-

-

-

-

Link copied

Link copied

-

-

-

-

Link copied

Introduction

The North American industrial goods sector is a testament to resilience and innovation, remaining strong amid turbulence. Sectors such as semiconductor equipment, industrial software, and building technologies are leading the charge, benefiting from favorable policies and trends in digitalization and automation. The US and Canada have a significant share of some of these high-performing subsectors, which are shifting value away from industrial conglomerates, as well as away from Europe. A further trend in industrial goods is the growing emphasis on sustainability, with regulatory requirements and customer demands pushing companies toward transparency and reduced emissions.

Looking ahead, the sector remains attractive for investment. With a generally positive outlook of bases analysts’ recommendation and an 81% favorable view of industrial goods companies, the sector is poised for continued growth and innovation.

These findings and other details in our “The State Of The Industrial Goods Sector” report are based on an analysis of more than 1,000 publicly listed companies worldwide, in addition to an online survey and our experience as trusted advisers in the industry.

Key findings and trends in the North American industrial goods sector

The industrial goods sector has shown growth amid change, with key trends emerging:

- Resilience: The sector has shown a remarkable ability to weather the recent upheavals caused by the pandemic, inflation, geopolitical turmoil, and supply-chain disruptions, as evidenced by a 12.3% average EBIT margin over the past 10 years.

- Shift in value: There have been significant shifts in value among subsectors like semiconductor equipment and industrial software, primarily at the expense of more traditional subsectors such as industrial conglomerates (which had a less than 1% average sales growth).

- Leadership in technology: The performance of semiconductor manufacturing equipment (22% average EBIT margin and 19% average sales growth) and industrial software (14% average EBIT margin and 11% average sales growth) shows that sectors capitalizing on digitalization and automation are experiencing a surge in value.

- Sustainability focus: Increased emphasis on sustainability (59% of firms are net-zero committed) is driving a trend toward greater transparency and emission reductions, though comprehensive reporting, and target-setting lag.

- Regional dynamics: North American firms are outperforming, increasing their global market cap share to 37% from 33%, partly due to supportive policies like the Inflation Reduction Act (IRA) and the Buy American Act.

- Future prospects are optimistic: The overall sentiment toward the sector is more positive (81% received “outperform” or “buy” recommendations) now than in the past decade, indicating readiness for continued growth and innovation.

Chapter 1

The North American industrial goods sector shows resilience and innovation

Overall, industrial goods have been a relatively safe harbor in turbulent times. However, significant variability exists across subsectors. Semiconductor equipment and industrial software stand out as frontrunners, outpacing others in terms of profitable revenue growth. Similarly, industrial components and building technologies are ahead of the average growth rate of industrials overall. Conversely, certain sectors consistently lag, notably conglomerates, as well as production systems and plant engineering.

North American companies perform better than the other regions in the study in both market value inflow and operational performance. Driving that trend is their high share of structurally outperforming subsectors, as well as other factors including lower energy costs, more streamlined regulation, flexible staffing strategies, and a stronger commercial, profit-driven mindset prevalent among management and stakeholders. With a long-term profitability rate of 12.3%, the sector not only demonstrates its enduring resilience, but also its adaptability in the face of ongoing challenges such as supply-chain disruptions.

Exhibit 1: Development of operating performance in North American industrial goods sectors

Weighted average sales growth and EBIT-Margin 2013-2022

Source: Company sample, S&P Capital IQ, Oliver Wyman analysis

Chapter 2

Shifting value from traditional subsectors to those specializing in technology and innovation

