It outlines what we expect for the industry in the coming years across a range of areas, including:

• Changes to the competitive landscape

• The role of shadow banking

• The relationship between banks and governments

• The returns delivered to shareholders

• The agenda for senior industry executives

"The Shape of Things to Come" demonstrates that European banking has proved surprisingly resilient in recent years, though returns have declined dramatically and the sovereign influence has become increasingly dominant in both performance and valuation. As a consequence of our diagnosis, we believe that institutions will need to address three important challenges in 2014: the growth agenda and strategy, managing deleverage and decoupling from the sovereign, and simultaneous improvement of cost efficiency and customer service.

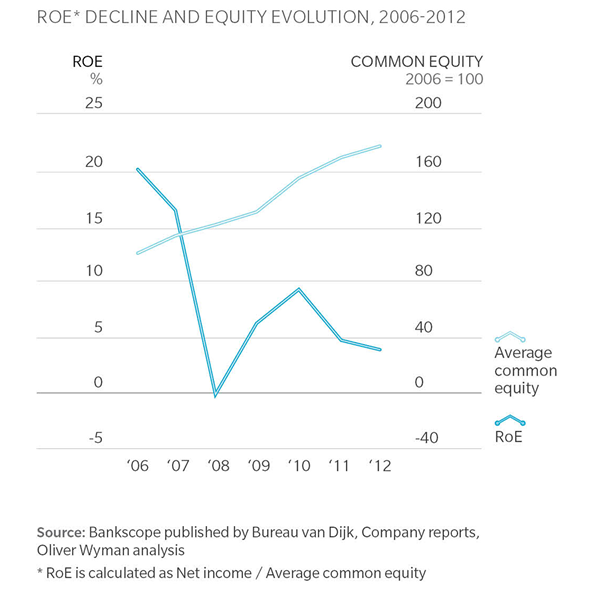

Increased capital to meet regulatory demands has further depressed returns

Returns for European banks have collapsed, from highs of ~20% in 2006 to ~4% in 2012. This is because of large provisions for non-performing loans (NPLs), a flood of other extraordinary charges (restructuring and conduct-related fines), significantly increased equity-to-asset ratios and insufficient reduction of operating costs. The rise in regulatory and compliance costs has swamped cost reductions.