A Future of Challenges and Hope

After five years of growth and profitability, the aviation industry is now entering a decade of uncertainty and, for at least the first two to three years, considerable financial pressures. As COVID-19 spread across the world, the industry lost over $118 billion in 2020, according to the International Air Transport Association, and saw dozens of airlines seek bankruptcy protection or stop flying entirely.

2021 is unlikely to be much different. Except for airlines in China, where domestic travel returned to pre-pandemic levels by November 2020, global carriers will still burn millions in cash daily for much of the year — but probably not all of it. Some will face the unsettling prospect of restructuring and consolidation. Losses in the tens of billions of dollars are expected again this year, although the industry will suffer less than half of the hit it sustained the first year of COVID-19.

That means cash preservation will remain a top priority for airlines, which is not good news for aerospace manufacturers and maintenance, repair, and overhaul (MRO) service providers. In 2020, COVID-related pressure on airline cash flow and reduced demand for air travel led global carriers to put thousands of aircraft into storage, retire twice as many as normal, convert some for carrying cargo, and cancel or defer some deliveries of new planes.

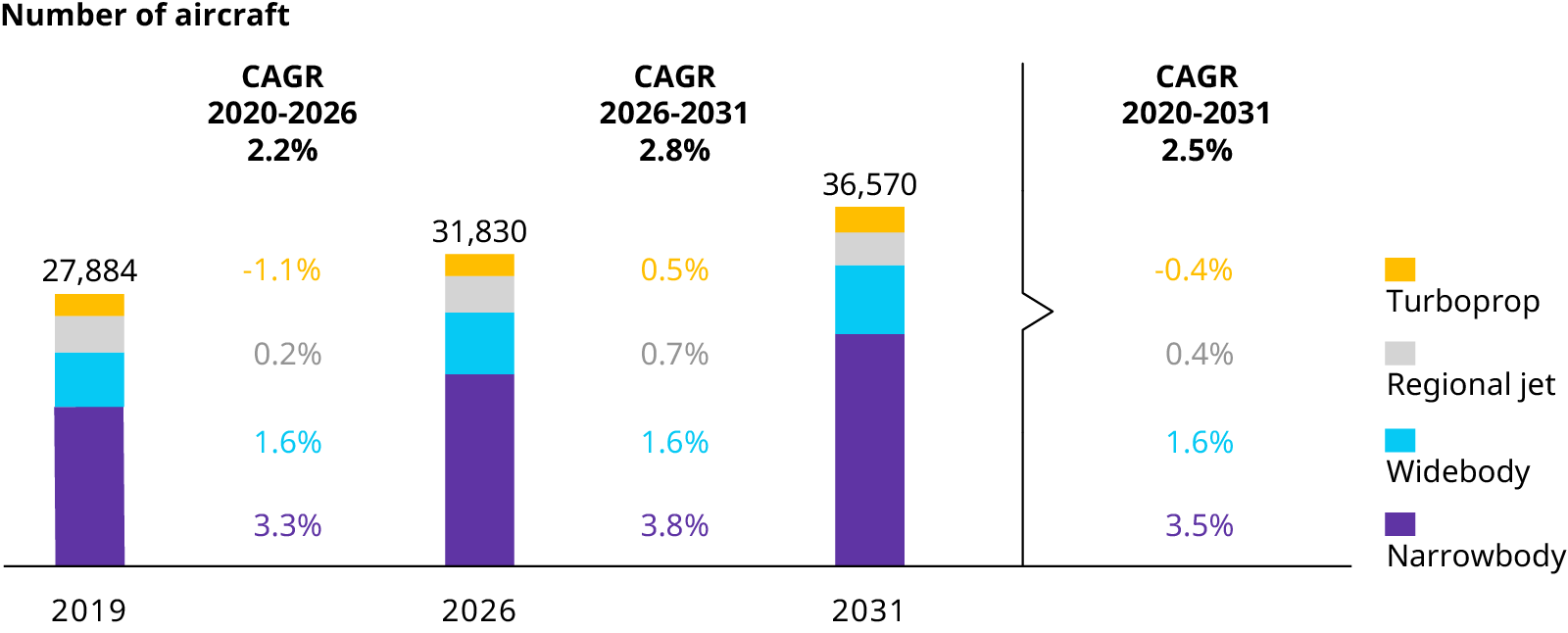

At its nadir, the global fleet had only about 13,000 aircraft in service, less than half the number flying in January 2020 before the pandemic was declared. Today, the 2021 fleet is up to more than 23,700 aircraft. By 2031, we forecast the fleet will number more than 36,500. But it’s still a far cry from pre-COVID projections, which put the 2021 global fleet at 28,800 and the 2030 fleet at more than 39,000.

Playing Catchup for 10 Years

That’s the outlook for aviation emerging from Oliver Wyman’s Global Fleet and MRO Forecast 2021‑2031. The 10-year forecast period starts slowly, with growth picking up steam in the second half of 2022, after the fleet finally recovers to its pre-COVID January 2020 level. Still, none of the three segments — airlines, aerospace, and MRO — are expected to catch up with pre-COVID projections by the end of the 10 years.