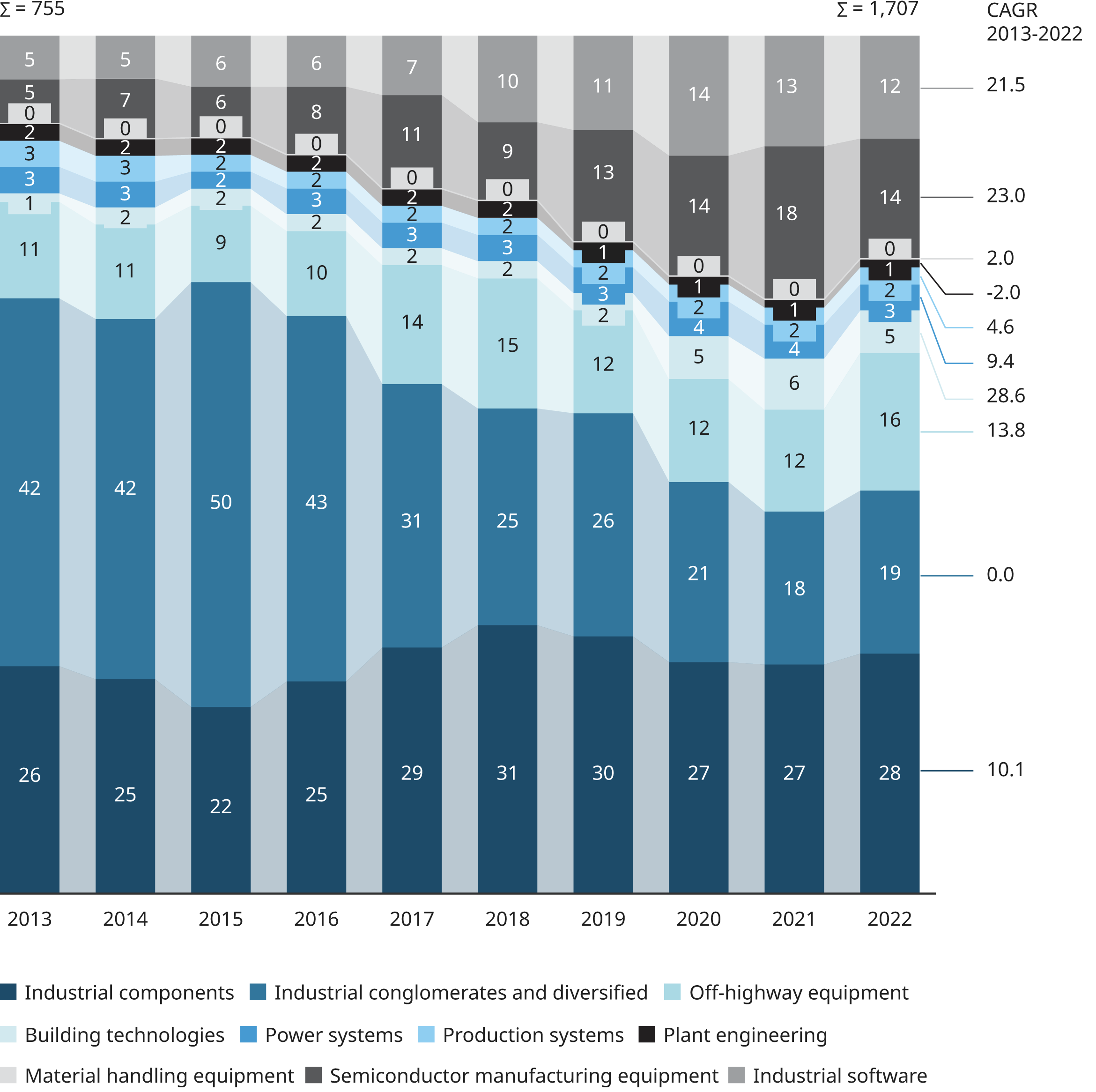

The industrial landscape is witnessing a significant shift in value among subsectors. Firms specializing in building technologies, semiconductor manufacturing equipment, and industrial software are experiencing a surge in value relative to the overall market capitalization of the industrial sector. This growth is primarily at the expense of more traditional subsectors, indicating a changing paradigm where technology and innovation lead the way.

Exhibit 2: Sectors that have been clear winners in the last decade

% of total, US$ billion

Source: Company sample, S&P Capital IQ, Oliver Wyman analysis

The sectors leading this transformation — notably building technologies, semiconductor equipment, and industrial software — have capitalized on major industry trends such as digitalization and advancements in factory and process automation. The off-highway equipment sector has particularly benefited from legislative support like the IRA, demonstrating a substantial increase in value from 2021 to 2022. Traditional industrial conglomerates and areas such as material handling equipment and plant engineering are experiencing a decline, meanwhile, reflecting a shift in investor focus and optimism.

