By Wai-Chan Chan and James Yang

This article first appeared in HBR China on July 5, 2018.

Brick-and-mortar retailers worldwide have been hit by e-commerce, but the impact in China appears to be bigger and faster. Though just 11 percent of China’s population had Internet access in 2006, more than 460 million Chinese regularly shop online now, a third of the population. Even more significant is the willingness of the Chinese to go online to buy food – the largest retail segment. Encouraged by densely populated cities that favor rapid, efficient home delivery, nearly 10 percent of the Chinese population already shops for groceries online, compared to just 3 percent in the United States and 6 percent in the United Kingdom, one of Europe’s highest rates. However, there is still significant room for expansion: Already, an estimated 5 percent of Chinese shoppers buy groceries exclusively online, indicating the potential for more people to abandon physical stores.

Now, new shopping formats – dubbed O2O, or online-to-offline – are being rolled out. These combine online shopping’s convenience and wealth of information with the social experience and physical contact with products that people enjoy in traditional, brick-and-mortar stores.

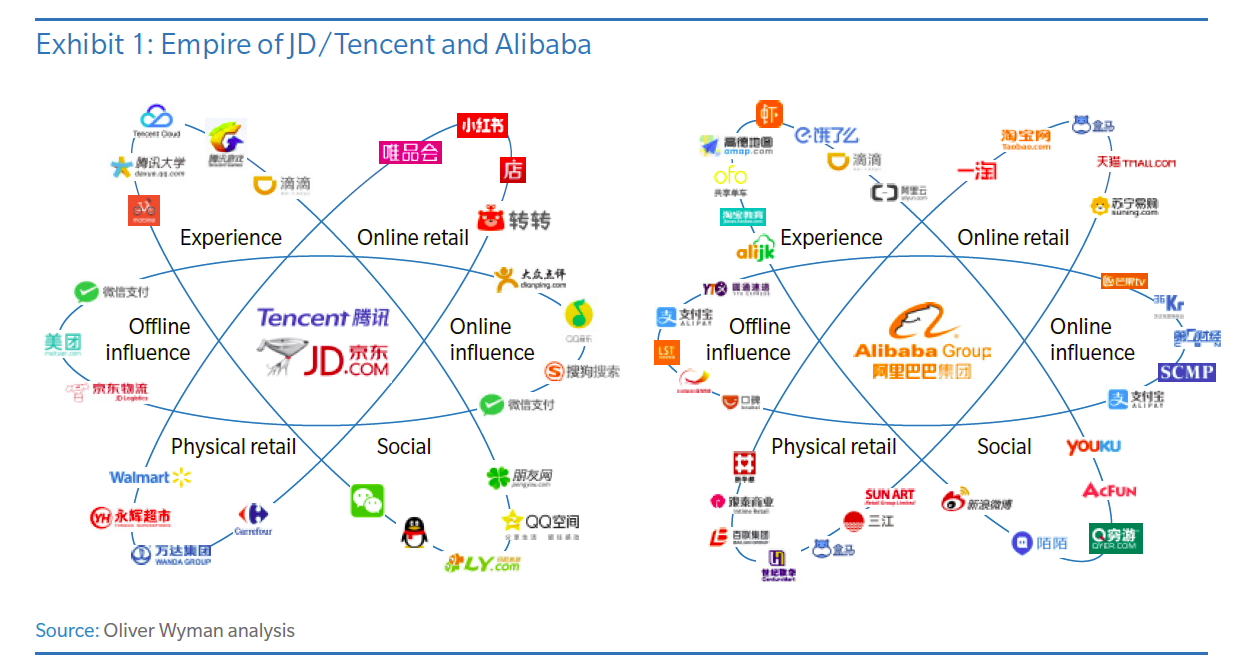

The innovations are not occurring in a haphazard way; they are being orchestrated by two emerging retail empires led by e-commerce giants. One is centered on Alibaba, which owns two of China’s largest e-commerce platforms, Taobao and Tmall, as well as an electronic payments system, AliPay. Its rival is an alliance between JD.com, a leading online retailer, and Tencent, an Internet and digital-technology conglomerate that owns WeChat, China’s largest social app. Together, they process 97 percent of mobile payments, providing them with valuable data on customer spending habits. Recently Alibaba and Tencent/JD.com set their sights on physical retail. They have acquired stakes in six of China’s top 10 hypermarkets, the country’s biggest electronics retailer, one of the largest department stores, and the largest commercial property and entertainment conglomerate.