Given the inventory backlog of new planes that are built but undelivered or still not sold, more aircraft will be delivered to airlines over the next several years than will be produced by aerospace manufacturers. While production and deliveries are closely aligned in normal years, the imbalance reflects conflicting pressures on airframe manufacturers to balance the realities of lower market demand with needs of key suppliers to maintain sufficient production.

Other aerospace revenue also may be in jeopardy. The early retirement of planes may reduce aerospace sales of new parts because of increased competition from the surge in supply of used components and green-time engines harvested from retired aircraft. It will take as much as three years to work through the excess of used serviceable material.

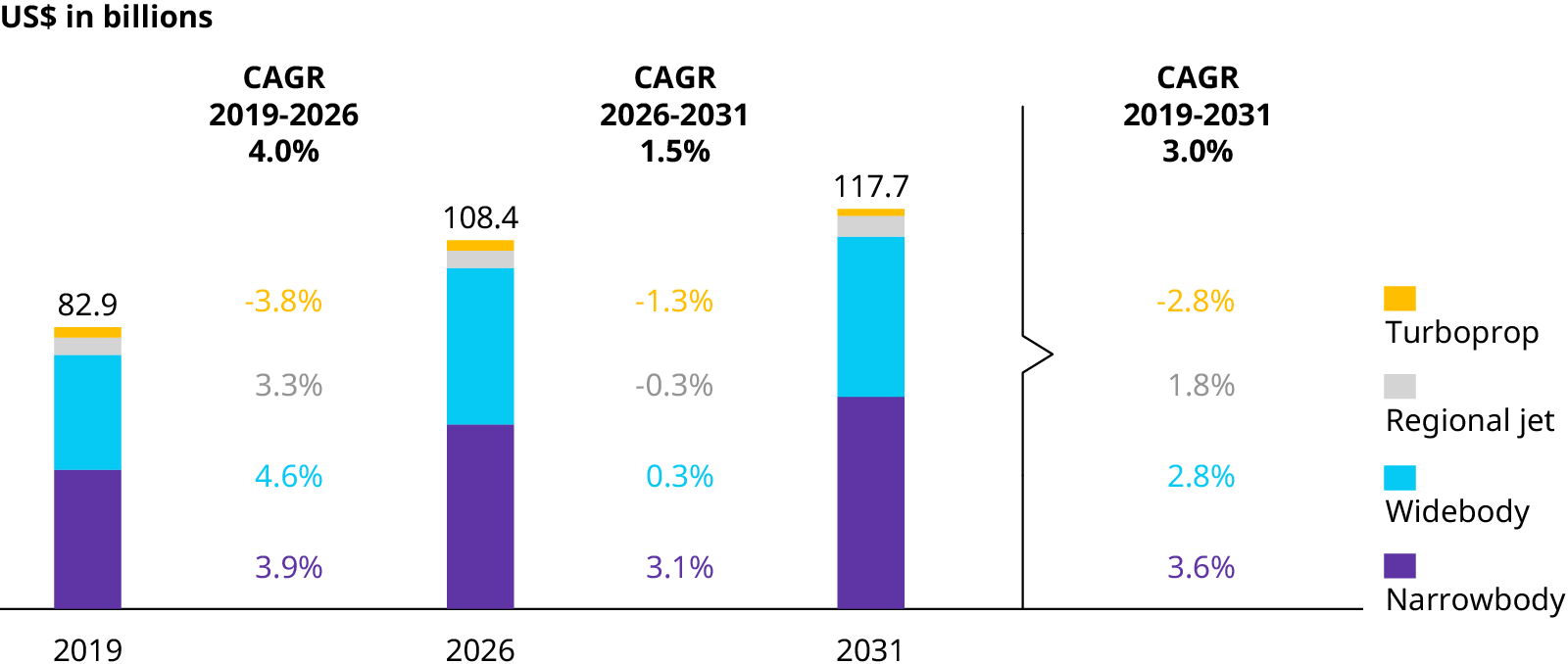

For MRO companies, a smaller fleet translates into less work. Demand is expected to be 33 percent, or $60 billion, below combined pre-COVID projections for 2020 and 2021. While the market is beginning to recover, the long-term MRO growth trend is now roughly half of pre‑COVID expectations. Cumulatively, MRO demand is expected to be $95 billion lower over the forecast period.

Opportunities for Growth

Despite the reduced expectations for MRO, the compound annual growth of the sector between 2019 and 2031 is projected at three percent. The combination of near-term lower demand and long-term growth prospects has created an attractive environment for private equity investors, and interest in MRO is high.

The popularity of narrowbody aircraft is also on the rise. For years, the narrowbody share of the total fleet has increased as the improving range capability and attractive seat mile efficiency of the class have made the aircraft the choice of low-cost carriers. This trend is expected to continue as more airlines align fleets to the demand realities of COVID-19.

