Industry Interrupted Report: The Roadmap to Healthcare’s Disruption

A new Oliver Wyman report suggests an innovative business model is soon going to disrupt healthcare’s status quo for good, especially as more incumbents and challengers begin – and continue – shaking up the market in areas of cost, regulation, and more. This shift –likely to be driven by customization – will occur even though the healthcare industry is still quite weak in certain foundational areas including affordability, value, and accelerated technological advance. And those resistant to change will need to step aside for those who embrace the coming healthcare revolution, as the time is now for healthcare’s long-awaited interruption. Here, in this report we outline just a few potential paths disruption will take in coming years.

Healthcare in the United States has long looked like an industry immune to disruption, with institutions too deep and interdependencies too intricate to allow radical change. Take, for instance, the division of the healthcare dollar: In 1960, 37 percent went to hospitals, 24 percent to doctors, and 11 percent to drugs; today, those shares remain effectively the same.

The rules of the game are well defined. To win, players need scale: scale in assets and facilities; scale in the ability to bundle services that align with benefit structures; scale in the ability to meet the broad needs of national employers; and, when negotiating, scale in the share of local market spending commanded. Scale has made those that achieve it essential to their markets, and in recent decades both payers and providers made sure to increase theirs.

Yet, even the most powerful business model can eventually run out of steam. Today, regulators are beginning to block mergers that limit competition as more and more geographies fall under the control of entrenched players; consolidations that do occur increasingly involve distressed assets. Both insurers and health systems are living with declining margins, which in turn has limited their ability to invest in the business. Companies are accelerating layoffs and looking for additional ways to reduce costs. The scale-based model may not be dead yet, but it is no longer a way to increase value.

Out With The Old

Worse, the traditional benefits of scale – cost synergies and efficiencies that deliver value to customers – have never been realized in healthcare. Players got bigger, but rarely better. It turns out achieving scale worked against innovation, ossifying the industry.

As the old business model withers, a new one is beginning to emerge. Based on our work with the healthcare industry and Oliver Wyman research of numerous other industries in disruption, we believe that in the next five years several foundational aspects of the healthcare market will be overhauled as organizations – both challengers and nimble incumbents – embrace new rules that are just now being written.

For healthcare, it is time to prepare for a post- scale world.

Unleashing The Value

One of the most important ways industries transform themselves is by exploiting trapped value. Trapped value is like potential energy for business: the difference between the value a company is creating and the value it could be generating, based on the needs of its customers.

Today the potential energy of healthcare is high, as both consumers and employers suffer with less-than-optimal products, high costs, and inefficiencies across the value chain:

- Costs have increased drastically, but outcomes are not demonstrably better

- Pricing is opaque, and it is difficult or impossible to assess the value of the product

- The experience of interacting with the system – across health plans, providers, and pharmacy – has remained complex, confusing, and frustrating

- Product evolution is painfully slow, with little innovation or differentiation

- The industry is dominated by generic offerings that try to serve everyone, and therefore serve no one well

As healthcare’s trapped value accumulates, the demands and expectations of consumers, employers and policymakers are mounting as well, with the gap between what is wanted and what is offered widening. Bottom line: Consumers, employers, and policymakers find healthcare’s seeming inability to provide affordable care efficiently, consistently, and conveniently to verge on the intolerable.

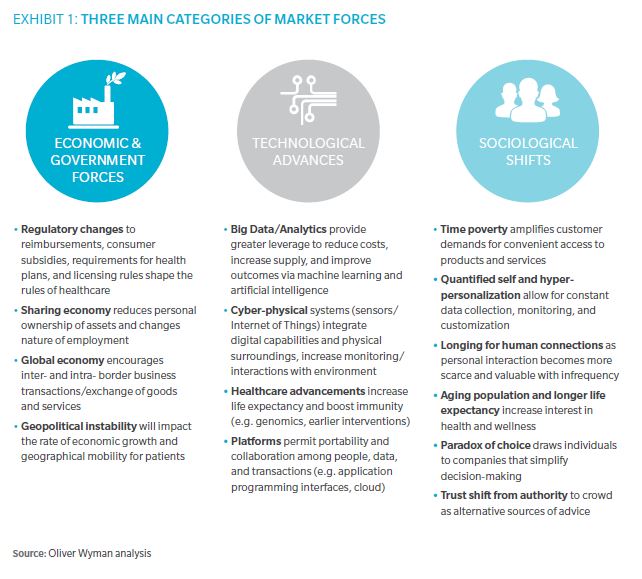

Clearly, the company or companies that unlock healthcare’s trapped value will reap rich rewards. And the catalytic regulatory, technological, and social forces that have fueled the rise of Amazon, Google, and many other innovators are increasingly being felt in the healthcare arena. Regulatory changes are enabling new reimbursement models; new data sources and insights promise to revolutionize diagnostic capacity and personalized care; and consumers are beginning to expect their doctors and insurance companies to provide the same convenience and personalization as online shopping or ordering a Lyft. (See Exhibit 1)

As these forces take hold in healthcare, they will make it possible to compete and deliver value in new ways: Organizations will deploy their resources differently, investing in a new and different mix of assets. The basis of commerce, profit, and strategic control will shift to respond to a new set of rules.