In contrast to this ambitious expansion, traditional grocers are struggling. Their sales have declined in real terms over the last three years, while the total number of stores is lower than five years ago – in spite of GDP growth staying above 6 percent. The best survival plan for these stores: Ally with the very e-commerce giants that are invading their space. Both Alibaba and JD.com have developed logistics systems based on centralized, large-scale networks of warehouses, which can replace traditional distribution. Their payments and marketing systems can easily be scaled to large networks of physical stores. They can therefore help traditional retailers attract new customers and become more efficient.

Big-box Retail Experiments With E-commerce

Independent stores are finding the new environment hard, because they typically operate under franchise models in which store operations and products are not coordinated effectively. Survival will need drastic change, but we believe this is unlikely under their current set-ups. Most already operate with thin or negative margins and may not have sufficient funds to invest.

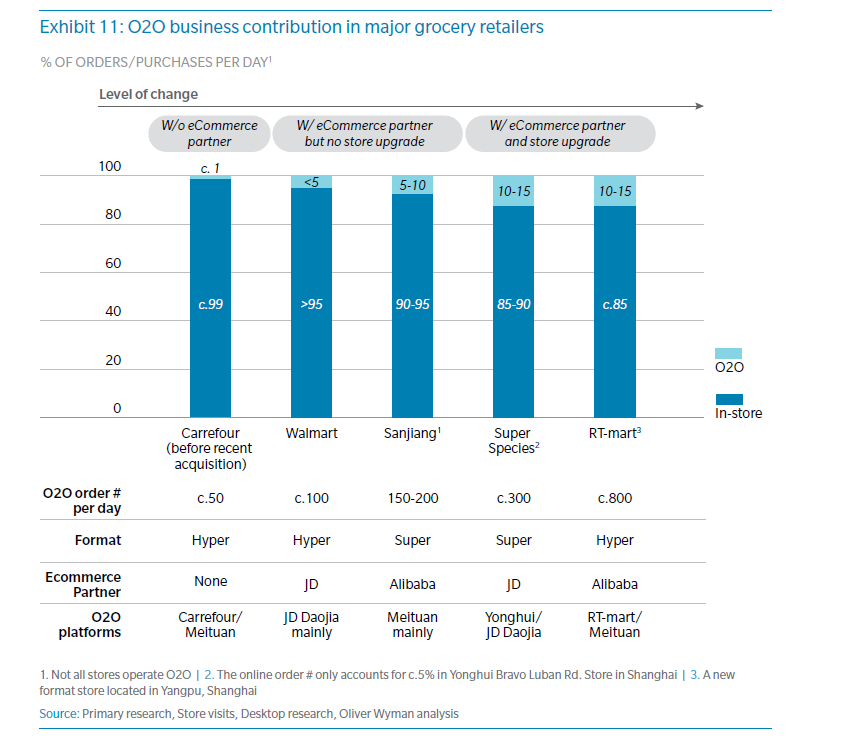

Big-box retailers have tried their own O2O and online shopping services. Hypermarket chain RT-mart launched its own B2C online platform Feiniu.com in 2014, while Carrefour China tried a similar system a year later in Shanghai. But these and other initiatives failed. One reason is that traditional brick-and-mortar stores do not have adequate distribution capabilities: Fresh food typically requires 30-minute delivery, which is only possible with a logistics operation that is complex, sophisticated, and large-scale. But big-box retailers have tended to invest more in marketing and promotion and focused less on logistics. Their store layouts are intended to guide shoppers towards products rather than to make it easy to pick items for delivery.

Moreover, picking for home delivery requires additional storage space, usually more than that in typical supermarkets. Although big-box retailers are starting to build their own logistics systems, their capabilities are still far behind those of online natives such as Alibaba and JD.com. Another reason for the big boxes’ difficulties is that they typically only generate O2O traffic from their own platforms, while Internet and e-commerce companies bring in customers through multiple contacts in their daily lives, including payment services, social media, and online purchases.