While forecasts for narrowbody production are 40 percent below 2018 levels for 2021, we expect the aircraft class to recover to within 10 percent of our original pre-COVID projections for the final years of the forecast period. One bright spot has been sales of A321LR, which remain strong even in the face of the pandemic. The aircraft offers sufficient range to serve routes that were previously flown with Boeing 757s or widebody aircraft, as well as providing airlines increased flexibility in their scheduling.

Deliveries of narrowbodies in 2021 will also be bolstered by decisions by the Federal Aviation Administration and European Union Aviation Safety Agency to recertify the Boeing 737 MAX for commercial service. More than 20 737s have already made it back into carrier fleets since the recertification, but there are 400 to 450 more MAX aircraft, built in 2020, that are sitting in Boeing’s inventory undelivered or not sold. In addition, the number of narrowbodies in the fleet will be expanded by the almost 400 737s that airlines have had in storage since the plane’s grounding in March 2019.

The Impact of Less Business and International Travel

In contrast, widebody aircraft production has seen a significant decline because of COVID-19’s impact on long-haul travel demand. Over the forecast period, we expect widebody production to be as much as 40 percent below pre-COVID expectations unless there’s a faster-than-expected recovery in long-haul routes.

COVID has created a long list of challenges never seen before in modern commercial aviation. It will take the next few years to adjust the fleet to the new realities and return to stable growth. Even after 10 years, the industry will not have fully regained all that it has lost with the pandemic.

COVID has created a long list of challenges never seen before in modern commercial aviation. It will take the next few years to adjust the fleet to the new realities and return to stable growth. Even after 10 years, the industry will not have fully regained all that it has lost with the pandemic.

International travel — which accounts for the bulk of long-haul — evaporated in the early days of COVID-19 and continues to be hard-hit, which has had implications for widebodies. Over the last year, nations around the world have been tightly regulating cross-border travel in an effort to keep out or at least contain the pandemic. Border closings and sudden requirements to quarantine for 14 days have discouraged travel between countries, with passengers fearful of being stranded or unable to get home. Under a new executive order from President Joe Biden, travelers entering the United States must provide proof of a recent negative COVID-19 test prior to entry — a requirement that already exists in some other countries.

Contributing to the decline in international long-haul travel has been the fall in business travel, the most profitable category for airlines. This is especially true on long-haul flights, on which executives often opt for premium seating.

Videoconferencing and teleconferencing have become attractive substitutes that allow companies to cut travel budgets, particularly for intracompany trips. COVID-19 has also forced many business conferences and trade shows to go virtual or be canceled entirely, eliminating another reason for executive travel. While most of this travel will eventually return as more people get COVID-19 vaccinations, it is unlikely to recover fully over the midterm.

Regional Jets

Meanwhile, the regional jet class is facing multiyear delays for some of its latest models as new platforms encounter development problems and as clauses in US pilot contracts limit their use. Given that many regional jets will reach typical retirement age or cumulative utilization during the forecast period, we expect many to end up flying beyond historical thresholds to cover some of the demand for smaller commercial aircraft.

It’s no exaggeration to say that modern commercial aviation has never faced such a long list of challenges as COVID-19 has created. It will likely take several years to adjust the fleet to new realities, and even then, the industry will not regain over the next 10 years all that it has lost with the pandemic.

Fleet & MRO Forecast COVID-19 Impact Dashboard

About the Forecast

The 2021-2031 edition of our Global Fleet & MRO Market Forecast Commentary represents a more than two-decade commitment to the understanding and assessment of the commercial airline transport fleet and the associated maintenance, repair, and overhaul (MRO) market outlook. The commentary is the go to resource of aviation executives—whether a manufacturer, operator, or aftermarket provider, as well as for those with financial interests in the sector through private equity firms and investment banks.

This year's research focuses on the aviation industry’s recovery from COVID-19, subsequent growth and related trends affecting aftermarket demand, maintenance costs, technology, and labor supply after a devastating 2020. The outlook reveals significant challenges the industry faces as it develops and expands its recovery and rebound plans.

An interactive tool also accompanies the report for further exploration of the forecast.

Analytical topics in the commentary include:

- In-service fleet, retirements, orders, conversions by aircraft class (widebody, narrowbody, regional jet, and turboprop)

- Global aircraft fleet forecast and regional fleet growth rates including in-service fleet by age

- MRO market forecast by segment (line, component, engine, airframe) and aircraft platform spend

- Economic GDP and traffic data (measured in revenue passenger kilometers or RPKs) by geographic region and specific countries along with utilization cycles

- COVID-19 impact on passenger and cargo traffic, anticipated recovery, and changing trends

- Forecast sensitivity analysis based on epidemiological timeline and public health response to COVID-19, traveler sentiment, government restrictions, and macroeconomic recovery

This article was authored with contributions from Faith Lee, Engagement Manager at Oliver Wyman.