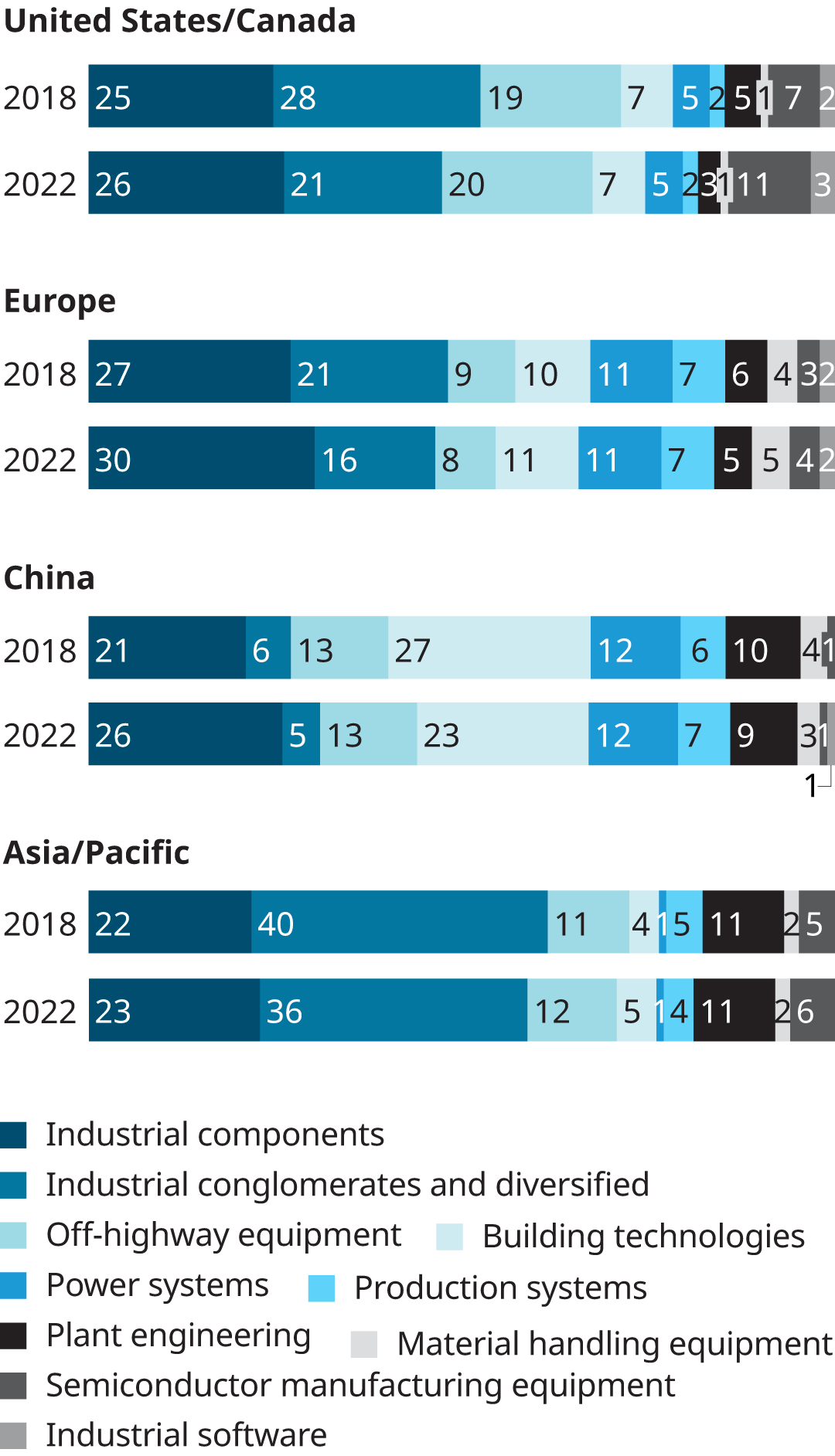

Exhibit 3: Revenue share and sector mix of industrial goods by region

Note: Percentages may not sum to 100% due to rounding

Source: Company sample, S&P Capital IQ, Oliver Wyman analysis

The regional analysis reveals that the US and Canada hold a significant portion of the high-performing subsectors, driving a notable shift in value to those regions. This is further evidenced by the market share of North American firms, which grew from 33% to 37% of the total global industrial goods sector’s value from 2021 to 2022. This trend is not only a result of the inherent strengths of these subsectors but also the direct and indirect impacts of policies such as the IRA, the Infrastructure Investment and Jobs Act, and the Buy American Act.

Exhibit 4: North America has been the beneficiary of a recent shift in value

Source: Company sample, S&P Capital IQ, Oliver Wyman analysis

Chapter 3

Sustainability takes center stage in the industrial sector, but reporting still lags

In recent years, sustainability has become much more critical to industrial firms. This heightened emphasis is driven by several factors including regulatory disclosure requirements and increasing demands among customers for transparency about products’ carbon footprints. Additionally, financial institutions are steadily incorporating environmental, social, and governance (ESG) criteria into their lending decisions, with interest rates and credit approvals now often contingent on meeting these standards. Institutional investors and asset managers consider those criteria more and more when making investment decisions as well.

