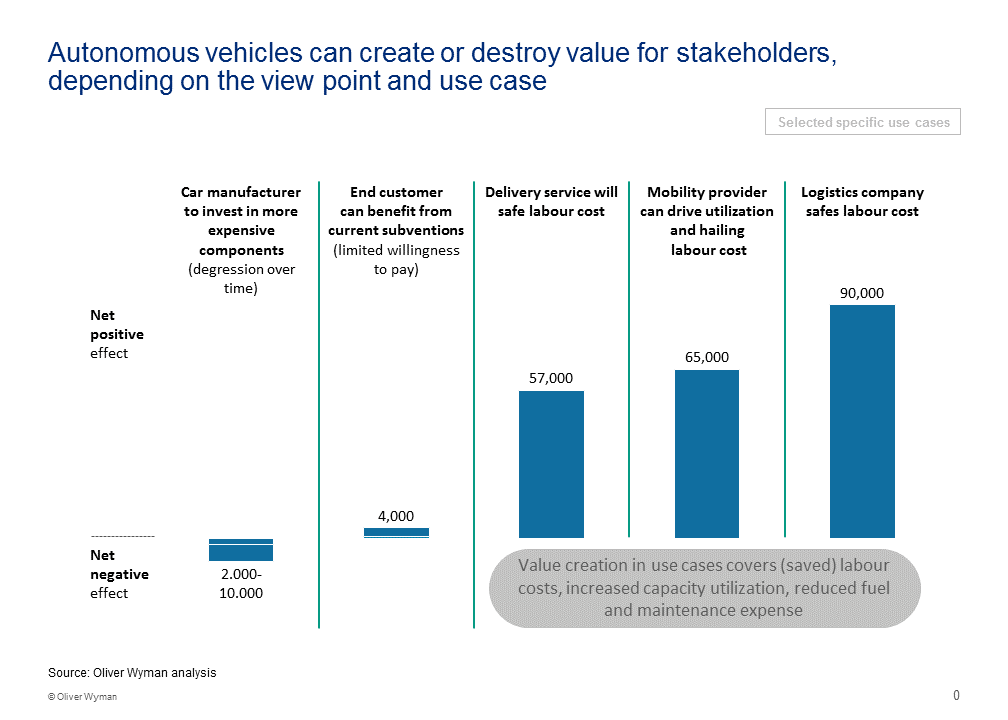

For a mobility provider or logistics company, autonomous driving could knock out the cost of human drivers – some 65,000 to 90,000 euros a year each in Western Europe. This could yield substantial profitability gains within service businesses that have limited options for diversification.

For a manufacturer of private cars, there’s no such upside. However, fitting the systems will be costly: around 8,000 to 10,000 euros at present. And it will be impossible to pass this price increase on to customers, resulting in a substantial net negative for business. Moreover, any accidents are more likely to be blamed on the manufacturer rather than the driver, so automakers could face an added risk to their reputations.

Autonomous vehicles are the future, however. Automakers should therefore broaden their outlook, anticipating shifts in consumer spending so that they can provide what is demanded. Robot-guided cars could turn up at someone’s door when needed, so consumers might spend their money on mobility rather than on vehicles. In addition, car use will increasingly be combined with other modes of transport, such as trains and bicycles, which will also shift spending away from automakers’ core business.

To participate in this widening mobility market, car manufacturers need to build up diverse networks of partnerships. These should include software specialists that can improve cars’ autonomous capabilities, suppliers of cloud-based digital infrastructure, and providers of new mobility services such as car-sharing and driverless taxis. The new services will make it all the more important to optimize the utilization of transport networks – and by participating, automakers will continue to benefit as mobility evolves.

To participate in this widening mobility market, car manufacturers need to build up diverse networks of partnerships

These partnerships will distribute risk and reduce costs, while letting an automaker remain flexible so that it can respond to changes in mobility needs. Boundaries with direct competitors should fall – especially in traditional hardware, where currently only half the innovations lead to a differentiation in brand perception, a proportion that is expected to shrink even further. In the future software will represent an increasing share of a car’s value, but also here brand differentiation exists only in limited cases directly at the customer interface. Car manufacturers must act wisely and fast – and be prepared to do so continuously.