-

-

-

-

Link copied

Link copied -

Oliver Wyman’s Clean Energy Startups Radar analyzes the annual flow of venture capital (VC) into startups providing solutions to the energy market that enable the transition away from fossil fuels. It also identifies which technologies investors are finding most promising. In a bid to drive decarbonization, non-emitting power generation is the single largest category of expected spend. As a result, traditional energy, manufacturing, and construction players will need to scale up at an unprecedented pace, while ensuring that the quality of the assets they are building is not impacted. Organizations will need to find more effective ways of planning and designing projects, and the construction industry will need to rethink the approach to productivity if they are to succeed in the coming infrastructure boom.

Using Crunchbase data in our analysis, the Radar provides an overview of VC activity in early-stage commercial development by tracking the funding for more than 800 companies involved in everything from power generation and grid operations to storage and carbon accounting. It also calls out the most significant deals and regions driving funding growth.

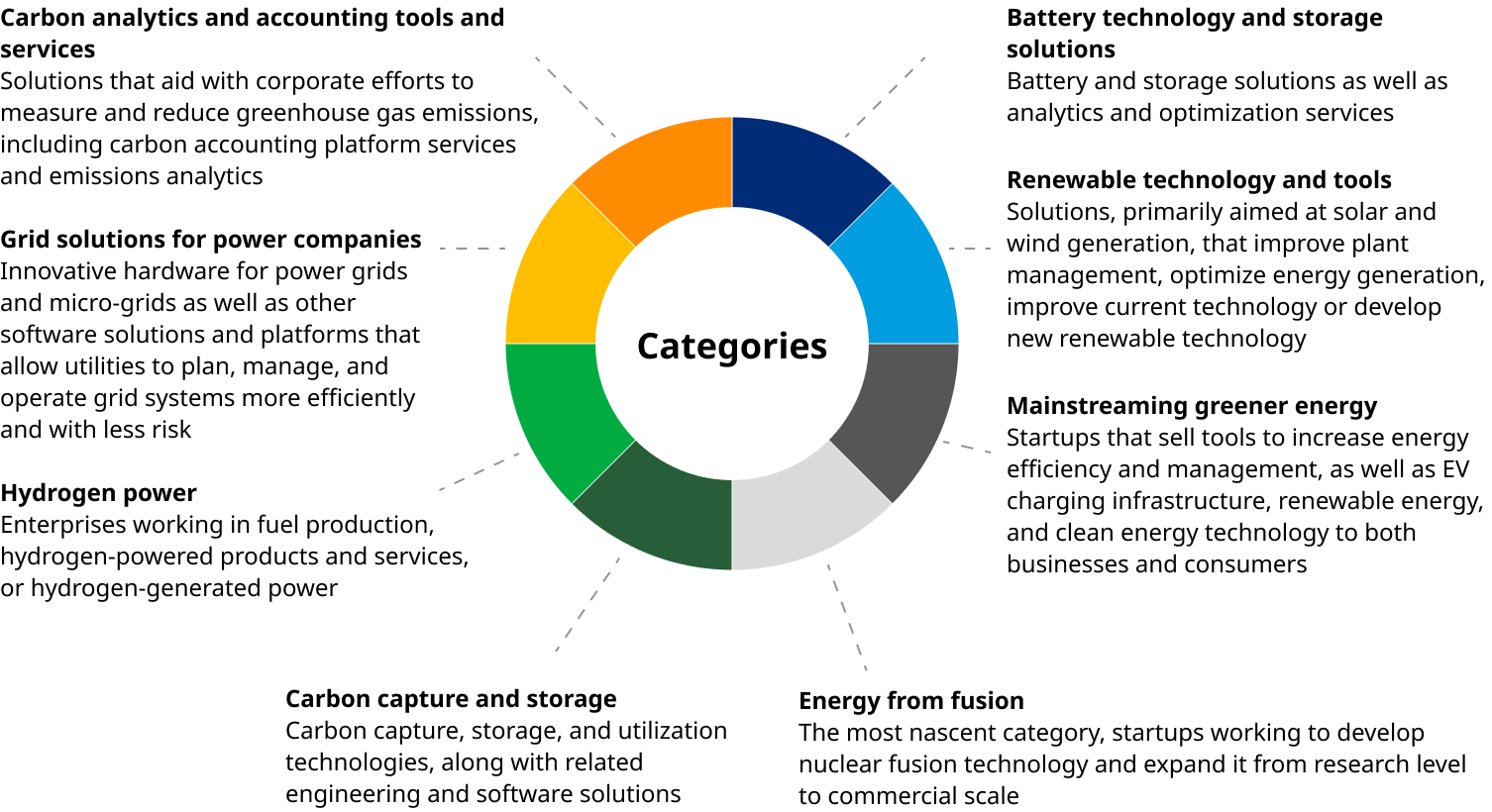

Exhibit 1: Categories of clean energy startups assessed in this analysis

Source: Oliver Wyman analysis

Avoiding economic pressures

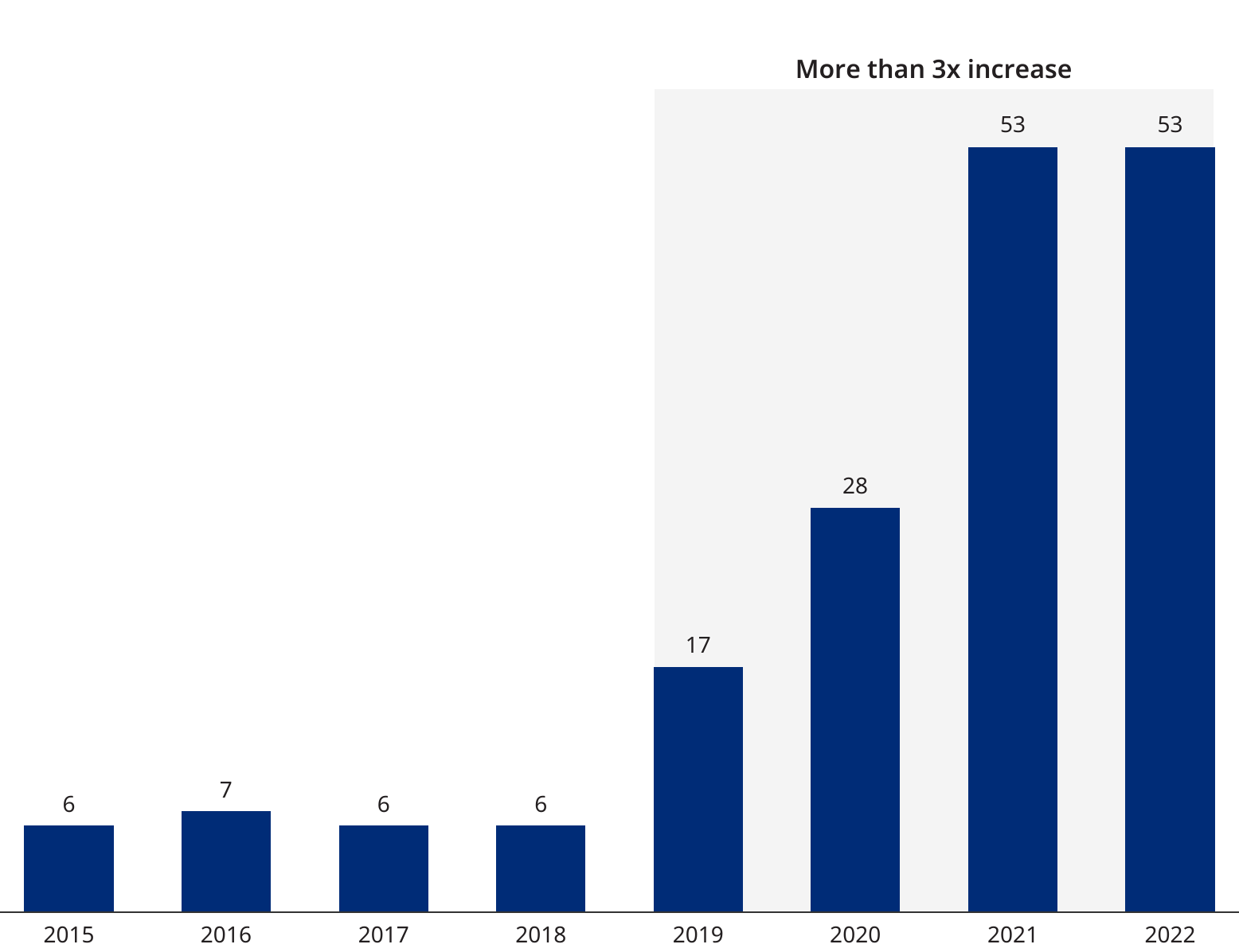

Total global VC funding in clean energy startups has increased dramatically over the last three years, growing more than sixfold from $1.9 billion in 2019 to $12.3 billion in 2022. This is despite a contraction in the broader VC market caused by the rise in interest rates and the subsequent tightening of liquidity. In 2022, overall VC funding across industries fell 53% year-over-year.

In stark contrast to funding for other sectors, such as mobility which saw its VC support drop 62% to $31 billion, investment in clean energy startups increased 10% in 2022 over 2021. While that was slower than the category’s growth between 2019 and 2021, the sustained expansion despite economic pressures reflects the VC market’s expectation that new solutions to facilitate an energy transition will be a top business priority moving forward. [For more data on mobility startup funding, please see Oliver Wyman’s Mobility Startup Radar.]

No doubt, green energy has been helped by catalysts like the Inflation Reduction Act (IRA) in the United States and corresponding measures in the European Union, such as the Net Zero Industry Act. Both new laws aim to reduce red tape around regulation and increase subsidies for clean energy solutions, with a significant potential to amplify investor interest in the sector in these regions.

Exhibit 2: Global venture capital investment in clean energy startups

In US $ billions

Source: Oliver Wyman analysis

Funding for clean energy startups is reaching record highs, despite the ripple effects from a host of economic pressures, including COVID-19, mounting geopolitical tensions, a VC liquidity crunch, and rising interest rates

Thomas Fritz, partner, Energy and Natural Resources, co-head of Climate and Sustainability, Europe

The rise in mega investments

The increase in funding has been driven in part by higher-than-average deal sizes, along with individual mega investments of more than $500 million each. The average deal size jumped more than threefold from $17 million to $53 million between 2019 and 2021 and then levelled off in 2022. The larger deals reflect the more mature status of the startups being funded, which have usually already reached development stage.