In contrast, partnerships with the tech empires benefit from complementary strengths, as technology from the online retailers helps the brick-and-mortar stores generate incremental revenue. For example, Alibaba installed shelves from its Tmall Supermarket online grocery service in some RT-Mart branches. The shelves direct Tmall’s best-selling products to RT-Mart stores in categories such as snacks, household essentials, and beauty products. From early 2018, RT-Mart has been offering one-hour delivery for these products to locations within 3 km of the stores in six cities. Alibaba has also contributed features such as mother-and-baby areas.

Next, Alibaba plans to help RT-Mart optimize its in-store O2O infrastructure. All the more-than 300 RT-Mart stores will be integrated into Taoxianda, the Taobao mobile app’s fresh delivery section. This will direct some users to RT-Marts, while customers will be able to order fresh products from RT-Mart through Taoxianda. RT-Mart operations will use Alibaba’s database of historical consumer purchasing data, so that stores can match their product lineups to consumer tastes.

Walmart has a strategic partnership with JD.com and is using its O2O unit JD Daojia as the service platform for more than 150 Walmart stores in order to attract online traffic. JD.com’s strong delivery capabilities will offer one-hour delivery. Planned upgrades to better support O2O services include picking areas in warehouses and a larger space devoted to fresh food. Wi-Fi will be available, so customers can self-checkout via a feature in the WeChat app.

In Shenzhen, Walmart has opened the first of a new chain of “smart” supermarkets, Huixuan, with an app-based shopping system in which customers scan and pay for items with their phones. The new stores will be relatively small – approximately 1,000 square meters – but have space for ready-to-eat food. Delivery is being handled by JD Daojia and is available in less than 30 minutes within 2 km of the first store.

Other recent strategic alliances include the January 2018 agreement by Tencent and Yonghui Superstores to take stakes in Carrefour China, as part of a plan for smart retail, mobile payments, and data analysis.

Mom-And-Pop Stores Reinvented

Smaller stores, too, can benefit from the e-commerce giants’ systems and transform from old-fashioned corner shops into slick, digital convenience stores. China’s more-than 7 million family-run stores are a major part of retail outside big cities and account for half the country’s sales of fast-moving consumer goods. Since early 2017, JD.com and Alibaba have been converting some of them into franchises. The stores are rebranded under the Tmall or JD.com umbrella and offer new services such as bill-paying. In addition, each can tailor its offerings to its clientele thanks to data-based curation advice. Stores can stock plenty of infant milk in a neighborhood with lots of babies and pet supplies if many residents keep dogs or cats.

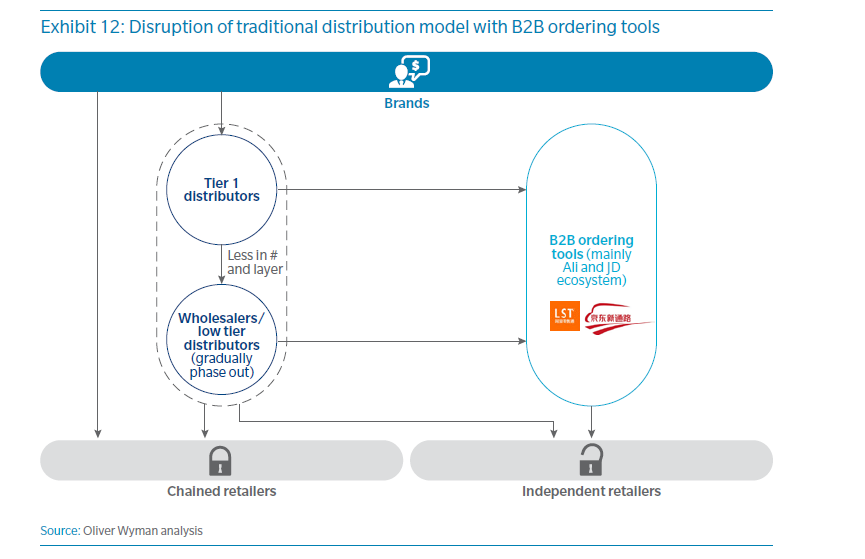

The procurement process, too, can improve dramatically. Small stores have traditionally been served by a network of multi-layered distributors and wholesalers. These capture a portion of the margins between producers’ prices and the money spent by consumers, and they often have troublesome requirements such as minimum purchase quantities.

