Welcome to the second edition of our EMEA banking newsletter. In this short publication, we look to summarise the themes that we believe are top of the agenda for senior management.

With trends in profitability during the first half of 2017 being mostly favourable, banks across Europe, the Middle East and Africa (EMEA) are increasingly focused on finding new sources of revenue and responding to long term business model disruptions.

In the third quarter of 2017, Oliver Wyman will publish a European banking report on the long-term success factors for banks. Meanwhile, in this Spotlight, we discuss three of the main challenges raised in our conversations with senior banking clients, and the best-practice responses that are emerging.

First, recent cyber-attacks have increased banks’ focus on data privacy and cyber security, and have highlighted how banks are struggling to balance these demands with the need to establish business models that can profit from the new world of data portability. Leading banks are using the new regulations in this sphere as an opportunity to undertake a fundamental review of their data strategy and IT in a bid to build long-term value.

Banks should be experimenting with different techniques to develop agile solutions

Second, a year after the UK’s referendum on European Union membership, banks are still working through the details of what their long-term EU footprint and business model will look like post-Brexit. Most organisations are planning for a worst-case outcome which will see them reduce their presence in London and increase their footprint in the remaining EU27 countries. Inefficiencies resulting from greater fragmentation will force many to examine the economics of their business very carefully.

These are significant tests. Planning a successful response brings about the third challenge: a need for a greater agility in decision making and design than most banks are currently able to deploy. Banks should be experimenting with different techniques to develop agile solutions. We conclude with an example of one such approach.

Data Portability, Privacy, Security

Technology and regulation are increasing the volume of data generated on individuals, the expectations for ease of transfer of this data, and the requirements for protection and security of this data. The General Data Protection Regulation (GDPR) in particular will transform EU banks’ obligations by granting individuals the right to transfer or erase all of their data.

Banks should be fundamentally reviewing their data strategy and IT architecture to meet these new expectations. In our paper, “Future Proofing Privacy”, we outline four components of sustainable solutions that provide data privacy and portability:

Data discovery or mapping tools that conduct an automatic review of systems to identify personally identifiable information (PII)

A single register for metadata that acts as a chain of custody for each element

Sharing of the register across all products or even external providers

A subject access portal through which to provide, amend, and retract consent

Figure 1: Finding a sustainable GDPR solution

Given the growing sophistication of cyberattacks, such solutions should include strong cyber security governance and procedures. In our paper “Deploying a Cyber Risk Strategy”, we set out five requirements:

Quantification of cyber risk in terms of capital and earnings at risk

Anchoring of all cyber risk governance through risk appetite

Independent cyber risk oversight using specialized skills

Comprehensive mapping and trialling of controls, especially for third-party interactions

Development and testing of major incident management playbooks

Banks that succeed in implementing new data and infrastructure strategies stand to benefit beyond the confines of regulatory compliance and risk management. First, they will build customer trust and loyalty by giving back control of data. Second, they can drive IT costs down by minimising the amount of data collected and stored. Third, they will help build a more open, modular business model that can thrive in the new digital economy.