Three Paths To Interruption

Other industries provide clues to what a post-scale healthcare world will look like. In each industry that has faced interruption, we recognize in retrospect how releasing trapped customer value through business- design innovation has dramatically reshaped the industry. Whether we’re talking about brick-and-mortar stores versus Amazon or networks versus streaming, the shifts in value and relevance have been enormous.

The real question is, "Who or what will be the disruption that forces healthcare out of its increasingly less profitable comfort zone?"

We see three vectors along which healthcare’s interruption is likely to occur. Each addresses core elements of the value trapped by the industry today. Each is already beginning to move from ideas and hypotheses to evidence and momentum. Taken together, the three provide the basis of a new, post- scale healthcare industry that operates in a fundamentally different way.

Edging Towards Customization

As an industry, healthcare has favored standardization. On the payer side, this means one-size-fits-all insurance plans with nearly identical coverage and networks; on the provider side it means an office experience that’s the same for a healthy millennial or a person with complex, chronic illness. As a result, it’s almost always too slow and unresponsive to serve the needs of the acutely ill, but it’s also too cumbersome, expensive, and inconvenient for everyone else. Formal structures, such as regulation and an intractable business model – especially when coupled with ongoing market consolidation – have reinforced this approach.

The industry’s first steps in the direction of customization and personalization have been rather tentative. Insurers and providers have created more focused business-to-business bundles based on relatively standardized episodes of care, such as hip and knee conditions, but they have not translated these into a form that lets consumers make productive choices among them. They’ve created new, narrower provider networks, but the focus in almost every case has been on controlling costs, not improving patient experience.

Meanwhile, digital entrepreneurs have created a dizzying number of new products designed to capture some of the health and wellness coverage that has crept into health plans. The explosion has confused consumers with too many or unclear choices, and most have opted to remain on the sidelines for now.

That said, we expect to see the pace and depth of change grow in the near future, as healthcare organizations use targeted, curated solutions to unlock value. And there are early signs across the industry that this sort of unbundling and customization is starting to take place. For instance, several companies are finding success with innovative packages and services targeting specific segments of the Medicare Advantage population. And health plan innovators are beginning to target younger consumers not well served by one-size-fits-all healthcare by offering convenience-oriented service bundles that include telemedicine, online interfaces, and convenient retail storefronts.

Unbundling and customization have many precedents across industries. In retail, a business model once based on in-store and catalog-shopping only has given way to a model where consumers can also buy online and pick up in the store or have the product delivered home. In the latest iteration, some retailers like Bonobos or Everlane offer only a limited number of garments in stores that customers can try on and then order them online on the spot.

The cable industry once sold content in the form of packages of cable channels – premium and basic. Today, it is watching consumers walk away from packaged bundles and turning to curate-it-yourself alternatives like Netflix and Hulu.

Unbundling services and products is a challenge for established industry players, but it offers opportunities for companies to understand their customers better so they can meet their needs better. Whether established players in healthcare wish to take advantage of the situation or not, the industry today is starting to face many of the same conditions that allowed – and ultimately forced – these other industries to transform almost overnight.

The New Front End

Healthcare today establishes and maintains “relationships” with consumers through its management of their care. For the integrated health system, the predominant front end is primary care; for pharmacies, it’s local retail counters; and for health plans, it’s the point of enrollment or activation. For most customers, the traditional models are wildly inconvenient, difficult to access, and seemingly expensive most of the time.

The past two decades have seen a proliferation of new access models for lower-acuity episodes – telehealth, urgent care, retail clinics, and the like – plus services like mail- order prescriptions and member portals. Yet, these innovations have done little to change how consumers actually utilize the system. And even if they were fully used, these models fall short of our experience in every other aspect of life.

We have come to expect our interactions with business and other institutions to be ubiquitous, on demand, and personalized. Healthcare is none of these things. As a result, a growing segment of healthcare consumers – led by millennials, family caretakers, and price-sensitive consumers with high deductible coverage – is primed to choose a different path the minute someone is smart enough to offer it. That they haven’t already is either a sign that the new access/interface models are not well known enough yet – or the new models just aren’t giving the public what it needs.

