Welcome to the 1st edition of our EMEA Banking Spotlight. In this short publication we aim to synthesise the key themes that we believe are top of the agenda for bank management teams.

After the whirlwind of change in 2016, the first quarter of 2017 was a time for banks to take stock of the new world and look at some of the major themes arising out of the political, economic, and market place changes seen in 2016.

After the dramatic rise of populism, banks must determine how their business models will adapt both to the long term challenge and the near term impacts of this change in environment. Below, we provide a brief update on what long term adaptation means, and recent responses to Brexit, arguably the most obvious impact of populism in EMEA.

Restructuring and regulatory reform have dominated the banking agenda since 2009, but the focus now has to be broaderLindsey Naylor, Partner, Financial Services

After 7 years of implementing regulatory constraints on financial resources, there are signs the tide may be turning. This may provide institutions a moment to evaluate their approach to resource allocation and product performance, which has often been ‘bolted together’ following the waves of regulatory change. We outline below the industry’s current positioning and views on how this can be improved.

Alongside the changing political changes, the market continues to face new opportunities. This quarter we released our State of Financial Services 2017 report at Davos. This year’s report focused on how banks can adapt to a broadly reordered marketplace, as digital technologies change how people live and work. We include a summary of the insights from the report below.

Is this new wave of change good or bad for the banks? We close with a spotlight on capital markets and how these themes will impact the wholesale banking and asset management industry.

BANKING IN AN AGE OF POPULISM

The events of 2016 raise the serious possibility that populism and nationalism will play a much larger role in advanced economies in the next several decades. If so, some key assumptions of recent decades may be reversed. We have identified 11 themes, some of which are highlighted below:

| Distinct roles for business and government | → | "Bolt from the blue" government demands, but also special favors |

| Relatively predictable economic policies | → | Frequent economic experimentation with more volatile outcomes |

| Low expected real returns | → | High demanded real returns to offset higher risks |

| International cooperation | → | National sovereignty |

In order to adapt to this new environment, we believe financial services institutions will need to make real changes to their business models. We have identified over 30, including:

- Consider more possibilities in strategic planning and risk analysis

- Take seriously the risk of war, hot or cold, including cyber attacks

- Diversify business, geography, and customers

- Change designs to function well in a balkanized world

- Increase capital and liquidity buffers

- Redesign products and services for a riskier and more volatile world

For a more detailed explanation, see our paper Financial Institutions in an Age of Populism. For more thoughts on the Trump administration specifically, see Implications of the Trump Administration for Financial Regulation

DRILL-DOWN: BREXIT BRIEFING

Over the past quarter, a “hard Brexit” is being seen to be increasingly likely – banks are now ‘planning for the worst’ defined as no passporting, limited or no equivalence judgements and no transition period. They also have started to work through the costly implications of amendments to the Capital Requirements Directive published last quarter that require banks to establish a single EU intermediate parent company if they have multiple EU entities or possibly even branches.

We expect both EU27 and UK based banks to take decisions on legal entity strategy and operational locations, managing the dual uncertainties around Brexit models and medium term regulatory changes during the next quarter, noting some have done so already. This will require:

- Definition of a plausible set of outcome scenarios (looking beyond Brexit to broader regulatory outcomes)

- Designing legal entity setups and quantifying economics for each scenario

- Deploying a coherent advocacy approach aligned to the scenario economics

- Developing and implementing a detailed action plan

THE NEW MODEL FOR FINANCIAL RESOURCE MANAGEMENT

Financial resource management has become exponentially more difficult in recent years, due to the proliferation of different regulatory constraints on capital (e.g. RWA, leverage ratios, regulatory stress tests, capital output floors) and liquidity (e.g. LCR, NSFR). Banks still struggle with the data, governance, and processes to manage these constraints, as well as the conceptual framework for what constraints matter when.

Going forward, banks will need to prioritise:

- Defining a conceptual financial resource framework that addresses the most important constraints for each segment, time horizon, and geography

- Setting up a central coordinating function to define objectives, develop metrics, and identify trade-offs

For more insights on bank’s current models and next steps, see our joint paper with IACPM on Financial Resource Management

TRANSFORMING FOR VALUE IN A DIGITAL MARKET

This quarter we released our report State of the Financial Services 2017 at Davos. This year’s edition focused on how banks can adapt to a broadly reordered marketplace, as digital technologies change how people live and work.

Virtually every service in the financial industry can be provided more efficiently and with greater customer delight than it is today using digital tools. To stay competitive, incumbents will need to “digitize to defend”: invest in digital transformation much more deeply. While dramatic cost reductions are possible, they will not in themselves create shareholder value, as most cost savings are ultimately passed on to customers.

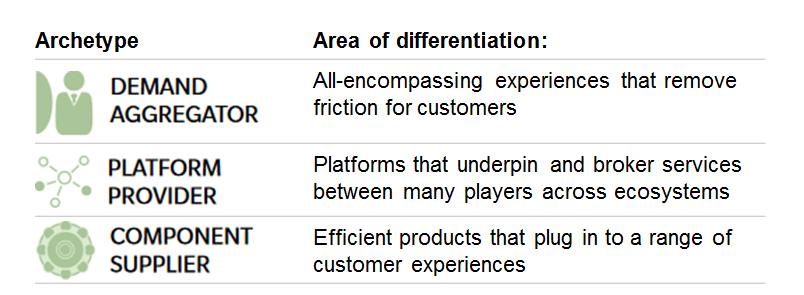

Incumbents looking to build and sustain new competitive advantages will need to also “go on offense” by organizing their overall transformation journey using three modular archetypes:

SPOTLIGHT ON CAPITAL MARKETS

In our 2017 Blue Paper with Morgan Stanley, we highlight how these factors of technology, politics, and regulation are creating a “world turned upside down” in wholesale banking, in which banks actually have a more positive outlook than asset managers. We expect that wholesale bank RoE will rise by 3 ppt to 2019, driven by decreased regulatory pressure and tech-driven restructuring. In contrast, we expect asset manager revenue to fall through 2019, driven by continued fee pressure and the rise of passive funds.