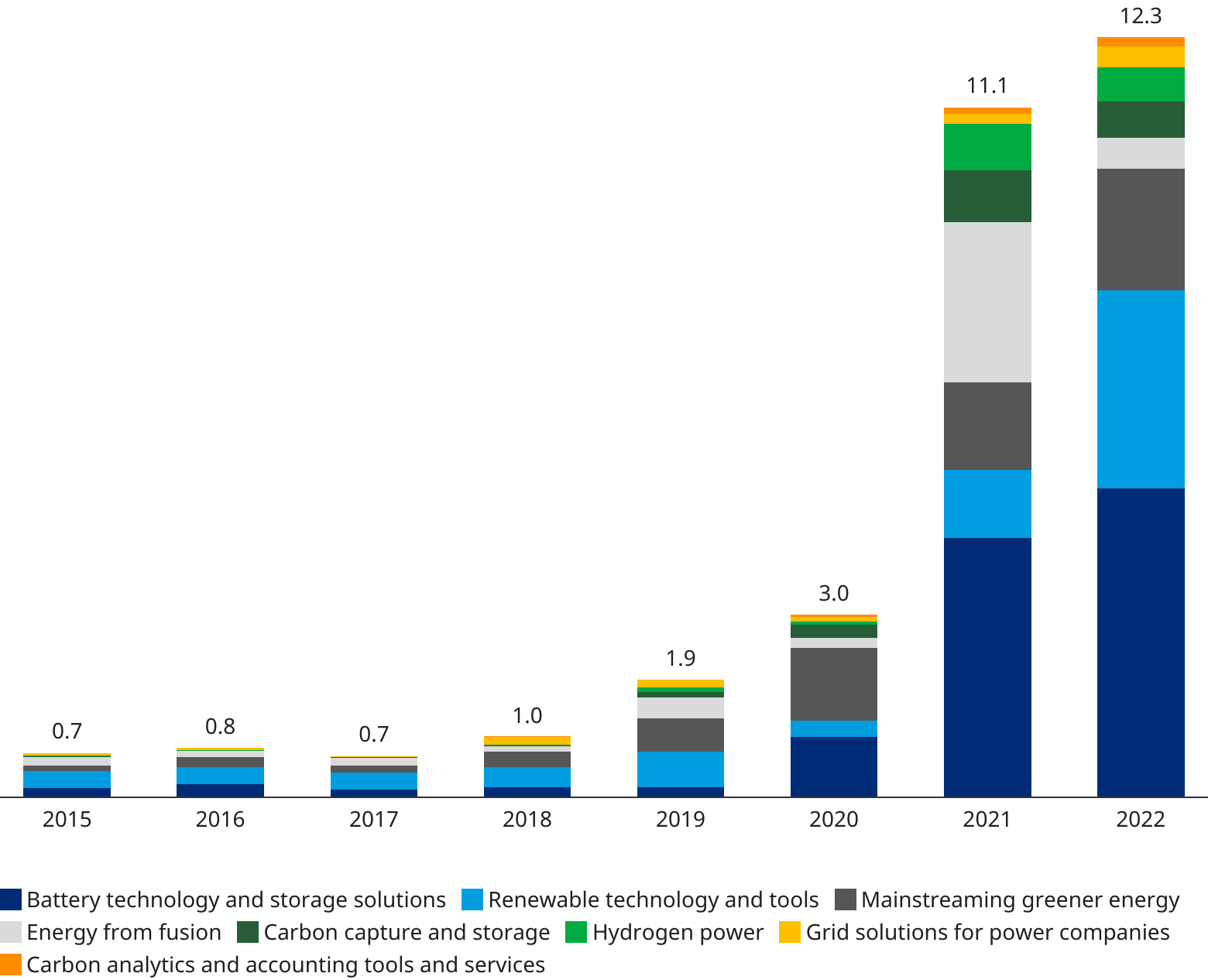

Battery technology, in particular, has received such large investments. When it comes to batteries, new technology is needed to enable large-scale decentralized storage and expand the availability of renewable energy on a less intermittent basis. In 2022, $5 billion was invested in battery ventures.

Two-thirds of global VC energy funding in 2022 was invested in batteries and renewables. For instance, investment in renewables technology tripled from $1 billion in 2021 to $3 billion in 2022.

Exhibit 3: Average funding amount per round

In US $ millions

Source: Crunchbase, Oliver Wyman analysis

The significant interest in fusion — which is still in the early research stage and not at all close to commercial scale — demonstrates that VC investors are also willing to play a long game in clean energy, which is good news for the planet

Christopher Sohn, principal, Energy and Natural Resources

Breakdown by category

Investment in hydrogen has been steadily gaining pace, but overall amounts are still lower than new technology and solutions surrounding more established technologies like batteries and renewables. Between 2019 and 2022, investment in the development of hydrogen production technology rose from around $70 million to approximately $550 million.

During the same three-year period, investment in carbon capture and storage rose from approximately $100 million to $600 million, which points toward increased confidence that this technology will play a key role in the energy transition. Carbon capture and storage is sometimes used in the production of hydrogen to take carbon out of hydrogen produced from natural gas or ammonia, moving it from gray hydrogen to blue.

One of the newest technologies attracting VC money is fusion. While it is less certain whether the technology will ultimately bear fruit, the rewards could be enormous if it does. Investment in fusion technology reached a high of $2.5 billion in 2021, driven largely by two mega deals. 2022 did not see mega investments in fusion startups, and as a result, the annual total for fusion dropped to $500 million.

Since 2020, investment in startups developing tools for emissions data collection, analytics, and accounting has been steadily rising — from less than $10 million in 2019 to approximately $150 million in 2022. This connects to the rising pressure globally on companies to report emissions. This is especially the case in Europe where the recently enacted Corporate Sustainability Reporting Directive (CSRD) will begin requiring companies to report their annual emissions, along with net zero targets and detailed transition plans to reach them.