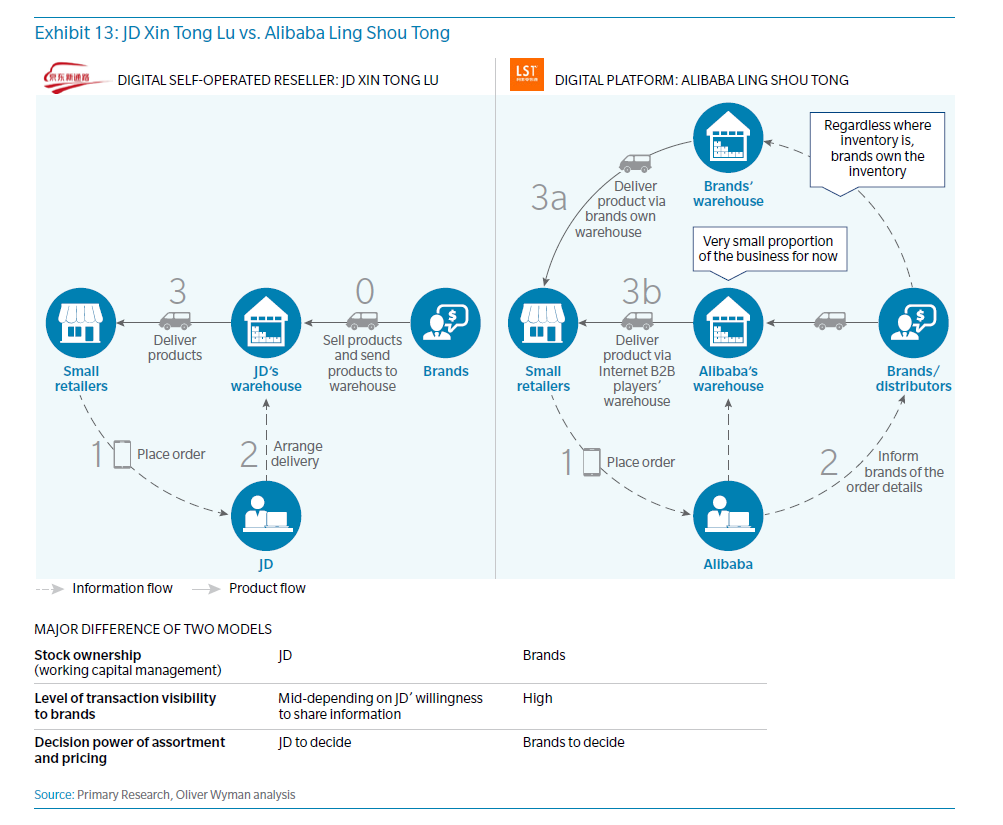

So, the two e-commerce giants have developed ordering systems that store owners can operate on their smartphones: Alibaba’s Ling Shou Tong (LST) and JD.com’s Xin Tong Lu (XTL). Goods arrive from centralized warehouses in less than three days and often on the day the order is placed. That contrasts with delays of weeks for traditional wholesalers. Alibaba and JD.com will capture new customer data and insights through these expansions. They are also likely to dominate the growing market for ordering systems, which could be worth around 400 billion yuan over the next five years.

Weijun Supermarket is a family-owned store in Hangzhou that in 2017 because the first franchise in a planned chain of Tmall corner shops. The store had been run down, and products were not presented in a way that made them easy to find. After renovation, the format is now similar to that of chain convenience stores such as FamilyMart and 7-Eleven, with a stable assortment of products laid out so that shoppers can find things easily.

Alibaba’s agreement stipulates that franchises must contain a shelf of Tmall products and purchase products worth at least 10,000 yuan a month via LST of. In the case of Weijun, about a third of the assortment comes from LST, giving it products that have proved themselves as online best-sellers. These, plus the Tmall brand have raised Weijun’s profile, and it soon achieved sales growth of 45 percent and a 26-percent increase in foot traffic.

The two alliances have slightly different strategies. Tmall was announced plans to open 10,000 franchises within the coming year in late 2017, mainly in Tier 2 cities and is focusing on store operations: The floor area must be over 50 square meters and the staff must be trained. But JD.com is targeting all kinds of cities, as well as rural areas, and hopes for one million stores by 2021. Its selection criteria for stores are less stringent: JD.com will provide the products and put its brand on the stores, but décor and logistics are covered by the franchises.

