The US business environment was surprisingly robust for most of 2021. Consumer spending bounced back after the COVID lockdowns and other restrictions of 2020, while companies enjoyed low interest rates, and government spending boosted growth. But conditions started to change towards the end of 2021 with rising prices and supply chain disruptions. In 2022, interest rates are expected to rise, the Federal Government’s spending package will be smaller than originally expected, and lenders will be more stringent on their covenants.

For these reasons, we expect that corporate restructuring will increase in the second half of 2022 and into 2023. A majority of these cases will be a success: Operations will be maintained, and business and financial positions will be strengthened. However, it’s essential that companies recognize the growing headwinds early, be realistic about upside and downside scenarios, and take action. The companies that are well prepared will be the most likely to restructure successfully – or avoid doing it at all – and to succeed in the future.

Today’s market disruption starts with consumers and employees, who are emerging from the last two years with radically different perspectives and tastes than in the past, as illustrated by a recent article from the Oliver Wyman Forum. These changing demands will be a moving target for businesses. At the same time, many businesses have been facing commodity price increases, labor shortages and supply chain disruptions since late 2021. These and other factors are causing revenue declines and have pushed inflation higher, which will contribute to higher costs over the next year.

This will result in cash shortages for some companies. In 2021, it was common for a company to avert a liquidity crisis by taking on additional debt, especially when its problems were due to short-term factors. But additional debt can also lead to unsustainable interest payments and further pressure on the business.

In addition, there are three major shifts that add to the difficulties in the business environment.

- First, capital markets were strong and interest rates were low in 2021. Financing was easy to come by, which let companies refinance easily and allowed distressed companies to take out additional debt to cover performance issues.

However, the strong capital markets of the last few years will most likely weaken. The Federal Reserve is expected to raise interest rates in 2022, likely in the first quarter, increasing borrowing costs. By 2023, the benchmark overnight lending rate is expected to be at least 1%, compared with the current range of 0% to 0.25%, where it has remained since March 2020. If inflation rises as expected, it may lessen the burden of existing debt. However, increased borrowing costs will pose a major problem for companies with maturing debt that are looking to refinance. - Second, the Federal Government provided stimulus to help individuals and businesses that struggled during the COVID pandemic.

But this has already been reduced from pandemic highs and will likely not be readily available, as concerns loom large over the government’s debt ceiling. This shift has been highlighted by the reduction in the Democrats’ proposed spending bill from $3.5 trillion to under $2 trillion. - Third, banks and other lenders were more willing to negotiate restructuring options and delay foreclosures in 2021, because the favorable economic conditions led them to believe they would recover more by letting business operations continue. This was aided by flexibility that covenant-lite credit documents afforded to debtors.

However, banks are likely to return to foreclosing on assets. That, combined with the slow return to normal financial market conditions, may leave a similar number of companies in distress but without the safety nets they had during late 2020 and early 2021.

As economic conditions change dramatically, otherwise stable companies could suddenly find themselves with an unsustainable capital structure, despite the best efforts of management. Alternatively, overly burdensome covenants might preclude the company from further investment. Or the company might not be able to refinance, due to either changed macroeconomic conditions or a diminished perception of its credit quality.

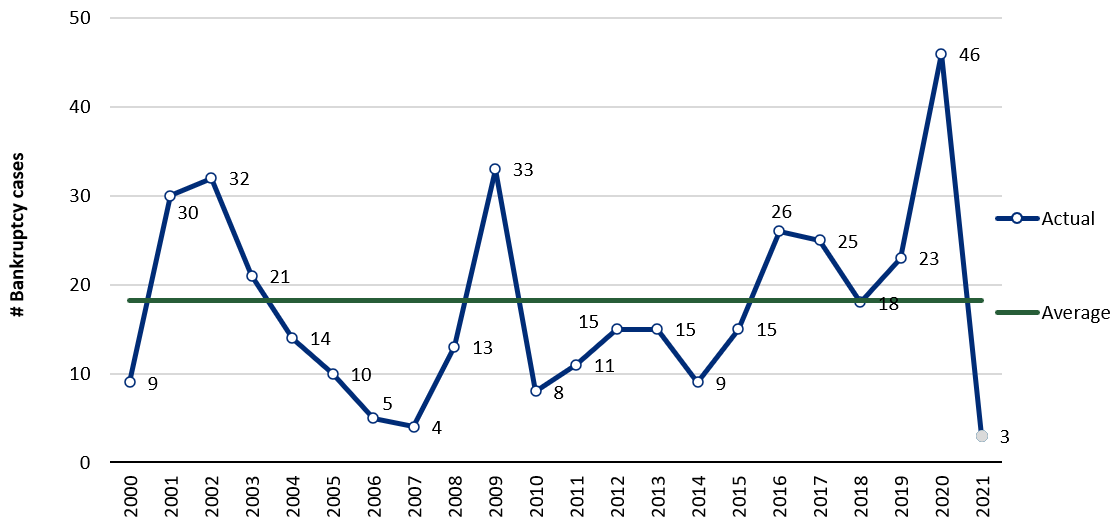

While US Chapter 11 bankruptcy filings increased in 2020 due to pandemic-related disruptions, the number declined in 2021 due to the unexpectedly favorable conditions. But in 2022 and 2023, we expect both informal and formal restructurings to increase.

To avoid restructuring – or at least to enable an out-of-court restructuring – companies should recognize these new headwinds conditions early. We think it is essential for companies to keep three imperatives top of mind: First, manage cash forecasting closely, including debt covenants. Second, develop robust contingency plans. And third, ensure they have capital available beyond their expected needs. The future takes shape in unexpected ways, and fortune favors the prepared.

Thanks to Josh Korn for contributing to this article.