers.

Collaborate and co-innovate with suppliers to reduce upstream footprint

A large share of overall emissions come from the supply chain that provides telecom operators with capital goods and other products and services. In some cases, where a telecom operators has already moved to renewables for its own power needs, these upstream emissions can account for over 80 percent of the company’s carbon footprint, making them the top priority.

Telecom operators can of course rely on suppliers to do their work, but it is more effective to team up and influence them. Most telecom operator procurement organizations have already implemented transparency measures for environmental, social, and governance (ESG) criteria, and they score suppliers on compliance. The most effective way to carry this out is using proven standards — GRI, to give an example. For large-scale strategic partners, such as network equipment manufacturers, the best way to measure ESG scores may be to modify one of the standard reporting frameworks.

More importantly, telecom operators need to communicate their priorities. Many telecom operators have already stated their goals for 2030, which in terms of technology is only two or three generations of radio equipment in the future, so roadmaps for their joint work with suppliers need to be shaped and set early. Questions to focus on include the following:

Should suppliers prioritize reducing telecom operators’ upstream Scope 3 emissions by reducing their emissions from production? Or should they prioritize telecom operators’ Scope 2 emissions by making their products more energy efficient? How can they help their customers use their products more efficiently — that is, how can they help reduce telecom operators’ downstream Scope 3 emissions?

In telecom standards with greater fluidity, should capital goods manufacturers focus on hardware or software? Custom hardware can be more energy-efficient, but it limits future flexibility. Software modifications tend to be less energy-efficient, but they enable customization. Analog hardware, such as 5G power amplifiers, offers further potential for optimization.

5G operators have made a significant push towards open hardware, such as OpenRAN, which is harder to optimize than a single-vendor end-to-end system. The business model of OpenRAN leads to a relatively large number of small suppliers. Consequentially, a much greater number of stakeholders need to be managed. How will telecom operators address this?

In service industries, the COVID-19 pandemic has led to effective off-premise working arrangements. Telecom operators can use this experience to include a reduction in travel-intensive on-site engagements in their supplier arrangements.

Teaming up with suppliers can extend to joint work on activities that are now in the scope of the operator. One example is the development of software for network platforms; the choice of programming language can affect the power consumption of an algorithm by more than a factor 50. Another example is management of the estate — especially the arrays of mobile base stations and power amplifiers: Networks and IT assets can be optimized for smart power management at the system, device, and configuration levels.

Value creation at telecom operators has largely been driven by agreed standards — such as the 4G and 5G standards and the resulting interoperable international networks — with an added layer of differentiation in the form of pricing and experience. If telecom operators can extend the thinking on standards — which is so engrained in the industry — to aligning their respective supplier roadmaps for decarbonization, the resulting cross-operator standard will be a powerful move. It will also be one that is aligned with the industry’s DNA.

Supply Chain Teaming opportunity: Draw a carbon transformation roadmap for the goods and services a telecom operator purchases. This is a complex and multi-disciplinary topic, which covers future technology, strategy for supplier relationships, and the impact of decarbonization. This type of teaming forms an overlay of existing discussions between telecom operators’ technology and procurement teams and suppliers’ teams. The complexity makes this activity difficult — but it is necessary.

New financing to accelerate the transition

Some telecom operators have already adopted green bonds to finance transformation projects that align specifically with green targets. So far, the market has not signaled spreads related to environmental ambitions, either in the form of a green premium or a green discount: Green funding is neither cheaper nor more expensive, aside from the greater effort needed to certify the underlying investments and measure their environmental impact. However, green bonds enable telecom operators to diversify their sources of capital, notably towards investors with a strong ESG focus. Though green bonds at present mostly focus on funding supply-side activities, such as network optimization, they could also fund projects to innovate in services.

By using PPAs to source renewable energy, telecom operators have become familiar with financial instruments that can secure their renewable energy needs. Using decarbonization purchase agreements, telecom operators could ask their customers to help fund specific decarbonization projects, offering a roadmap that uses IoT and automation. Many other industry sectors, too, are now familiar with PPAs as buyers of power. They could apply a similar concept to their purchases of telecom services by using them to reduce their carbon footprints.

Financial Teaming Opportunity: The greatest opportunity in the climate transformation for telecom operators is downstream, where there is a 2 to 3 percent revenue upside. Known financial instruments could be applied to take advantage of this opportunity.

Conclusion

The CDP reporting shows that the overall impact for the benchmark group of telecom operators is expected to be small. However, measures to reduce climate impact could be a driver of business development. In particular, four teaming opportunities could potentially be effective: alliances and co-investment for renewable energy; teaming up with and incentivizing customers for a renewable energy migration; joint, cross-industry supplier roadmaps to decarbonize the supply chain; and new sources of finance to fund the transformation.

Given the upside potential of these opportunities, telecom operators should enthusiastically embrace measures to limit climate change. Beyond the economic upside, we believe this would have direct, positive benefits for customers, employees, and shareholders.