Most industrial companies have embarked on the sustainability journey, albeit at varying paces. The many that set Scope 1 and 2 targets (for direct and indirect greenhouse gas emission levels, respectively) from 2018 to 2022 managed to reduce their emissions by 24% in that time frame. That’s clearly a move in the right direction, though it trails the 37% reduction for all European companies reporting. It’s also worth noting that taking 2021 as a base (it is the last year with full sample availability), only 60% of firms are reporting their Scope 1 and 2 emissions at all.

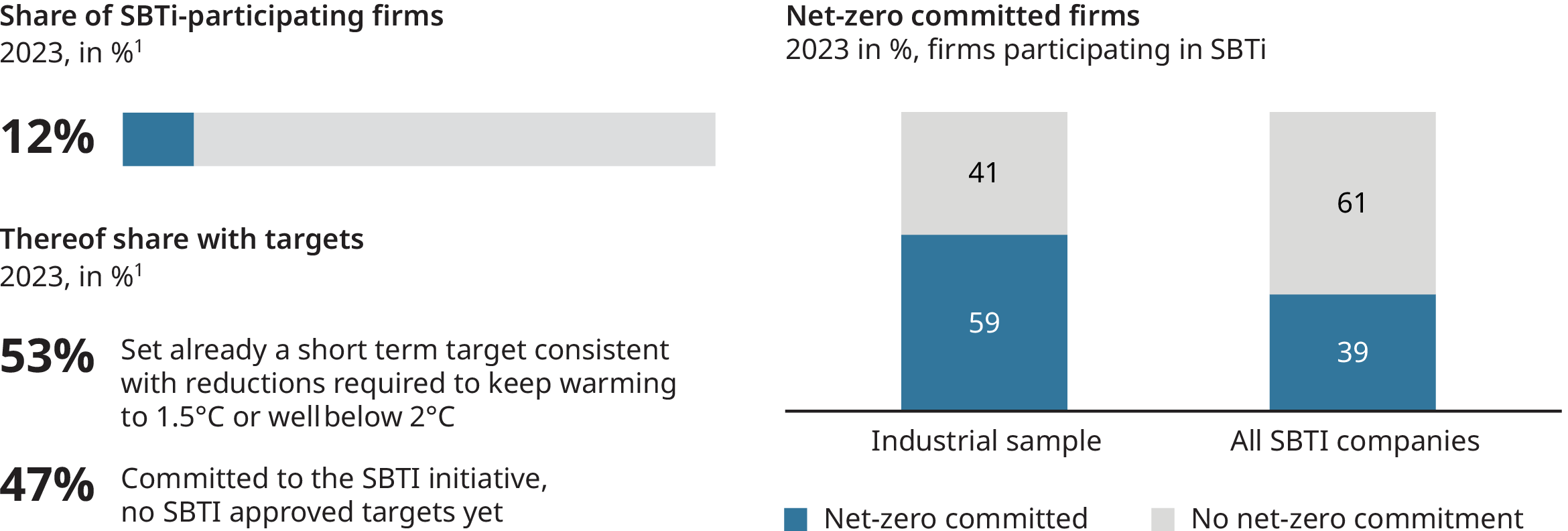

Exhibit 5: Net-zero commitments of industrial goods companies are above average

Note: 1. Scope of data sample from 139 listed US and Canadian companies in 2022

Source: SBTI, Oliver Wyman analysis

While the reluctance to disclose might be attributed to the challenges involved in baselining and modeling carbon data, this type of transparency is not just a regulatory expectation; it is increasingly demanded by customers, making it business critical. Consider target setting: Around 60% of all industrial firms in our sample report Scope 1 and 2 targets. However, only 12% are participating in the Science-Based Targets initiative (SBTi), one of the leading non-governmental institutions approving emission targets. Of those 12%, just 53% have an approved target for 2030 that is aligned with the Paris Agreement goal of limiting the average global temperature increase to 1.5°C above preindustrial levels. Additionally, only 59% of SBTi-participating firms have committed to net-zero greenhouse gas emissions.