As consumers, we’ve learned to use, and often love, new front ends in many areas of life – from Apple’s App Store to Facebook’s half- newspaper, half-watercooler feed, to Amazon’s virtual megamall. These technology-enabled access models don’t just help us get what we want, where and when we want it – they also build intimate relationships with us.

A similar process has begun to play out in healthcare. Consumer-facing processes like scheduling and health-plan enrollment are increasingly automated, and additional functions, such as billing and payment, are attracting similar interest and investment.

More important, we’re seeing the emergence of healthcare platforms that help consumers select physicians, understand their conditions, and connect with health and wellness tools, all in a highly personalized way.

Meanwhile, clinics in pharmacies and other retail outlets like Walmart are gaining traction, covering more conditions and offering attractive prices. But their real potential is not just in offering more locations for care. Rather by embedding the front end of care in the texture of our daily lives, they can begin to make healthcare immersive and ubiquitous.

As these changes and others spread through the industry, it will be increasingly easy – and attractive – to “cut the cord” to traditional healthcare.

New Information And Intelligence

Healthcare today is organized around experts – physicians, researchers, actuaries – whose training and experience put them at the center of healthcare decision making. They are a vital resource, but also a bottleneck – an entrenched power structure resistant to change. And in an age of exponentially increasing healthcare information, there is more and more reason to wonder how – and whether – they can keep up.

At the core is the physician. The healthcare industry’s fundamental unit of activity is the doctor visit; health plans are organized around physician networks; the regulatory system centers on licensure and reimbursement limits. As biological understanding and medical science have advanced generation by generation, we have counted on the clinician to serve as the channel through which that knowledge is translated into optimal health outcomes.

While physicians will continue to play a central role, care as a process is going to change. Over the past two decades, healthcare has created an ocean of data on clinical encounters, claims, prescription drug fulfillment, and much more. In theory, this data should enhance the effectiveness and efficiency of physicians and other skilled professionals. In practice, however, progress has been slow.

There are certainly solutions in the market to help segment populations, identify gaps in care, and predict and prevent health exacerbations. But for the most part, they are reactive and limited in scope. In particular, they use very little data about the “me” being served – my benefit, the product I buy, my experience, my treatment, my role in an actuarial pool. While healthcare can be rightly considered a data business, it has struggled to be an information business. And the way we deploy and utilize human talent has changed almost not at all.

However, this situation should change dramatically over the next decade. First, the amount and nature of available information is beginning to explode: New data is entering the system from rapid advances in genomic, proteomic, and biomic analysis; from capture and mining of clinical data across an increasingly ubiquitous electronic medical record (EMR) infrastructure; and from user- generated data from wearable devices and smart(er) phones. And second, advances in computer science have reached a point where machines can be used to make sense of the enormous pool of data, apply intelligent and learning algorithms, and deliver insights beyond the intrinsic ability of unassisted human intelligence.

Organizations that harness this new level of data to generate deeper insights about populations and individuals will be able to outperform and extend human capabilities, drawing on immense pools of information and analyzing them with advanced analytics and artificial intelligence. They will extend our knowledge of significant patterns and relationships affecting health. The tools may be new, but the dynamic is old and powerful: Better knowledge leads to better medicine.

New Models, New Opportunities

These three vectors of change are conceptually simple, but their implications are immense.

The new healthcare industry they point toward will be smarter. Consumers will be better, more intimately served by those who provide care. Their treatment will be differentiated by condition, stage of life, and other personal factors. Insights about each individual will be as important as overall populations, or even more important. Information will be the basis of new business models – for incumbents to embrace as their future or for challengers to exploit in disrupting the status quo.

Most significantly, this new system will be capable of learning – about people and their needs, as well as the roots of disease and the effectiveness of treatments. It will help us figure out how to engage and motivate patients to care for themselves and how to empower healthcare professionals to do a better job for more people.

Over the next decade, if not sooner, we expect to see the emergence of a healthcare system radically different from what any of us – either as consumers or as members of the industry – have experienced. Value and strategic control will no longer be based on scale. Business designs, operating models, profit models will all be reborn in forms that we’re only now beginning to understand.

To participate in that change will not be a check-the-box exercise. It will demand an extraordinary level of commitment, not just to the profitability of companies but to understanding and connecting with a new kind of consumer – and allowing their needs to guide us in the right direction.

US healthcare has delivered enormous value – to the population, the economy, and the global base of scientific knowledge. Its next contributions will almost certainly arise out of interruption and reconfiguration.

In a new world with new rules, industry has an opportunity to unleash new value, using new technologies and processes in new and unexpected forms. It is up to leadership teams – boards, senior executives, and medical leaders alike – to rise to the challenge.