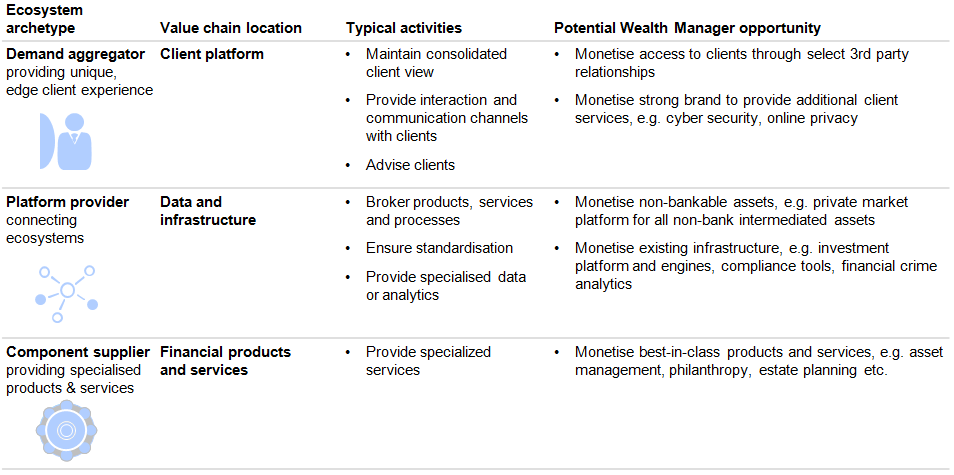

Spotlight on Wealth Management

In our recent wealth management report in association with Deutsche Bank, “Time to Advance and Defend”, we highlight how increasing levels of data availability and transparency will put pressure on wealth management profitability, while suggesting how banks can use this change to control costs and find new sources of earnings.

We expect that middle and back office digitisation will represent the most important cost lever. Revenue efforts will need to include both doubling down on existing initiatives, for example increasing alternatives presentation, and finding new non-traditional sources, as described in Figure 2.

EU Business Models Post-Brexit

Political developments and an increase in uncertainty since the recent UK election have led banks to converge around a base case for Brexit which leaves the UK with limited privileged access to the EU, no immediate regulatory equivalence (such as through the Markets in Financial Instruments Directive), and no transition agreement. Banks will have to serve EU clients and interact with the EU financial market infrastructure from an EU entity, which will require a substantial strengthening of existing capabilities and, for many, the licensing of one or more new entities.

Most banks are therefore planning to reduce their capacity in the UK and shift some of their business into the EU 27. Frankfurt, Paris, Dublin and Amsterdam are emerging as the main beneficiaries, but final decisions on the scale of the move, and eventual locations, are still to be made. Banks are conducting their deliberations on the basis of a range of criteria, namely their existing footprint, their clients’ locations, the relative costs and tax levels, and the respective regulatory environments.

Banks are conducting their deliberations on the basis of a range of criteria, namely their existing footprint, their clients’ locations, the relative costs and tax levels, and the respective regulatory environments

Moves to the EU will result in both operational cost and financial resource inefficiencies:

- Financial resource: The combination of stress tests, solvent wind down plans, and asset quality reviews is likely to lead to an increase in requirements for capital, funding and liquidity. Such a development will be exacerbated if firms lose internal model approvals, or if assumptions with regard to back-to-back booking models are rejected.

- Cost: Operating costs could also increase as banks build up European risk management, compliance, and control functions, as well as central teams to interface with regulators and run activities relating to the Supervisory Review and Evaluation Process. Unlike in the front office, there will be significant duplication across the two regions in these central teams.

These inefficiencies are set against a background of returns in Europe which, for many banks, are below hurdle. Corporate and investment bank businesses in Europe delivered returns on equity (RoE) of approximately 8% in 2016, compared to more than 10% in other regions.

Design Thinking Techniques for Agile Decisions

Meeting these strategic and infrastructure challenges will require well-executed three-to-seven-year strategies involving many teams across the bank. Typically, banks are simply not agile and flexible enough to deploy these strategies swiftly.

In particular, the interaction between front and back office is often far too transactional, with the front office taking decisions and then leaving the Operations and IT functions to execute, often with delays.

One valuable technique to help spur agility at large institutions is the process that we describe in our joint report with IESE Business School, “Design Thinking: The New DNA Of The Financial Sector”. Design thinking typically consists of five steps:

Empathise: Understand customer needs through data, intuition, and experimentation

Define: Define the problem and start setting goals and objectives

Ideate: Generate ideas for innovative solutions

Prototype: Start producing cost-effective and simple prototypes to generate feedback

Test: Understand what the customer thinks about the product, and why

This process should involve workshops with key stakeholders in the front office, IT, operations, and other relevant divisions. Workshop facilitators should try to avoid coming into the process with an outside-in view of what the right answer should be, but instead seek the right answer as it emerges through the process.

Preserving agility in a large institution is a great challenge. While we do not believe that any bank has found the ideal solution, our experience shows that this type of approach does move companies in the right direction.