Empires Of The Future

Some leading convenience stores should be able to survive on their own in the short term. 7-Eleven and Lawson, for instance, will continue to benefit from impulse buying. Moreover, they still have room for expansion to meet unfulfilled demand in lower-tier cities. But over the long term, even their growth will stagnate, and they will come under threat from family-run stores revived in the franchise networks of JD.com and Alibaba.

New O2O retail formats will increase the pressure. Many large supermarkets worldwide now offer online services in parallel to their physical supermarkets, so that customers can order via a website and have food delivered. Alibaba is going further, with a network of Hema stores where customers use their smartphones to see product information and to pay. They can choose to have their purchases delivered to their homes, or even to eat some of their food in the store.

Early signs indicate that O2O will go beyond an interesting experiment and significantly change the retail landscape. Hema stores are already attracting young, wealthy, tech-savvy shoppers, a coveted group. Though they are expensive to set up and run, the O2O contribution has boosted productivity, and they should soon be able to break even. We believe there is potential for at least 1,000 stores in major cities with total revenues of 200 billion yuan.

Moreover, the two empires’ domination of mobile payments gives them additional expertise and access to data. Mobile payments are already used for 35 percent of grocery purchases, and even when customers shop outside the big e-commerce platforms, they can still be a valuable source of data. The empires learn where, when, and what customers are buying, as well as which websites they like to visit, the apps they use, and whom they follow on social media.

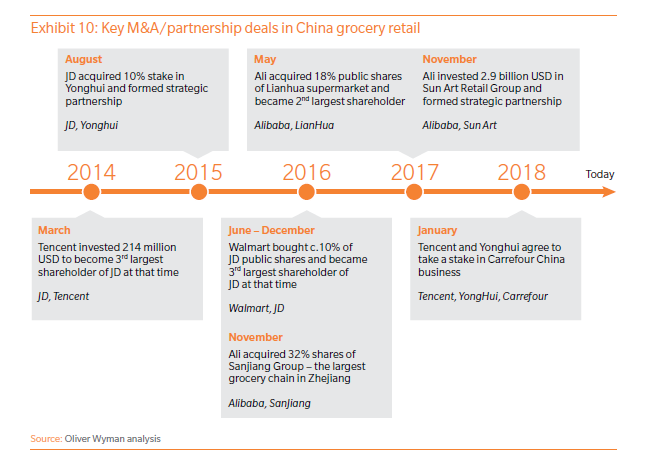

To facilitate these combinations of e-commerce and traditional retail, the groups have carried out a wave of acquisitions and partnerships over the past four years. Alibaba has made strategic investments totaling $21 billion in retail alone in just the last two years. The two empires already account for around a tenth of grocery retail, and these plays will attract more consumers through different activities and channels. Their share of grocery shopping could increase to around 30 percent over the next five years, by when it could be worth an estimated 400 billion yuan in gross merchandise value.

Facing The Challenge

So, traditional retailers need to plan the best way to function in a retail world dominated by the two empires. The first step is to figure out how a strategic alliance can leverage the empires’ tools and platforms. These will include ordering and payment systems, as well as data analytics that use customer transaction data to facilitate product selection and inventory management. Eventually, stores will be able to integrate their online and offline businesses, and they may be able to test dark stores in selected regions.

Brands, too, need to engage the new tech empires. Just as anchor tenants in malls get preferential treatment thanks to their role in attracting shoppers, brands should establish themselves as part of store networks’ core propositions, so that they benefit from prominent display and favorable financial terms. In the current system, the intermediaries that supply small stores make it hard for brands to ensure that their products – and only genuine products – find their way onto shelves and that they are appropriately priced. Working with the new tech giants could help to fix these problems and make distribution more efficient. At the same time, brands should maintain relationships with other distributors – if these survive – to avoid being completely dependent on the e-commerce giants.

The tech empires are going to strongly influence the shape and future of retail. To survive and thrive, incumbent retailers need to find ways to partner or co-exist.

This article is posted with permission of Harvard Business Publishing. Any further copying, distribution, or use is prohibited without written consent from HBP - permissions@harvardbusiness.org.