Chapter 4

Navigating the future of the North American industrial goods sector

The industrial goods sector has a strong mid-term future with numerous opportunities in the pipeline, including artificial intelligence, low-carbon technologies, and new markets. However, inflation, geopolitical turmoil, and potential recessions pose major risks. Industrial firms must navigate these dynamics with skill and foresight. Success will hinge on striking the right balance between making bold, transformational moves to align with long-term structural trends and maintaining strategic flexibility to adapt to potential disruptions. The coming years will be pivotal for the sector, promising to be as full of surprises as the previous ones.

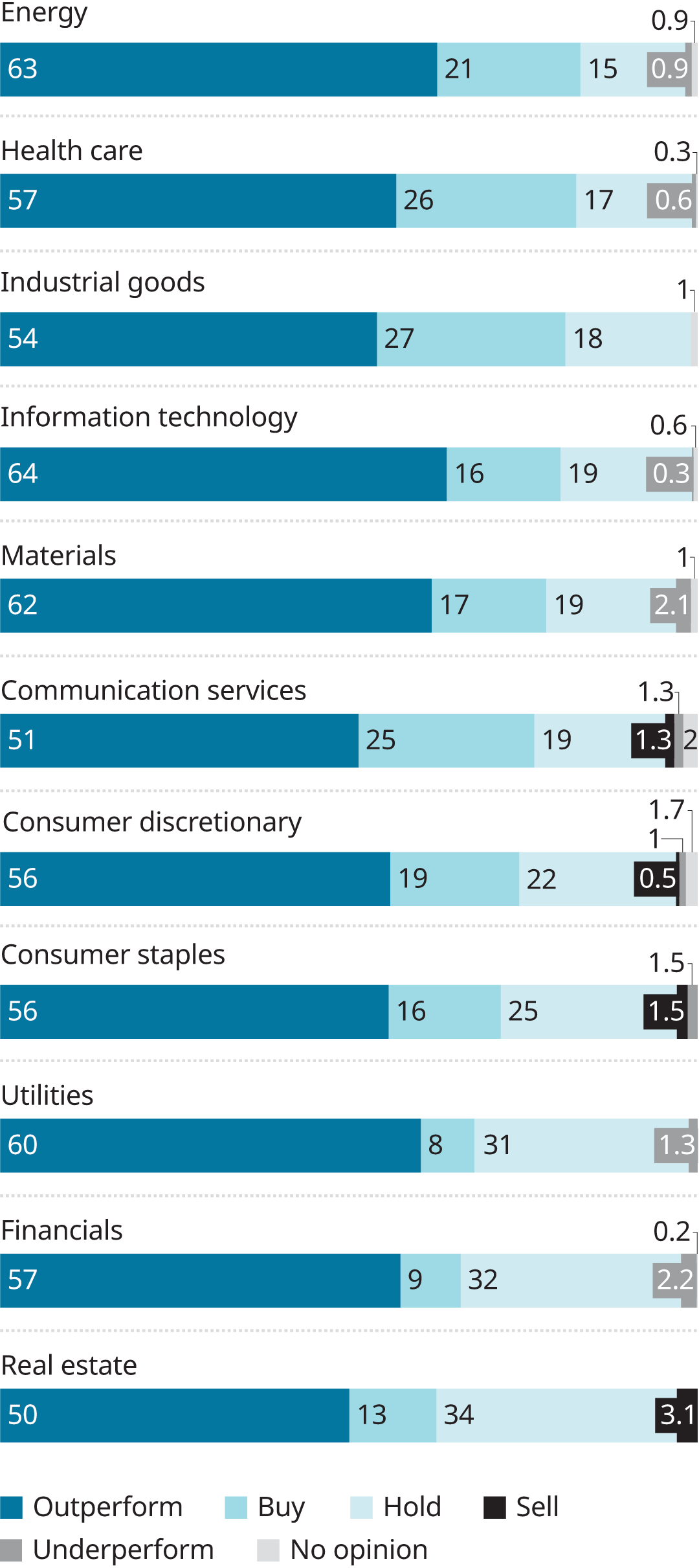

Exhibit 6: Analyst recommendations for investment in North American industries

Ranked by sum of outperform and buy recommendations

Note: Based on 3070 listed US / Canadian companies with a total revenue >100 mn USD in 2022

Source: Capital IQ, Oliver Wyman analysis

The overall sentiment toward the industrial goods sector is more positive now than it has been in the past decade, with 81% of companies viewed favorably. This optimism underscores a sector poised for continued growth and innovation, ready to confront the challenges and capitalize on the opportunities that lie ahead.