Other clean energy startups attracting investment include ones working in innovative grid technology, which attracted almost $350 million in 2022, and solutions that would mainstream green energy approaches to increasing energy efficiency, helping with decarbonization efforts, and stemming the rise in energy costs for businesses and consumers.

Exhibit 4: Global venture capital investment in clean energy startups by category

In US $ billions

Source: Crunchbase, Oliver Wyman analysis

Solar and wind energy, while more mature technologies, still must overcome their intermittency problem through storage solutions. That’s one reason why more than two-thirds of global VC clean energy funding in 2022 went to battery, storage, and renewables

Leopold Zangemeister, engagement manager, Energy and Natural Resources

Leading the charge

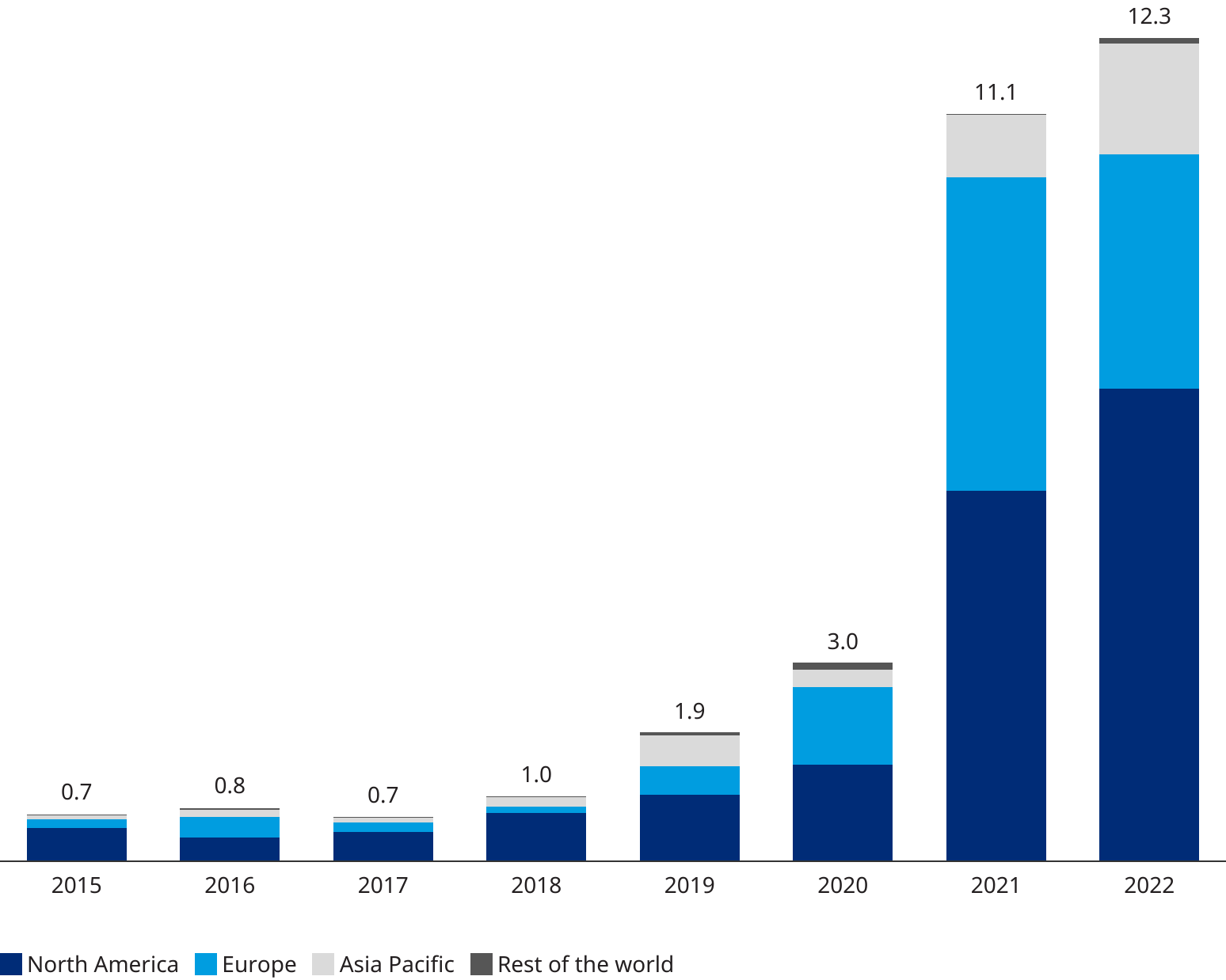

Investors in North America were the primary drivers in clean energy investment in 2022 — contributing $7 billion, or about 57%, of the annual total. That funding was up from $5.5 billion in 2021.

Europe was the other active region for clean energy investment, with a 2022 total of $3.5 billion. The two regions together accounted for 85% of total clean energy startup funding last year. Still, Europe’s contribution dropped in 2022 from $4.6 billion in 2021, the result probably of economic pressures from inflation and interest rate hikes.

Another development pushing green investment in the two regions has been recently passed laws. In the US, the Inflation Reduction Act provided incentives for investing in and adopting clean technologies. The EU also sweetened their subsidies with the Net Zero Industry Act, while bolstering reporting standards with the passage of the CSRD.

Between 2019 and 2021, VC investment in China rose from $300 million to $700 million. The more than twofold increase in funding was driven primarily by a handful of investments in companies working on batteries, renewables technology, and energy efficiency. In 2022, it increased again more than 71% to $1.2 billion because of a push to expand renewables. Beyond that, Japan and Australia also were active players in Asia Pacific bringing the region’s total to $1.7 billion — almost 14% of the total for last year.

Investment in the rest of the world amounted to around $100 million.

Exhibit 5: Global venture capital investment in clean energy startups by world region

In US $ billions

Source: Crunchbase, Oliver Wyman analysis

Was Europe a hiccup?

Despite the year-over-year decline in VC funding from Europe, there’s new urgency in the region for innovation in clean energy technology because of the disruption in energy markets caused by the Ukraine war. In an otherwise conservative investment climate, the continued European enthusiasm also demonstrates strong investor confidence in the potential size of opportunities in clean energy technology.

