New Front Door to Healthcare: Retailers Take Starting-Point Advantage

In its recently released report “The New Front Door to Healthcare is Here,” Oliver Wyman predicts that consumer use of alternative sites for care - such as retail clinics, urgent care, and telehealth - is only going to increase. As a result, $200 billion in current healthcare spend could flow from traditional sites of care to one or more of these new options. Much is at stake for all industry players, but retailers, in particular, will play a significant role in the new front door. With their existing customer base, brand loyalty, physical footprint, and health resources, they have a starting-point advantage. Yet the report, which includes findings from a survey of more than 2,000 individuals, concluded that not all retailers are created equal (in consumers’ eyes). Every retailer must think strategically about pairing its offering with its customer base. Here, Oliver Wyman Principal Graegar Smith presents five key considerations of the new front door for retailers:

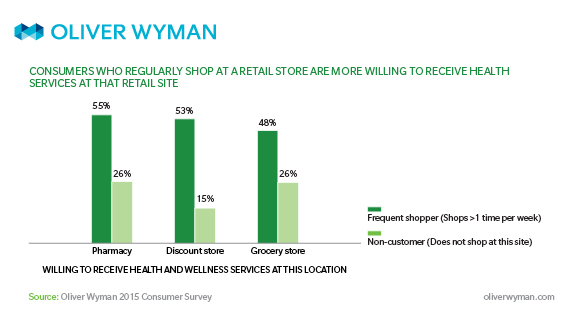

1) The survey shows “frequent shoppers” are very willing to receive health services in a retail location. In other words, retailers’ best customers are all in.

Market meaning: If a retailer doesn’t meet frequent shoppers’ desire for health services, chances are someone else will. For frequent shoppers, health services can increase per-customer revenue and margin. And for the infrequent shoppers, health services can drive traffic to retail stores and be a vehicle to build customer loyalty.

2) Health services could be a standalone business, or it could be something much broader and encompass the entire store, changing a retailer’s core offerings and adding new ones.

Market meaning: Competition is much fiercer if the stated goal is “stealing” share/revenue from incumbents. The pie is bigger if retailers go after the broader health and wellness play; but the path to get there is also more difficult.

3) Depending on the offering a retailer is pursuing – just healthcare or a more complete model with nutrition and wellbeing services – the business model required will, obviously, vary.

Market meaning: If the “customer” is the payer or employer, the profit model must be built around getting reimbursed for the services delivered. If the “customer” is a risk-bearing provider, the value proposition is retailers’ ability to extend the care team into the store, deliver an expanded set of services, and gain a share in the value created. If the “customer” is a consumer who is buying-up health and wellness services, the model is focused on capturing consumers’ discretionary budget for services such as fitness and nutrition.

4) The capabilities and partnerships required will be determined by the business model retailers pursue. Running a successful healthcare business within a larger retailer requires a different skill-set and resources, and retailers are going to need help.

Market meaning: The answer may be more retailer-to-retailer partnerships. From a contracting vantage, a coalition of regional retailers all offering a common program could be attractive and a credible alternative to national retailer offerings.

5) Grocery and mass merchants have a unique bar and higher hurdle to overcome, as some consumers have an aversion to healthcare in a setting that sells food or general merchandise.

Market meaning: There is clear opportunity for all retailers; it just will require more work and strategic business models. Grocers and mass retailers may be able to overcome consumers’ aversion using other attributes, such as price or experience; or by increasing reliance on provider partnerships to gain credibility.