Insurance is not known for being at the forefront of innovation. By and large, customers are buying the same types of covers from the same carriers in the same way as they were 20 years ago. Of course there are some exceptions to this rule, and solution innovators are mostly still playing at the edges of the industry. And even with the introduction of vast and readily-accessible computing power, most insurers have largely just digitised their existing processes rather than fundamentally reinvent the way they deliver the peace of mind for customers’ critical protective moments and assets.

Contrast this to the way that technology has changed the way in which we navigate a journey and we can see how stark the gap is between the real customer value innovators and their disruptive solutions and our industry.

Today it is possible to programme a vehicle with your final destination, and not only have it take you there without any human at the wheel, but also to dynamically adjust its course in real time to deal with any unexpected challenges. This was unthinkable 10 years ago. And yet the equivalent in insurance, to provide protection and savings which adapt automatically to our clients’ changing needs and circumstances, seems just as far away today as it was before the first electronic map.

Of course it is easy to overstate the relevance of such examples to the insurance industry. Insurance is heavily intermediated, which means that we don’t fully control the customer proposition or experience. It has historically relied on long-term contracts with defined terms & conditions, so our ability to pivot fast is constrained by large legacy back books. And we have relatively few touch points with our customers to gather and process new information.

Yet surely there are lessons we can learn from the big innovators which have made so much of a difference to so many other parts of our lives

In our 2018 State of the Financial Services report, we discuss exactly that dilemma. Our discussions with financial services executives have uncovered a gnawing sense of concern: that the structural advantages of their businesses are eroding; that it is unclear where growth is coming from; that new customer value is being generated in other industries now more and faster than in financial services; and that big techs are growing extremely quickly and will be entering the industry in force in the coming years.

These concerns are well-founded. Recent growth has not only lagged historical norms, it is also well behind that for the big tech firms. At the same time, many of the historical foundations that once supported growth and profitability have deteriorated – risk pools are shrinking towards “segments of one”, information asymmetries are flipping back in favour of customers, and the bedrock of investment yield has eroded in many mature markets. The good news, however, is that there is still time to do something – but not for long!

In our view the first step that an incumbent looking not only to preserve its current place but to find new sources of growth is to take innovation seriously. And the best place to look for lessons to be learned is the big tech companies themselves. We see three common ingredients:

1. They focus on solving a big customer problem and establish a beachhead solution to that problem. Too often we see innovation programmes and units which are in reality extensions of business-as-usual development, and end up focusing on innovating against existing operations or existing products and propositions. The most successful innovators have put their energies into creating net-new growth out of areas of as-yet-unresolved customer struggle

2. They create active solutions, treating product components and customer experience as an integrated whole, moving in lockstep with customers’ evolving needs

3. They generate flywheel momentum to sustain growth, relentlessly improving their solutions with data and analytics. Rather than taking a once-and-done approach to proposition development, they realise that the more they improve the experience, the more traffic they drive to their solutions, the more underlying products get activated, which in turn enriches the data and insights they are able to generate – and as a consequence, allows them to attract top talent across ‘STEAM’ disciplines (science, technology, engineering, art and maths)

Our report illustrates these ingredients in action by asking the question:

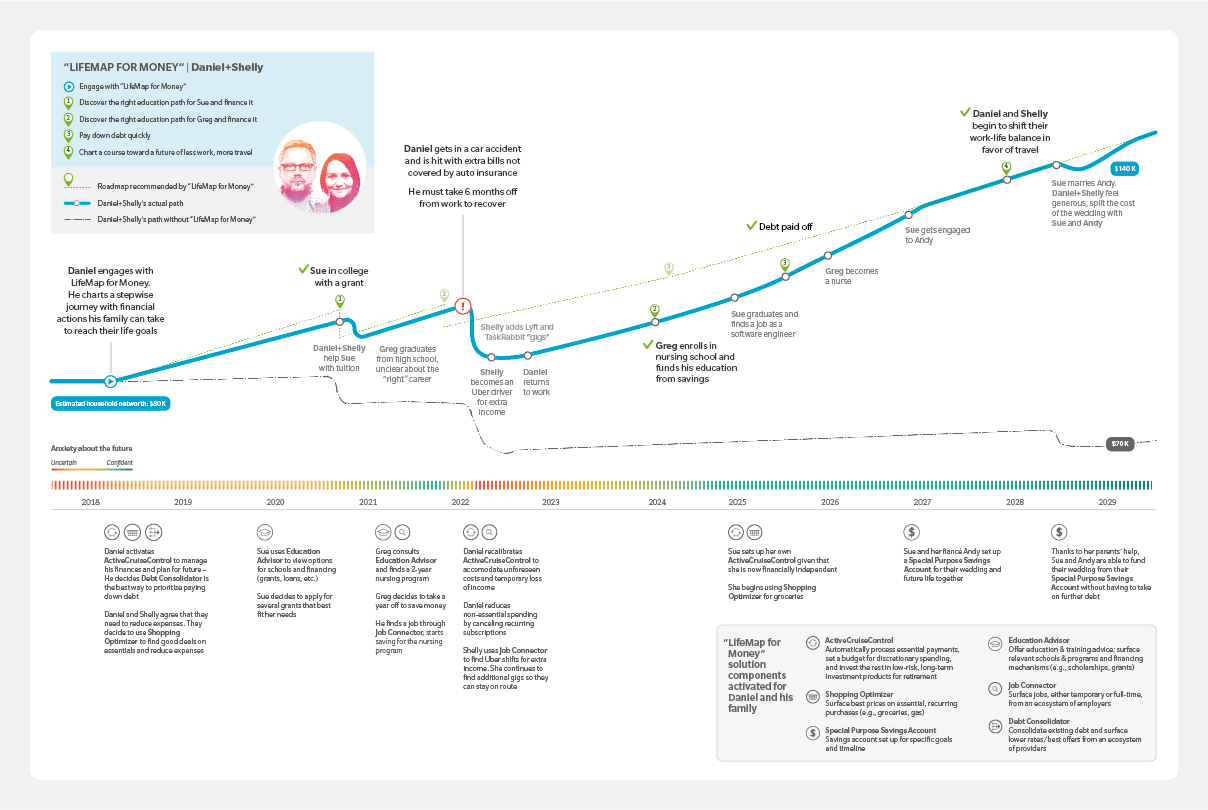

What would Google Maps look like for financial services?

It presents the concept of the LifeMap for Money, a real-time adaptive financial management tool that engages with a customer’s financial destinations, plots the optimal path to get there (plus some alternatives) but is continuously updated for unexpected snags along the way.

Many insurers will recognise the concept as something they have been working towards for many years, but have yet to realise. Many will also recognise the analogue Financial Advice parallel – the human in the passenger seat with the map book, unsure of whether the maps are still up to date, with infrequent traffic reports on the radio, little idea of where the next refuelling stop is or what time we’d expect to reach our destination. Those experiences feel like ancient history when driving, yet are still the norm for many financial services customers.

It is all too easy to set out the problem statement here, but much harder to land on a set of actions that will lead to the kind of solution that transforms – or creates - an industry. Our report finishes with six concrete plays that we believe all insurers looking to drive transformative change should adopt:

Play 1: Face the gnawing concern head on

Play 2: Rethink how you assess customer value

Play 3: Design active solutions

Play 4: Build your ecosystem strategy around active solutions

Play 5: Get on the Growth Flywheel through careful portfolio analysis

Play 6: Get on the Growth Flywheel through organisational design