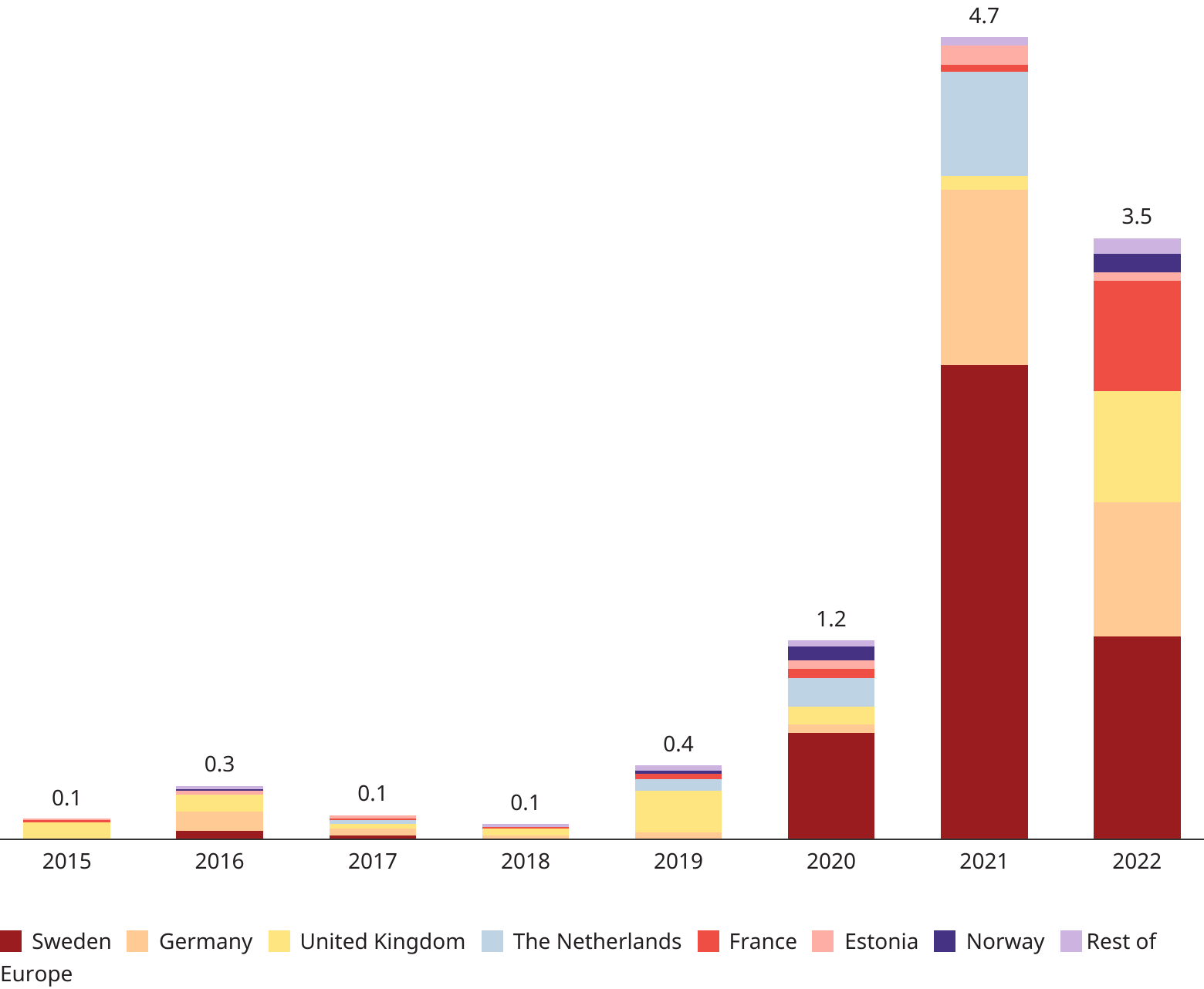

Within Europe, Sweden was the frontrunner between 2020 and 2022, beating out the usual leaders — the United Kingdom, France, and Germany. Together, these four markets consistently accounted for more than 75% of VC funding in Europe between 2019 and 2022 — reaching as high as 95% in 2021.

Across Europe, and especially in Germany, record funding for startups providing end-to-end solutions for consumer and business end users reflect the more intense focus on increasing energy efficiency and cutting onerous electric bills. The concentration on the cost of energy is the product of inflation fueled by the COVID-19 pandemic and Ukraine war. It has awakened investors to the opportunity fragmented and decentralized energy markets represent. Before the spike in prices, utilities and other incumbent providers had not fulfilled customer expectations regarding end-to-end service and solutions — an omission not sustainable in the current climate.

Exhibit 6: Venture capital investment in clean energy startups based in Europe

In US $ billions

Source: Oliver Wyman analysis

The opportunity for established energy players

On the road to net zero, energy companies face an unprecedented and unparalleled need to innovate, putting many business models that have worked for decades under pressure. The price for the energy transition is rising daily as central banks across Europe and North America continue to raise interest rates. That means much needed investments in innovative technologies may not materialize to the same extent in the foreseeable future — an untenable situation given rising climate pressures. To keep up with the push for decarbonization, established energy players should look to partner with young, innovative businesses like these startups. The four biggest reasons to partner are:

- The same level of innovation is difficult to generate in an established company setting.

- Established companies struggle with transforming existing corporate culture.

- Incumbents often struggle to attract younger R&D talent that’s often responsible for developing cutting-edge technology, especially in the digital realm.

- Partnerships with startups offer a lower-risk strategy for incumbent companies to expand quickly into new business models and diversify portfolios.

Startups also benefit from teaming up with deep-pocketed legacy players because of the large customer bases they offer. Incumbents also have the personnel and capacity to scale projects more quickly.

As the energy transition accelerates, big energy enterprises should look to differentiate themselves through innovative green business models that have the potential to unlock new value pools. It will be all about building sophisticated ecosystems that include either in-house startups or external partnerships with them.